Bayer Pharma AG

Bayer Pharma AG

Latest Content by PharmaCompass

KEY PRODUCTS

KEY PRODUCTS

About

PEGS Boston SummitPEGS Boston Summit

Industry Trade Show

Not Confirmed

11 May-15 November, 2026

DIA Global Annual Meet...DIA Global Annual Meeting

Industry Trade Show

Not Confirmed

14-18 June, 2026

Discovery EuropeDiscovery Europe

Industry Trade Show

Not Confirmed

15-16 June, 2026

CONTACT DETAILS

Digital content ![]()

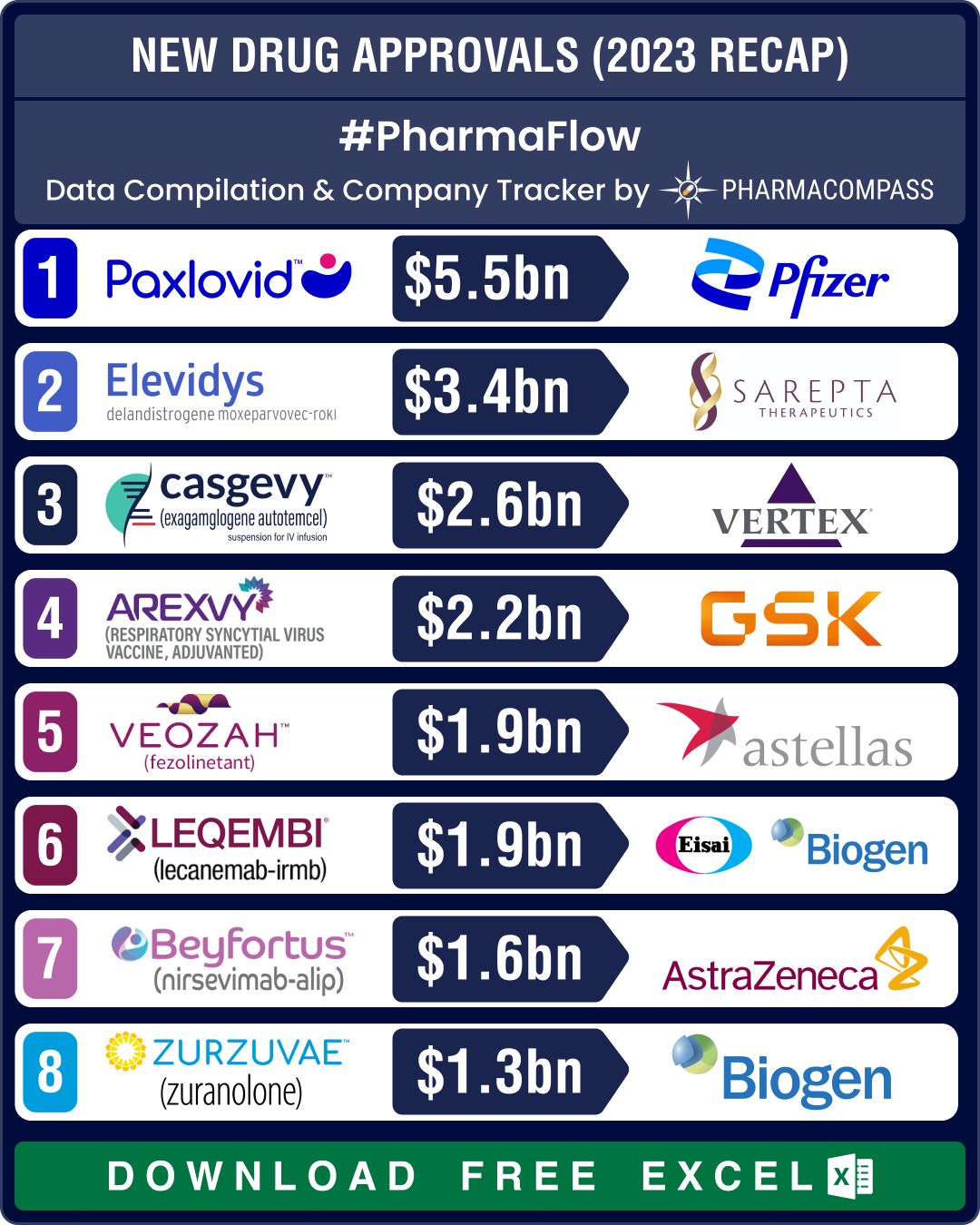

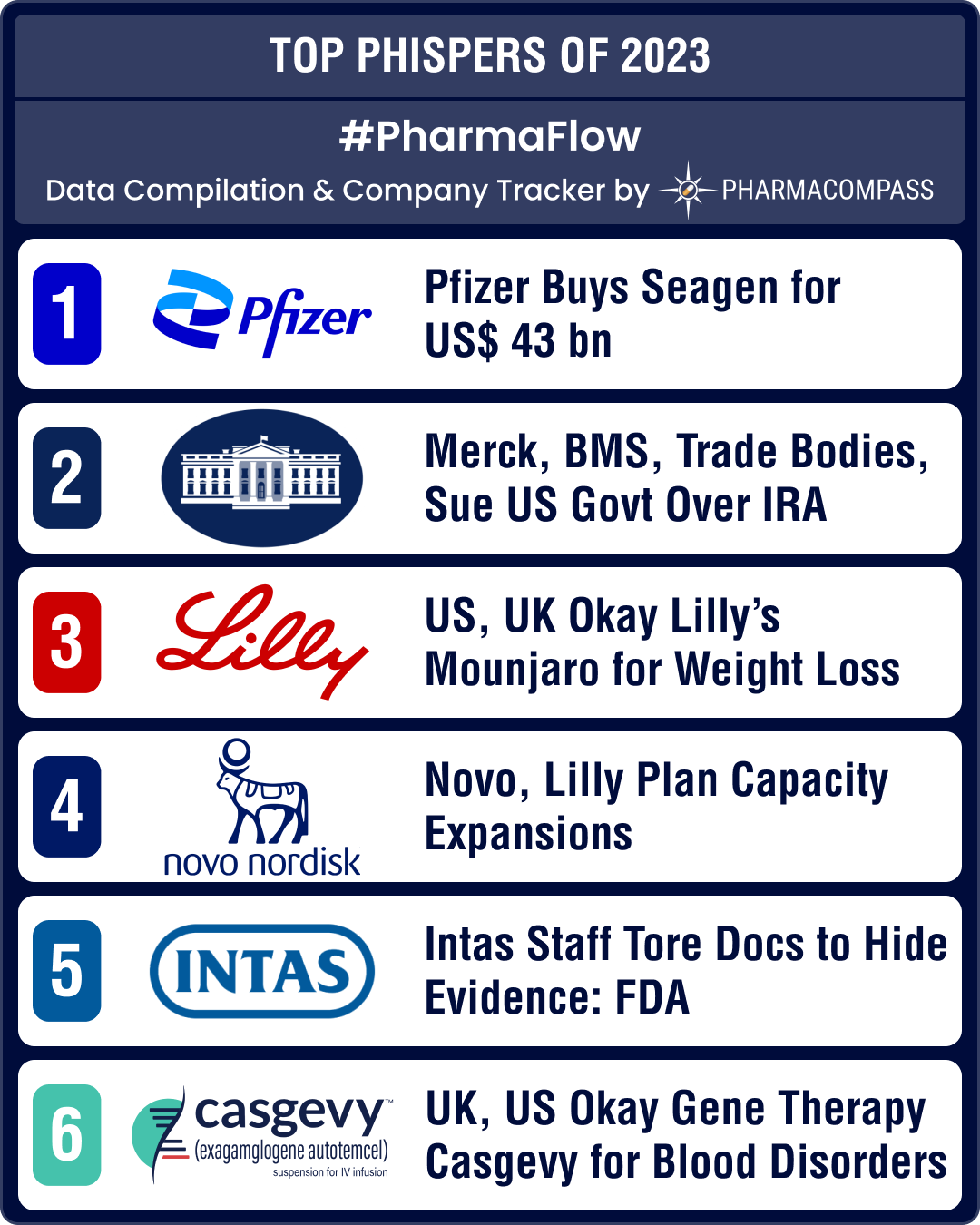

DATA COMPILATION #PharmaFlow

NEWS #PharmaBuzz

08 Jun 2026

// BUSINESSWIRE

05 Jun 2026

// PRESS RELEASE

05 Jun 2026

// PRESS RELEASE

02 Jun 2026

// BUSINESSWIRE

30 May 2026

// BUSINESSWIRE

27 May 2026

// REUTERS

USDMF

FULL SCREEN VIEW Click here to open all results in a new tab [this preview display 10 results]

FULL SCREEN VIEW Click here to open all results in a new tab [this preview display 10 results]Drugs in Development

FULL SCREEN VIEW Click here to open all results in a new tab [this preview display 10 results]FDF Dossiers

FULL SCREEN VIEW Click here to open all results in a new tab [this preview display 10 results]FDA Orange Book

Europe

FULL SCREEN VIEW Click here to open all results in a new tab [this preview display 10 results]Canada

FULL SCREEN VIEW Click here to open all results in a new tab [this preview display 10 results]KEY PRODUCTS

TOP RANKED SUPPLIER FOR:

Inspections and registrations

ABOUT THIS PAGE

Bayer Pharma AG is a supplier offers 56 products (APIs, Excipients or Intermediates).

Find Ethinyl Estradiol bulk with DMF, CEP, JDMF offered by Bayer Pharma AG

Find Norethisterone bulk with DMF, CEP, JDMF offered by Bayer Pharma AG

Find Acarbose bulk with DMF, CEP offered by Bayer Pharma AG

Find CAS 50-28-2 bulk with DMF, JDMF offered by Bayer Pharma AG

Find Ciprofloxacin bulk with DMF, CEP offered by Bayer Pharma AG

Find Ciprofloxacin Hydrochloride bulk with DMF, CEP offered by Bayer Pharma AG

Find Drospirenone bulk with DMF, CEP offered by Bayer Pharma AG

Find Estradiol bulk with DMF, CEP offered by Bayer Pharma AG

Find Gadobutrol bulk with DMF, CEP offered by Bayer Pharma AG

Find Iopromide bulk with DMF, CEP offered by Bayer Pharma AG

Find Levonorgestrel bulk with DMF, CEP offered by Bayer Pharma AG

Find Medroxyprogesterone Acetate bulk with DMF, CEP offered by Bayer Pharma AG

Find Norethisterone Acetate bulk with DMF, CEP offered by Bayer Pharma AG

Find Rivaroxaban bulk with DMF, CEP offered by Bayer Pharma AG

Find Testosterone bulk with DMF, CEP offered by Bayer Pharma AG

Find Testosterone Enanthate bulk with DMF, CEP offered by Bayer Pharma AG

Find Alpha-Cyclodextrin bulk with DMF offered by Bayer Pharma AG

Find Aspirin bulk with CEP offered by Bayer Pharma AG

Find Azelaic Acid bulk with DMF offered by Bayer Pharma AG

Find Ciprofloxacin bulk with DMF offered by Bayer Pharma AG

Find Clotrimazole bulk with CEP offered by Bayer Pharma AG

Find Cyproterone Acetate bulk with CEP offered by Bayer Pharma AG

Find Dienogest bulk with DMF offered by Bayer Pharma AG

Find Estradiol Valerate bulk with CEP offered by Bayer Pharma AG

Find Estriol bulk with CEP offered by Bayer Pharma AG

Find Etofenamate bulk with CEP offered by Bayer Pharma AG

Find Gadolinium Ethoxybenzyl Dtpa bulk with DMF offered by Bayer Pharma AG

Find Gestodene bulk with CEP offered by Bayer Pharma AG

Find Hydrocortisone bulk with CEP offered by Bayer Pharma AG

Find Iloprost bulk with DMF offered by Bayer Pharma AG

Find Iopromide bulk with CEP offered by Bayer Pharma AG

Find Levonorgestrel bulk with DMF offered by Bayer Pharma AG

Find Mesalazine bulk with JDMF offered by Bayer Pharma AG

Find Molidustat bulk with DMF offered by Bayer Pharma AG

Find Moxifloxacin Hydrochloride bulk with CEP offered by Bayer Pharma AG

Find Nifedipine bulk with CEP offered by Bayer Pharma AG

Find Norethisterone bulk with CEP offered by Bayer Pharma AG

Find Rivaroxaban bulk with DMF offered by Bayer Pharma AG

Find Testosterone bulk with CEP offered by Bayer Pharma AG

Find Testosterone Undecanoate bulk with DMF offered by Bayer Pharma AG

Find Nisoldipine bulk offered by Bayer Pharma AG

Find Ciprofloxacin Hydrochloride bulk offered by Bayer Pharma AG

Find Enrofloxacin bulk offered by Bayer Pharma AG

Find Estradiol bulk offered by Bayer Pharma AG

Find Estradiol Benzoate bulk offered by Bayer Pharma AG

Find Estradiol Valerate bulk offered by Bayer Pharma AG

Find Ethinyl Estradiol bulk offered by Bayer Pharma AG

Find Finerenone bulk offered by Bayer Pharma AG

Find Methylprednisolone Aceponate bulk offered by Bayer Pharma AG

Find Moxifloxacin bulk offered by Bayer Pharma AG

Find Nifedipine bulk offered by Bayer Pharma AG

Find Pentetic Acid bulk offered by Bayer Pharma AG

Find Pradofloxacin bulk offered by Bayer Pharma AG

Find Regorafenib bulk offered by Bayer Pharma AG

Find Sorafenib bulk offered by Bayer Pharma AG

Find Berrysiguat bulk offered by Bayer Pharma AG