Data Compilation #PharmaFlow

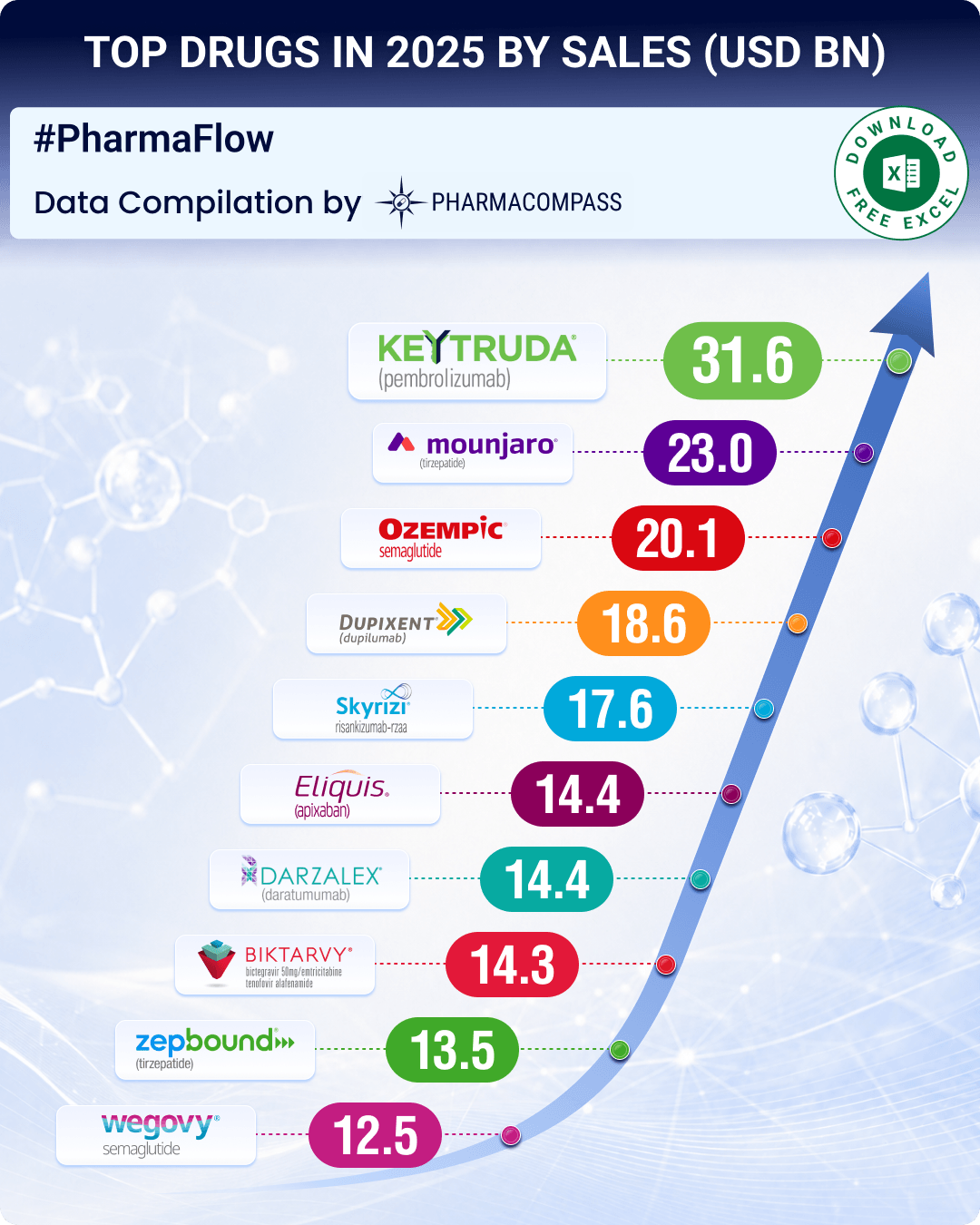

Top Pharma Companies & Drugs in 2025: Lilly vaults eight spots to emerge at the top; GLP-1 drugs dominate list

For the pharmaceutical industry, 2025 was a watershed year

when obesity drugs settled firmly in the

Prostaglandin market to cross US$ 1.27 bn by 2035; Liquidia’s Yutrepia okayed for pulmonary hypertension

Prostaglandins are natural fatty acid compounds

produced by the human body. They are made from

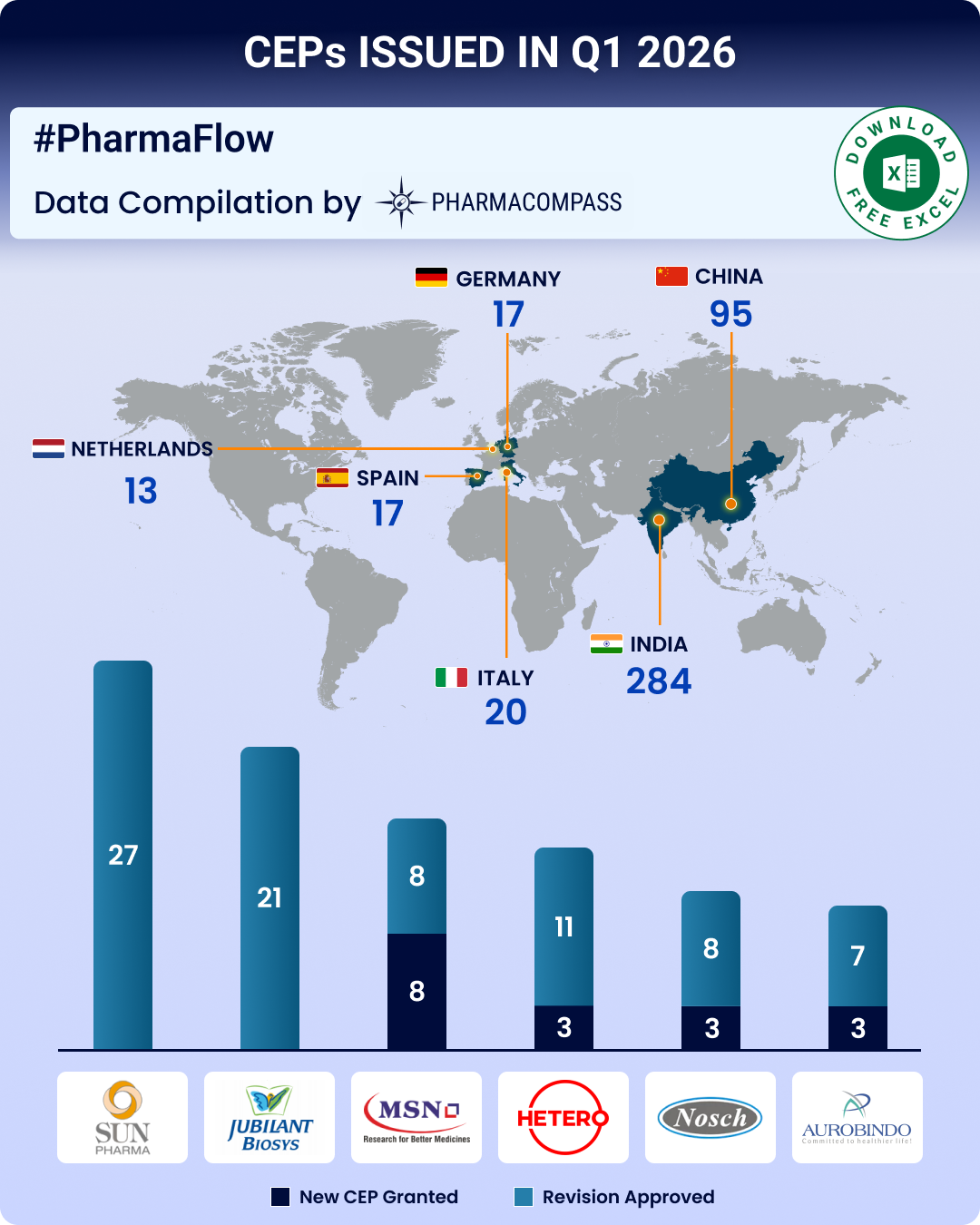

CEP Q1 2026 Update: CEP 2.0, EDQM’s new guidelines strengthen ecosystem; Indian firms top list of CEPs issued

PharmaCompass is introducing a new regulatory update

that tracks developments in Certificates of Su

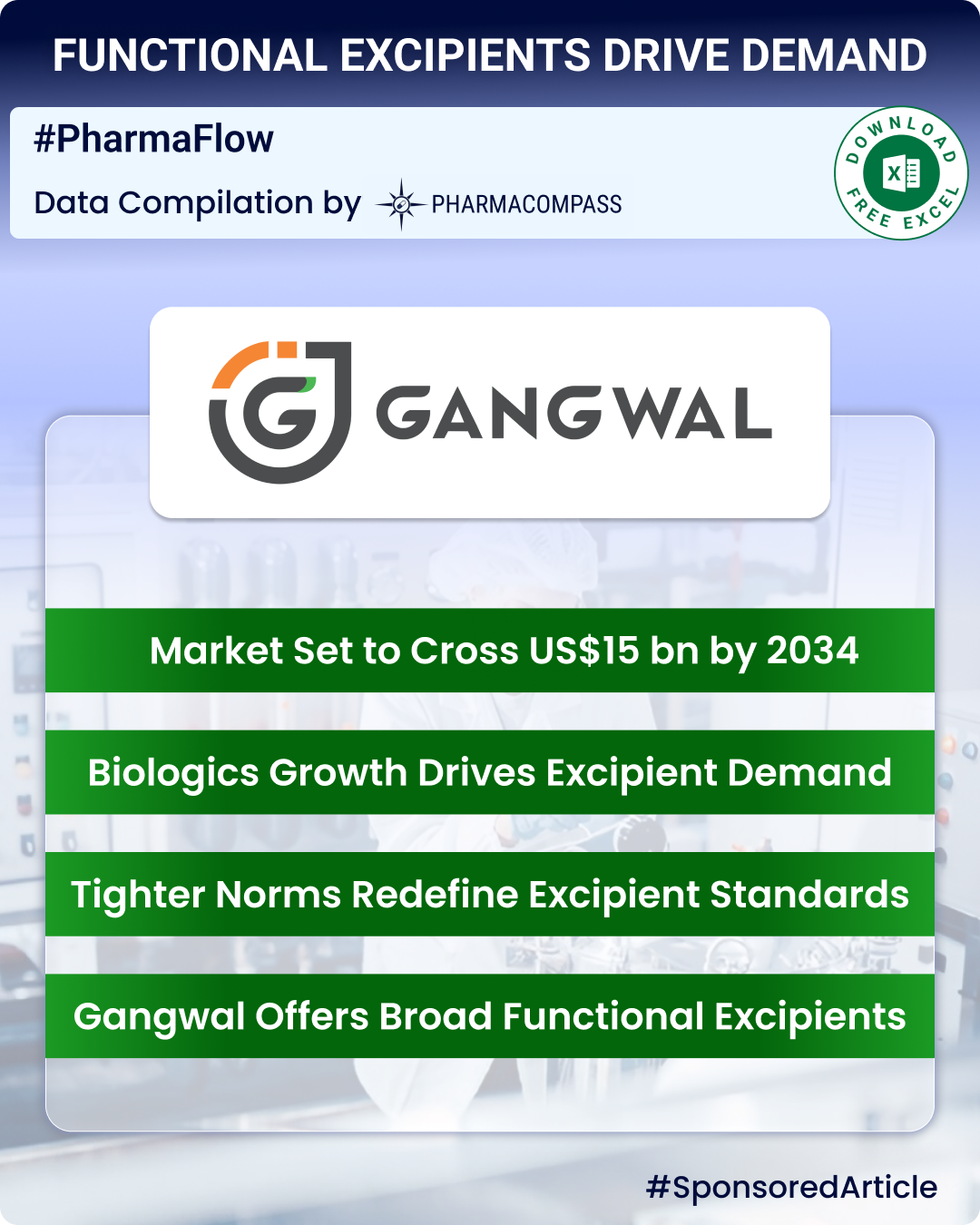

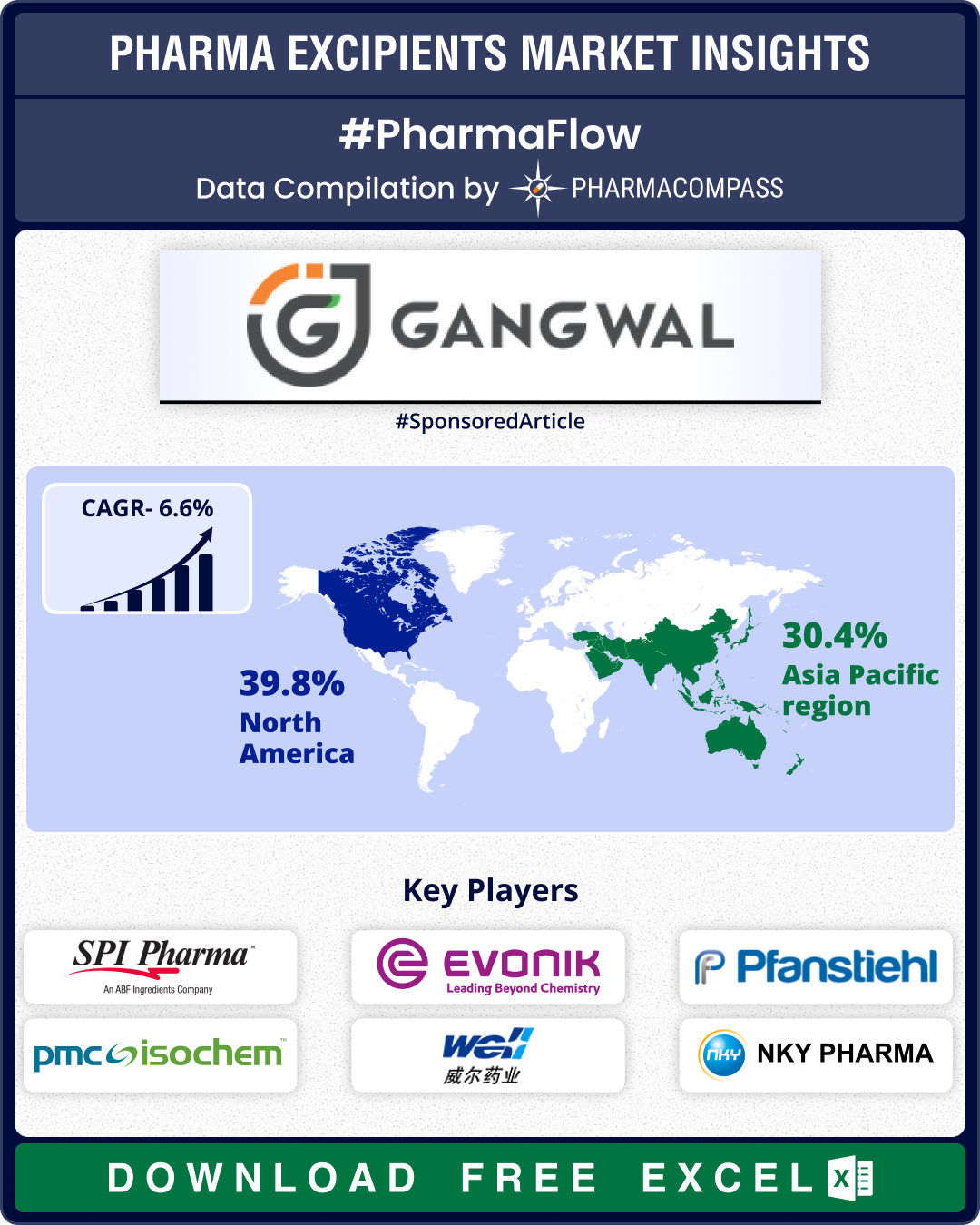

Excipient Market Overview: Clariant sets up its first PEG excipients facility in US; India harmonizes 22 excipient monographs

The market for pharmaceutical excipients — or inactive substances used in the production of dr

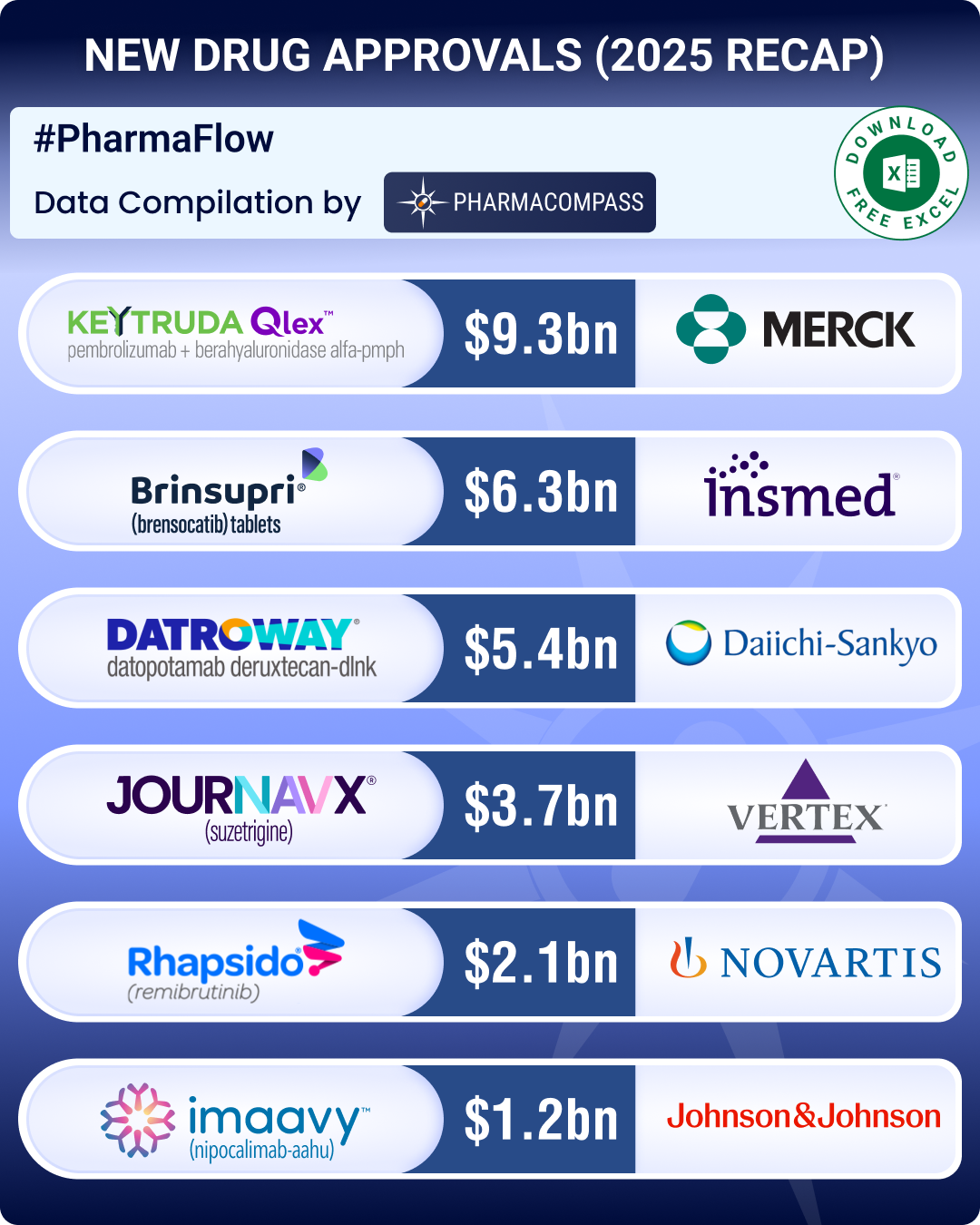

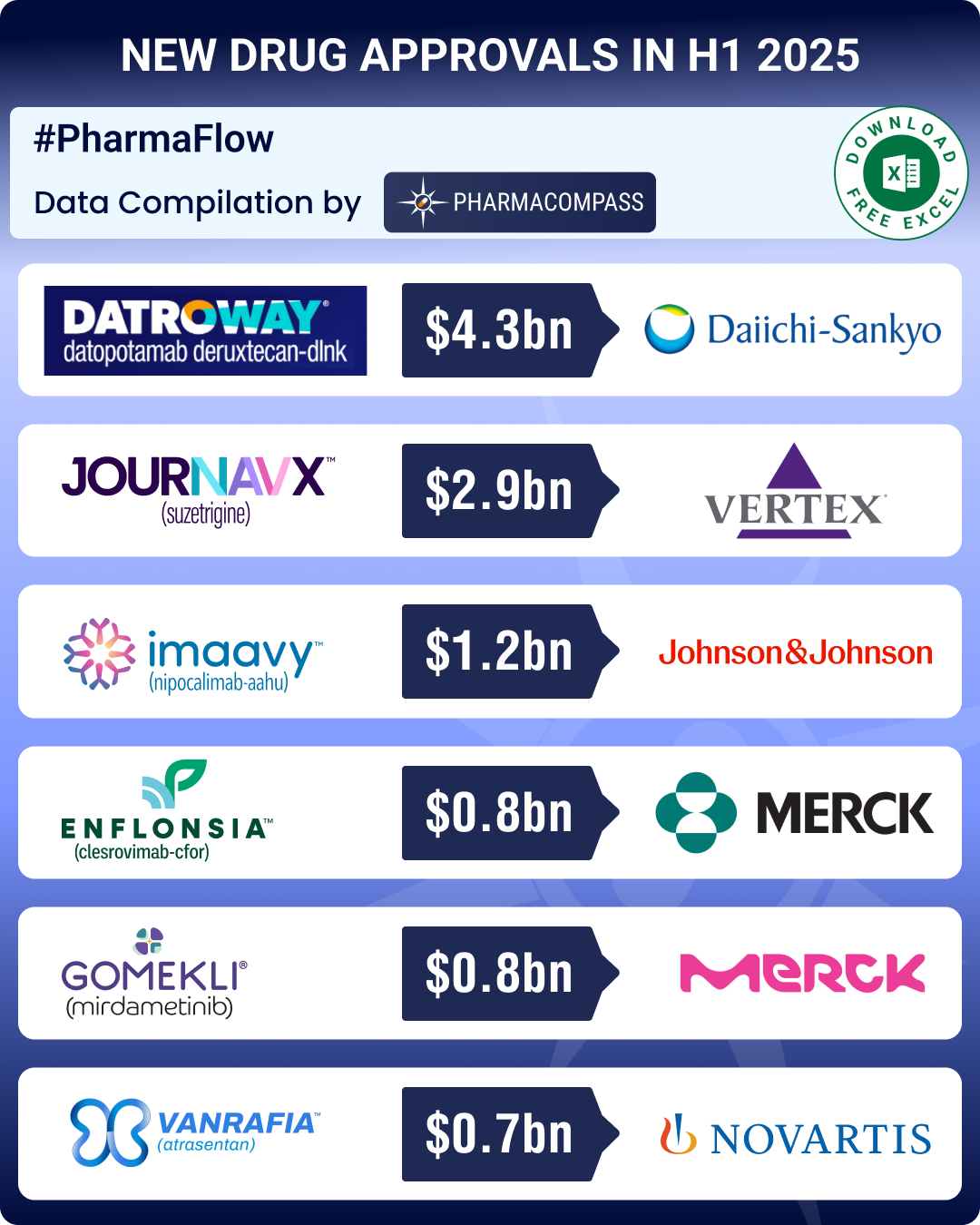

FDA approvals drop 8% in 2025, with fewer blockbusters; Brinsupri, Rhapsido make it to first-in-class list

Our

update for new drug approvals by the US Food and Drug Administration (FDA) in

the first half (

FDA’s December 2025 OPOE list features 784 prescription drugs, 73 OTC drugs

This

week, PharmaCompass brings you key highlights of the US Food and Drug Administration’s D

Top news of 2025: Drugmakers invest in US capacities, agree to lower Medicaid prices; Pfizer buys obesity-focused biotech Metsera

The year 2025 was an eventful one, marked by increased trade

tensions, tariff threats, accelerated

CDMO Activity Tracker: Lupin’s CDMO commissions oncology block in India; Cambrex, Axplora, Hovione expand operations

The global contract development and

manufacturing organization (CDMO) market has been growing at a

Antibiotic market to reach US$ 74.07 billion by 2033; FDA approves GSK’s Blujepa for uncomplicated UTIs

The global market

for antibiotics has been witnessing several challenges. First, there is growing

Excipient Market Overview: Evonik launches high-purity excipients; India mandates disclosures from March 2026

The global pharmaceutical excipients market continued to evolve in the third quarter (Q3) of 2025, s

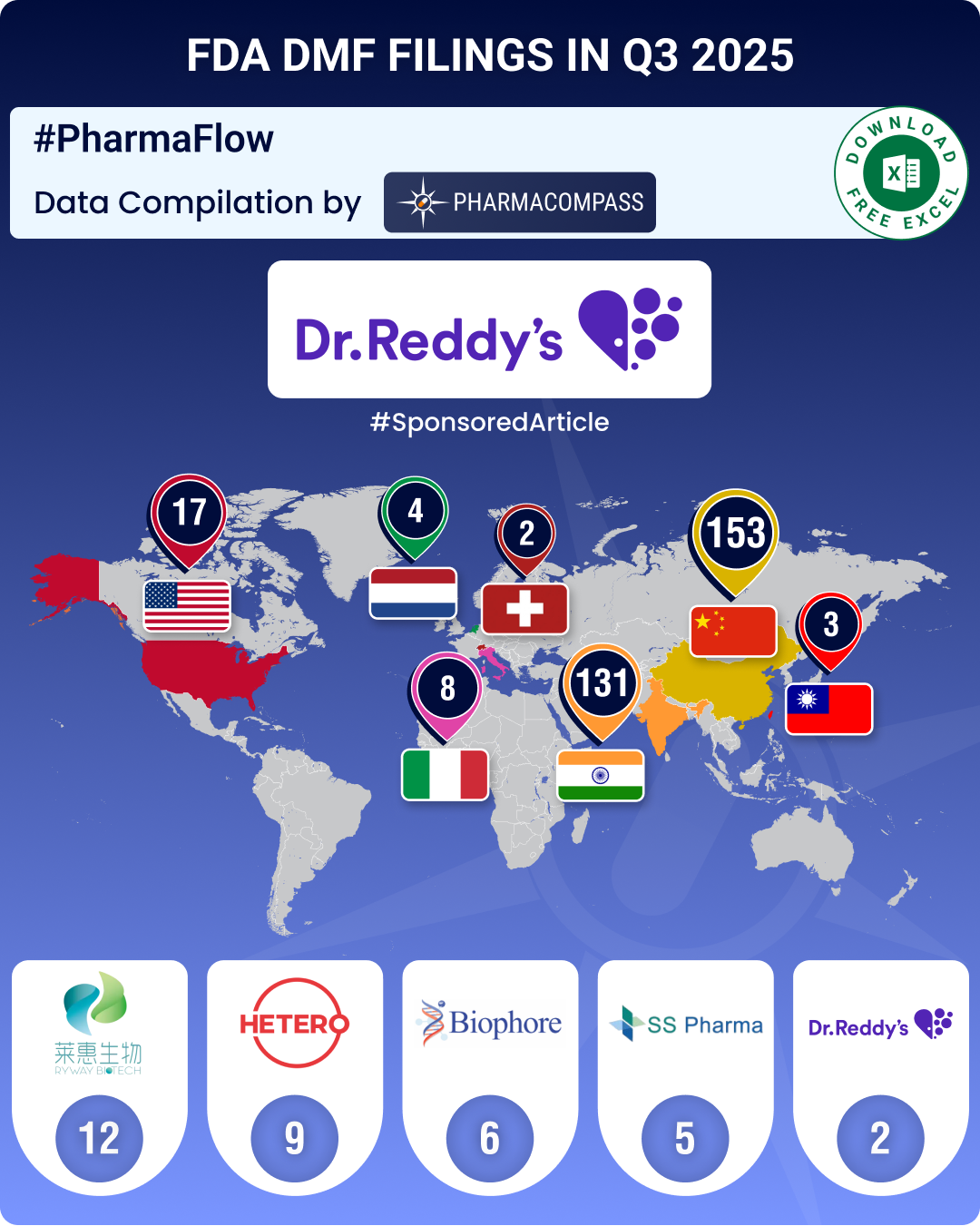

DMF filings rise 4.5% in Q3 2025; China holds lead, India records 20% growth in submissions

The

third quarter (Q3) of 2025 witnessed a steady rise in Drug Master File (DMF) submissions to the

CDMO Activity Tracker: Veranova, ChemExpress invest in ADC facilities; Cohance to set up oligonucleotide facility in India

The contract development and manufacturing organization (CDMO) sector has emerged as a key partner i

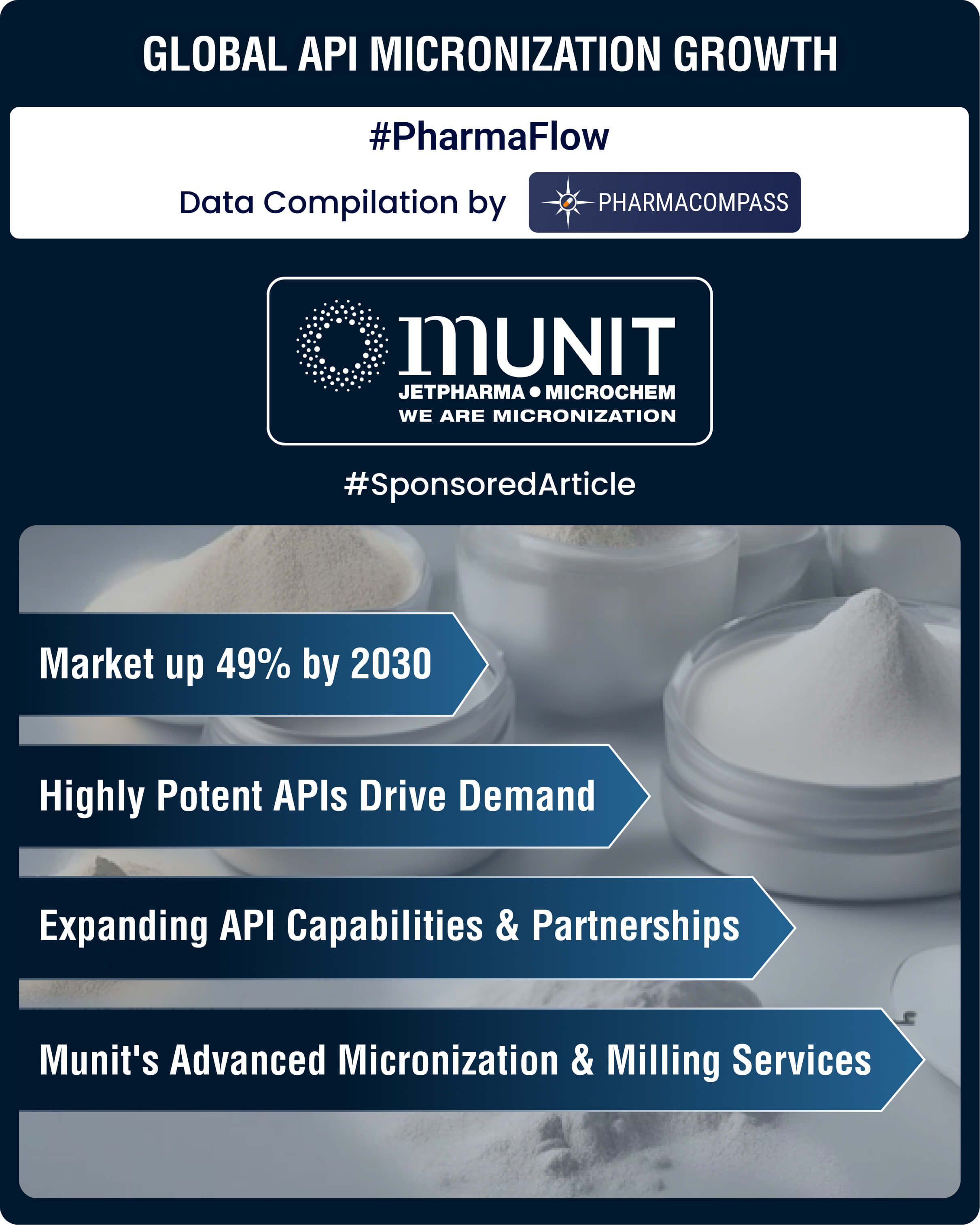

Global API micronization market set to surge 49% by 2030, led by specialized industry pioneers

Precise particle size control has become the cornerstone of modern pharmaceutical manufacturing. Wit

FDA approvals drop 24% in H1 2025; GSK’s UTI med, Vertex’s non-opioid painkiller lead pack of first-in-class meds

It has been a turbulent year for the US

Food and Drug Administration (FDA), marked by reduction

CDMO Activity Tracker: Veranova, Carbogen lead ADC investments; Axplora, Polfa Tarchomin, Famar expand European footprint

During the second quarter (Q2) of 2025, contract development and manufacturing organizations (CDMOs)

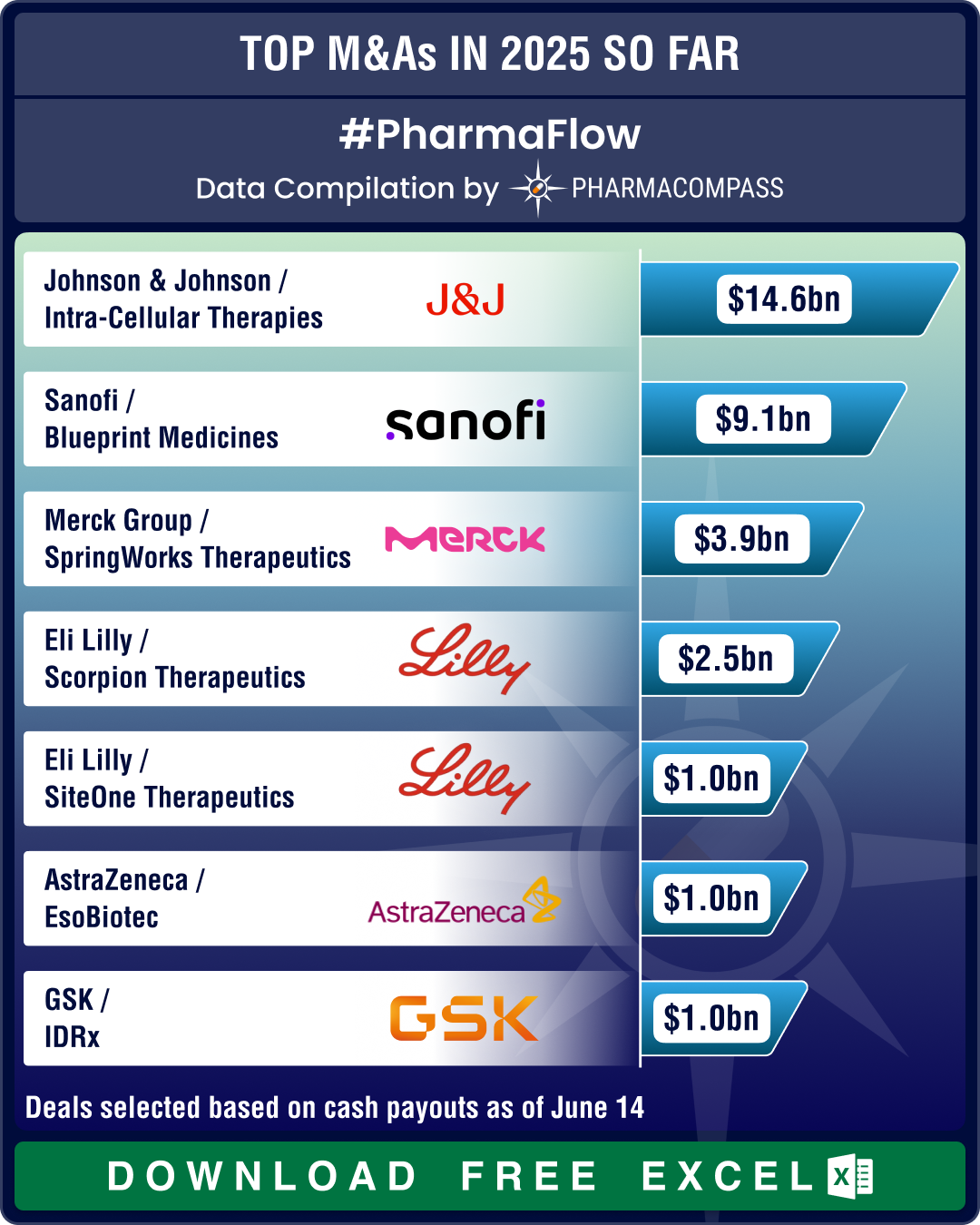

J&J’s Intra‑Cellular buyout, BMS’ oncology gambit, Sanofi’s Blueprint acquisition drive mega deals in H1 2025

The pharmaceutical industry has witnessed a wave of mergers, acquisitions, and strategic partnership

Excipient Market Overview: Roquette announces restructuring post IFF Pharma buyout; WHO, FDA advance regulatory frameworks

The pharmaceutical excipients market saw significant strategic

consolidations, technological develo

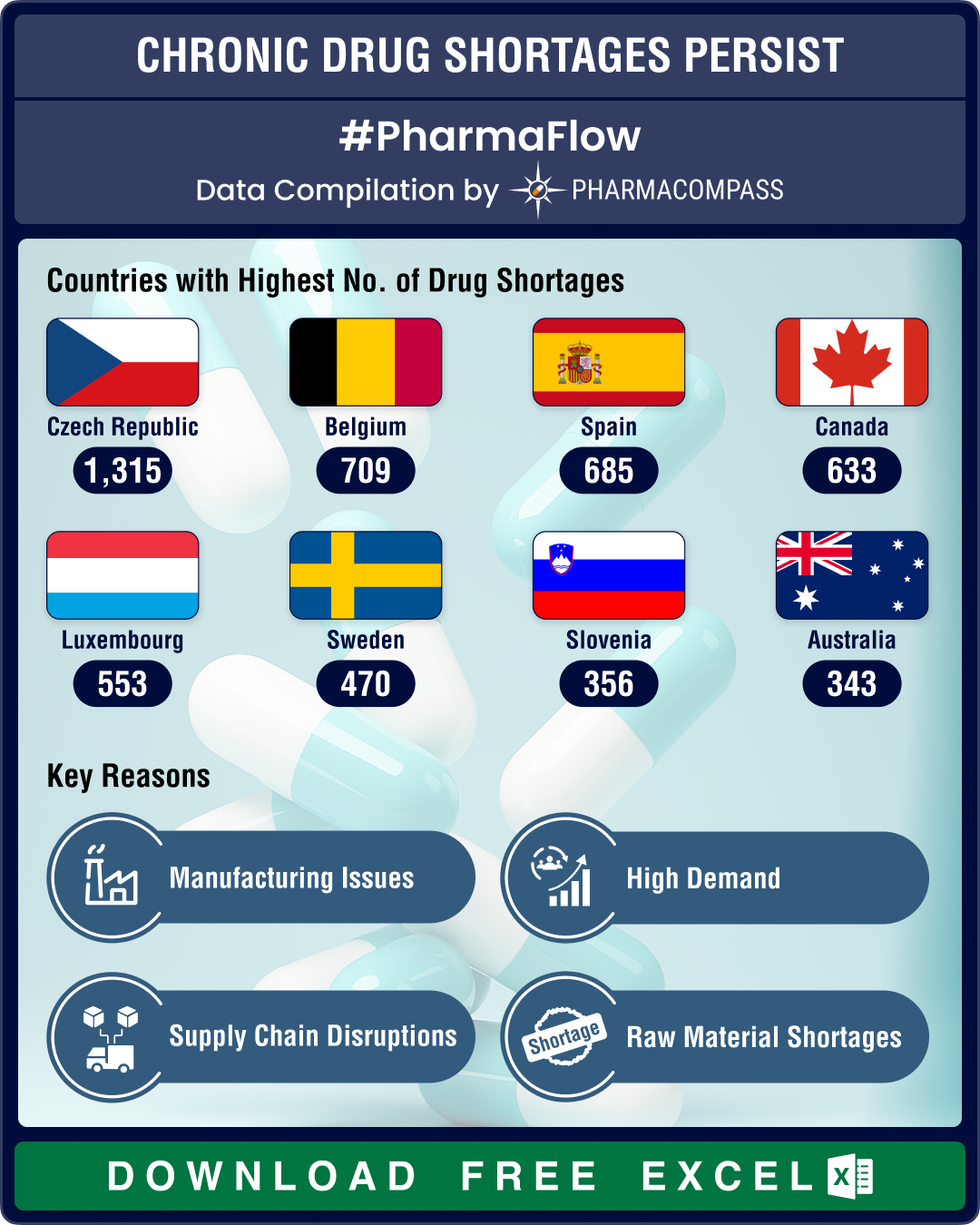

US drug shortages reduce 16% YoY in Q1 2025; CNS drugs, antimicrobials face highest scarcities

The pharmaceutical industry in the United States continued to

grapple with drug shortages during th

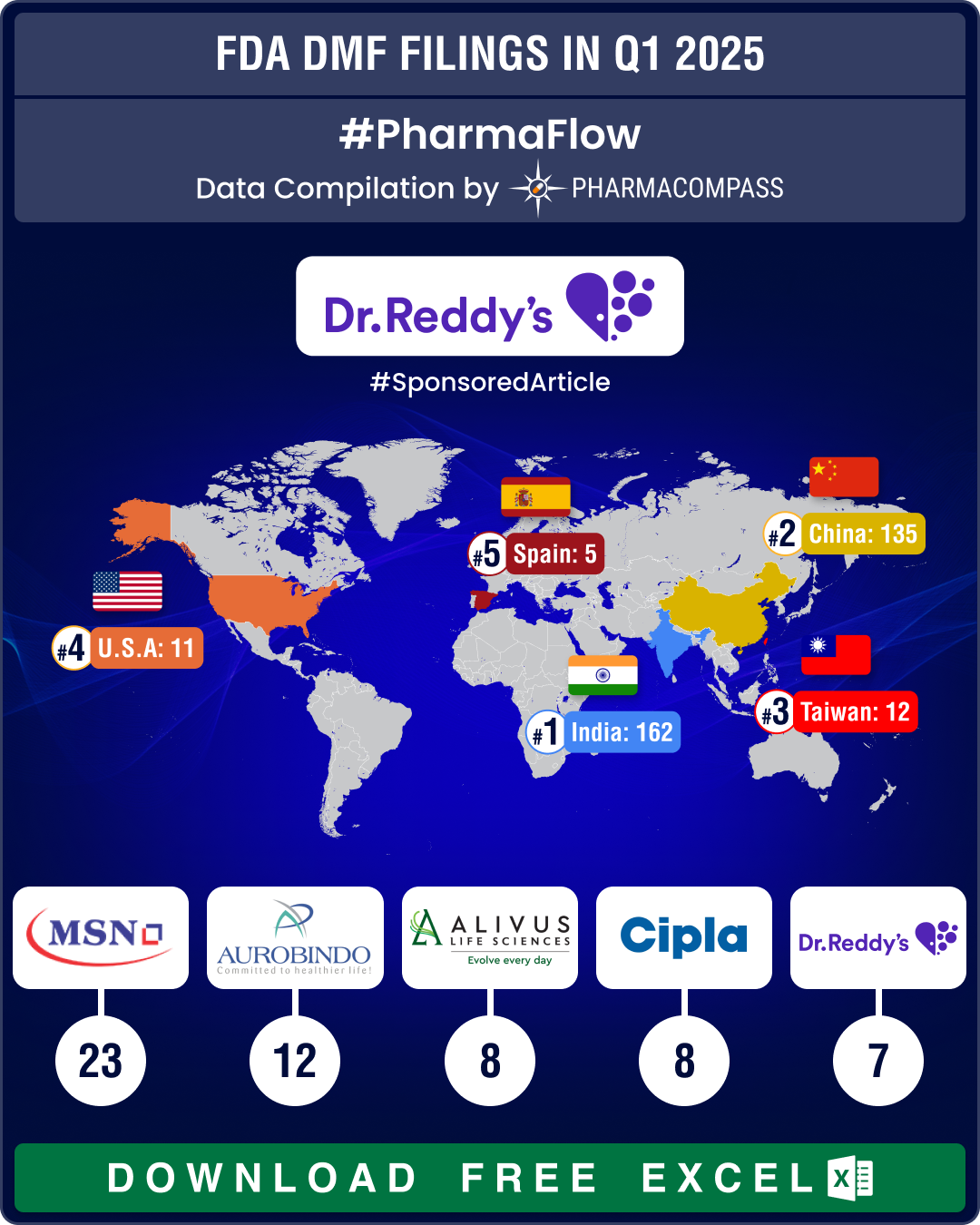

DMF filings surge 44% in Q1 2025; India tops list with 51% rise in year-on-year submissions

The first quarter (Q1) of 2025 witnessed an impressive surge in Drug Master File (DMF) submissions t

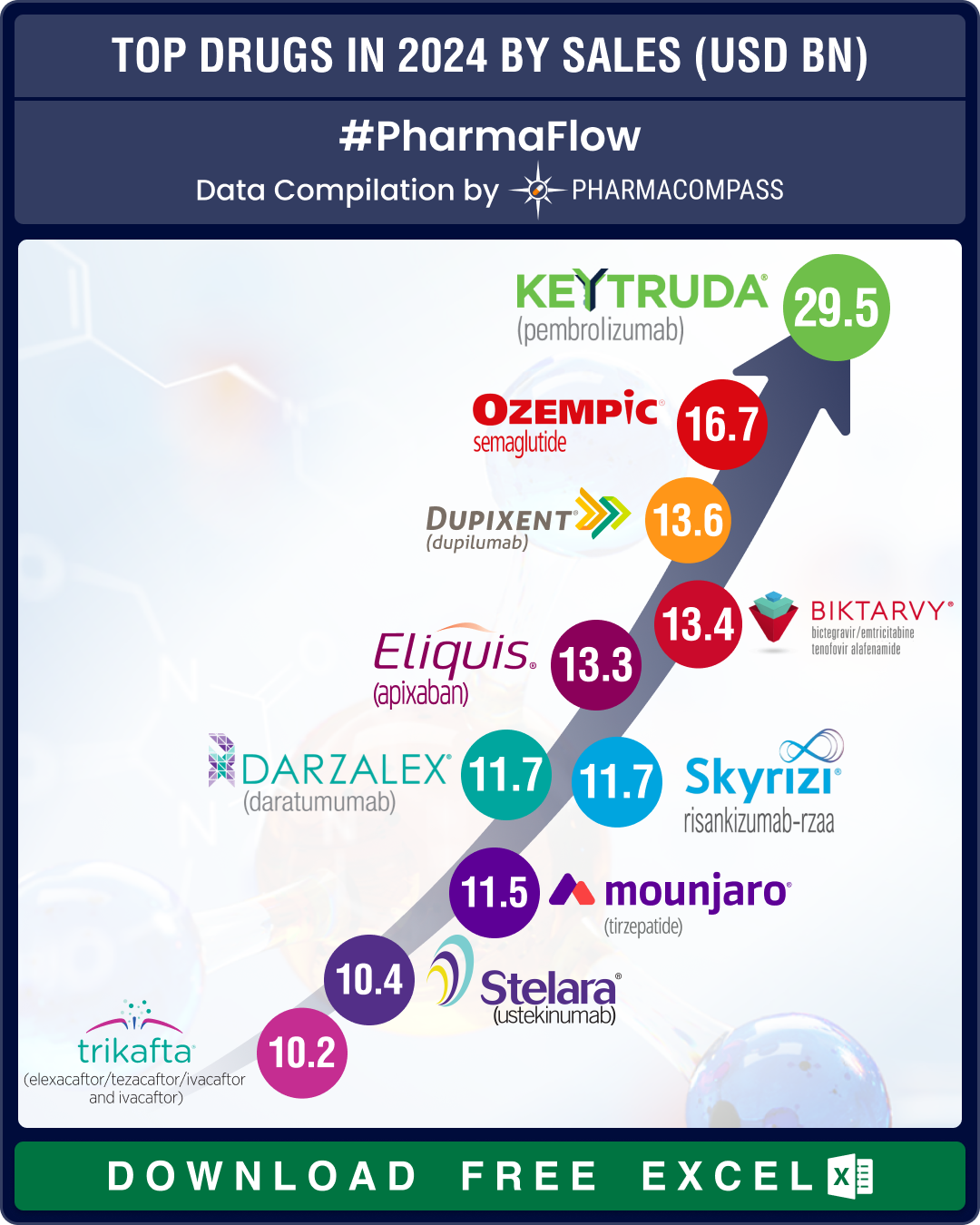

Top Pharma Companies & Drugs in 2024: Merck’s Keytruda maintains top spot as Novo’s semaglutide nips at its heels

In 2024, Big Pharma players consolidated

and maintained their dominance, even as innovation continu

How Trump’s tariffs on imported drugs can hurt supply chains, consumers and industry

Ever since Donald Trump has moved into the White House for a second term, there has been turmoil acr

CDMO Activity Tracker: Axplora enhances ADC capacities, Quotient beefs up HPAPI capabilities; Evonik, EUROAPI forge deals

The contract development and

manufacturing organization (CDMO) sector witnessed significant activit

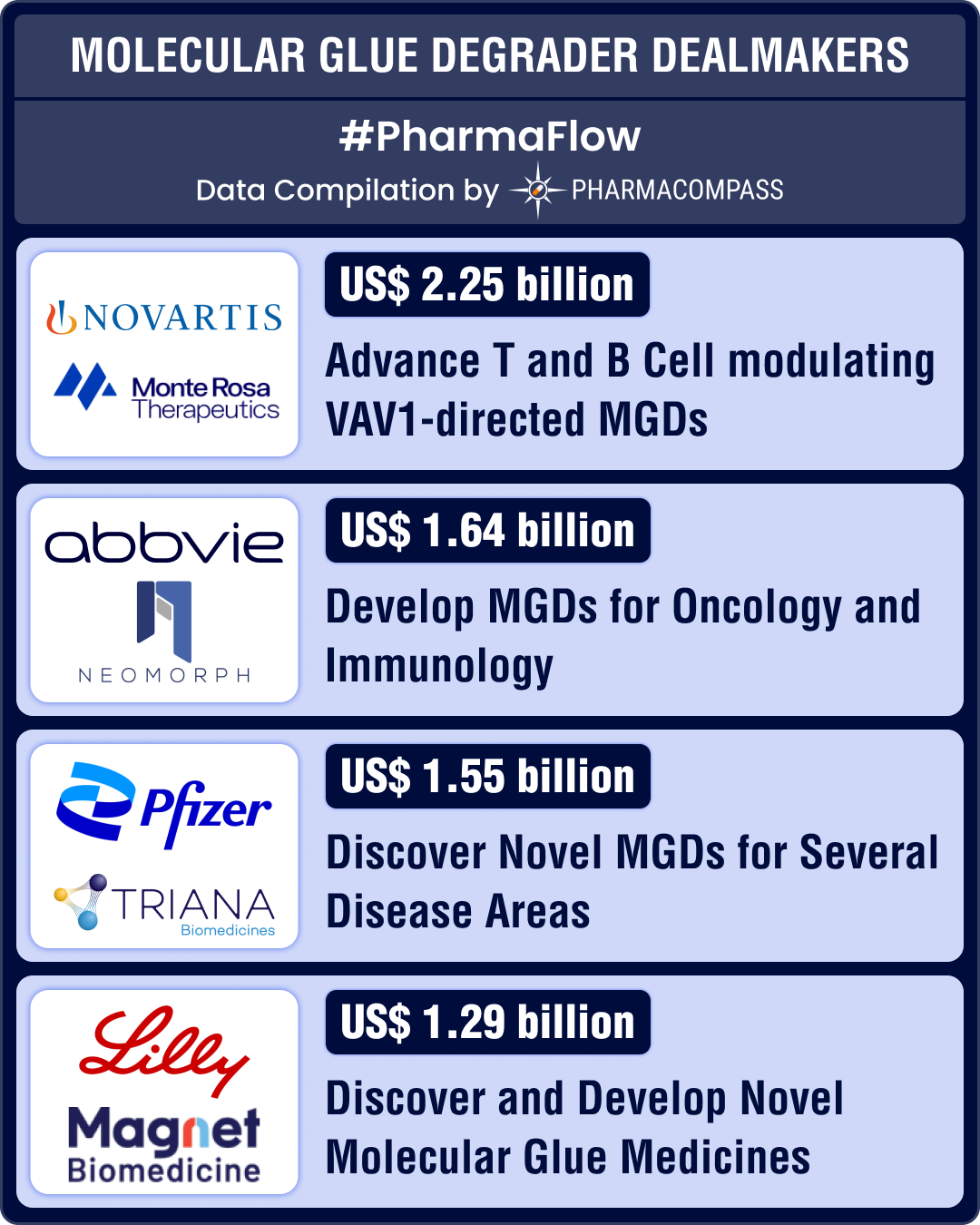

Molecular glue degraders: Lilly, AbbVie sign billion-dollar deals; BMS leads with three late-stage drugs

This week, we delve into molecular glue degraders (MGDs), one of the most promising frontiers in dru

AI drug discovery market to grow 30% CAGR, to reach US$ 35 bn by 2034; Novo, Lilly, BMS forge deals

Artificial intelligence (AI) is emerging

as a transformative force in drug discovery and developmen

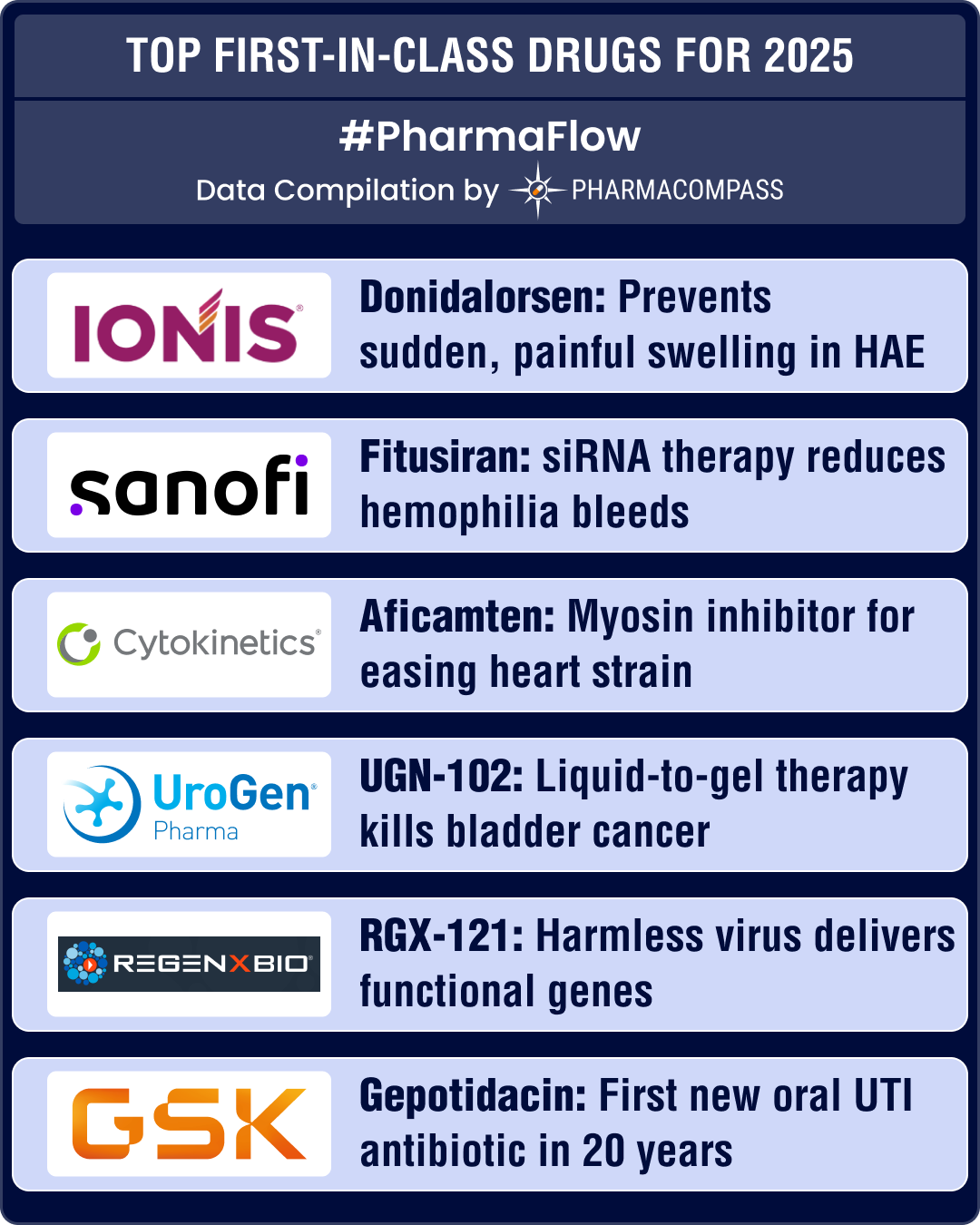

Top first-in-class drug candidates of 2025: Ionis’ donidalorsen, Sanofi’s fitusiran, Cytokinetics’ aficamten await FDA approval

First‑in‑class drugs are therapies with entirely new approaches that improve patient out

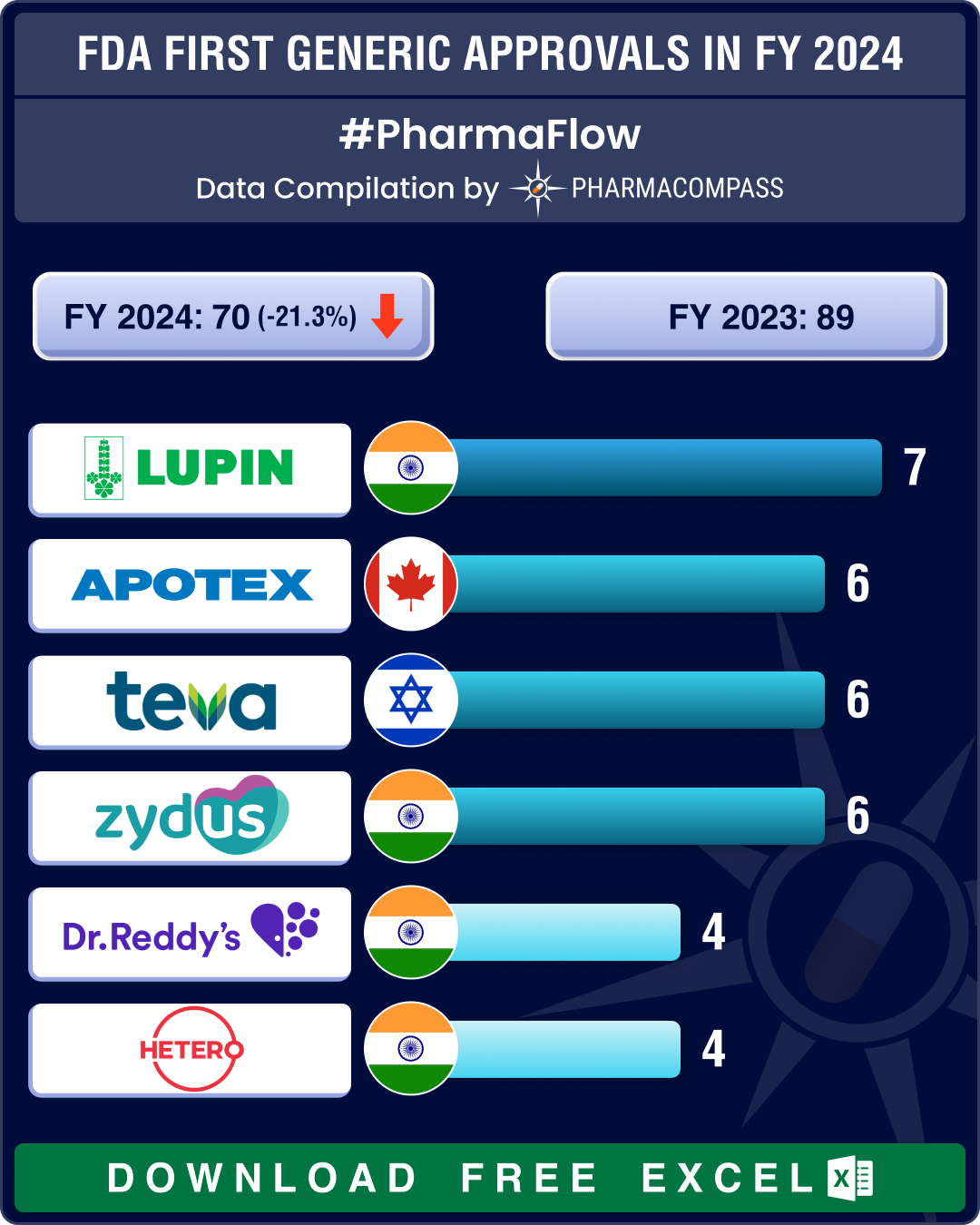

FDA’s first generic approvals slump 21% in 2024; Novartis’ top seller Entresto, cancer blockbuster Tasigna lead 2024 patent cliff

A watershed moment in the journey of a drug is when it transitions from being a patented, high‐

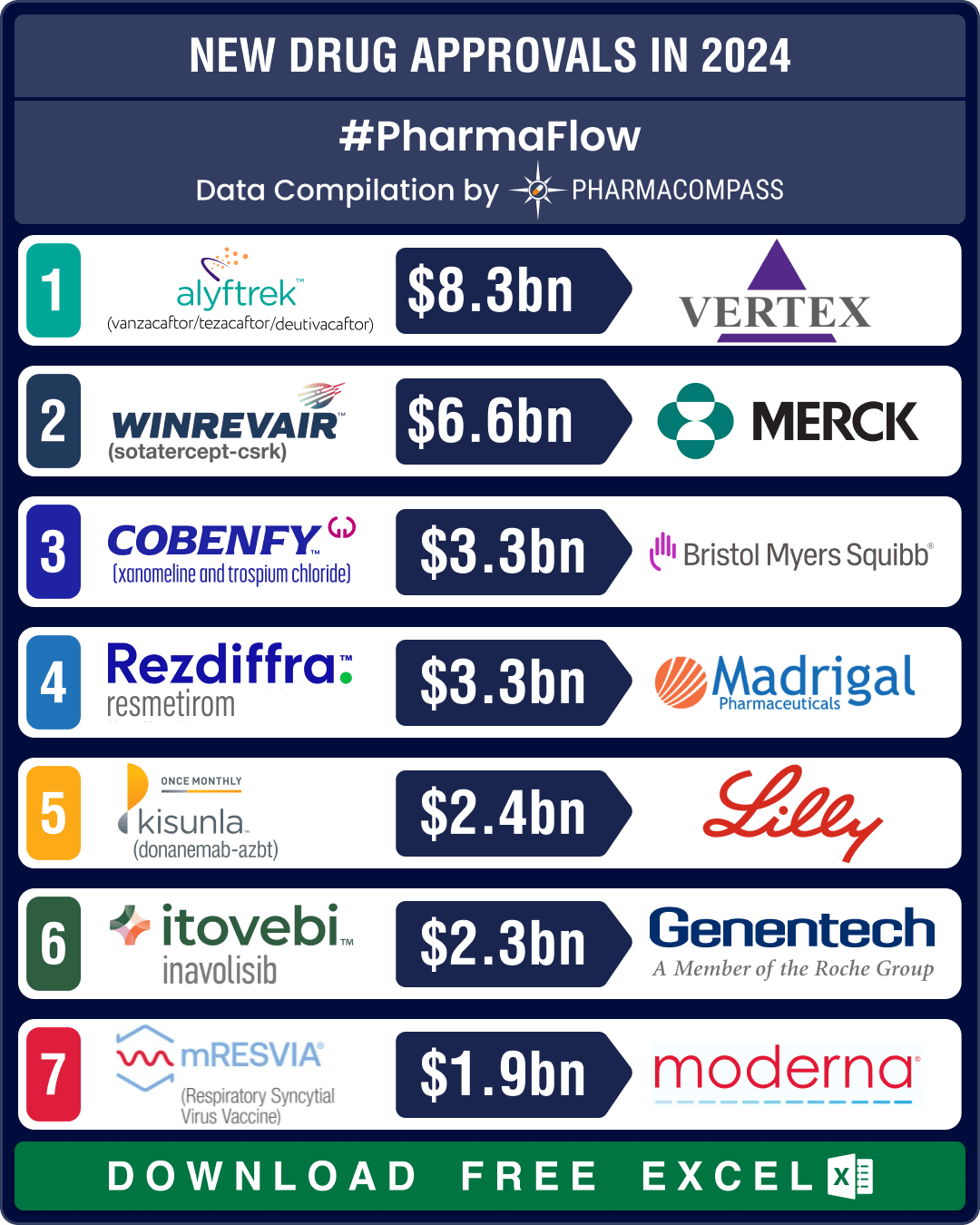

FDA okays 50 new drugs in 2024; BMS’ Cobenfy, Lilly’s Kisunla lead pack of breakthrough therapies

In 2024, the biopharma industry continued to advance on its robust trajectory of innovation. Though

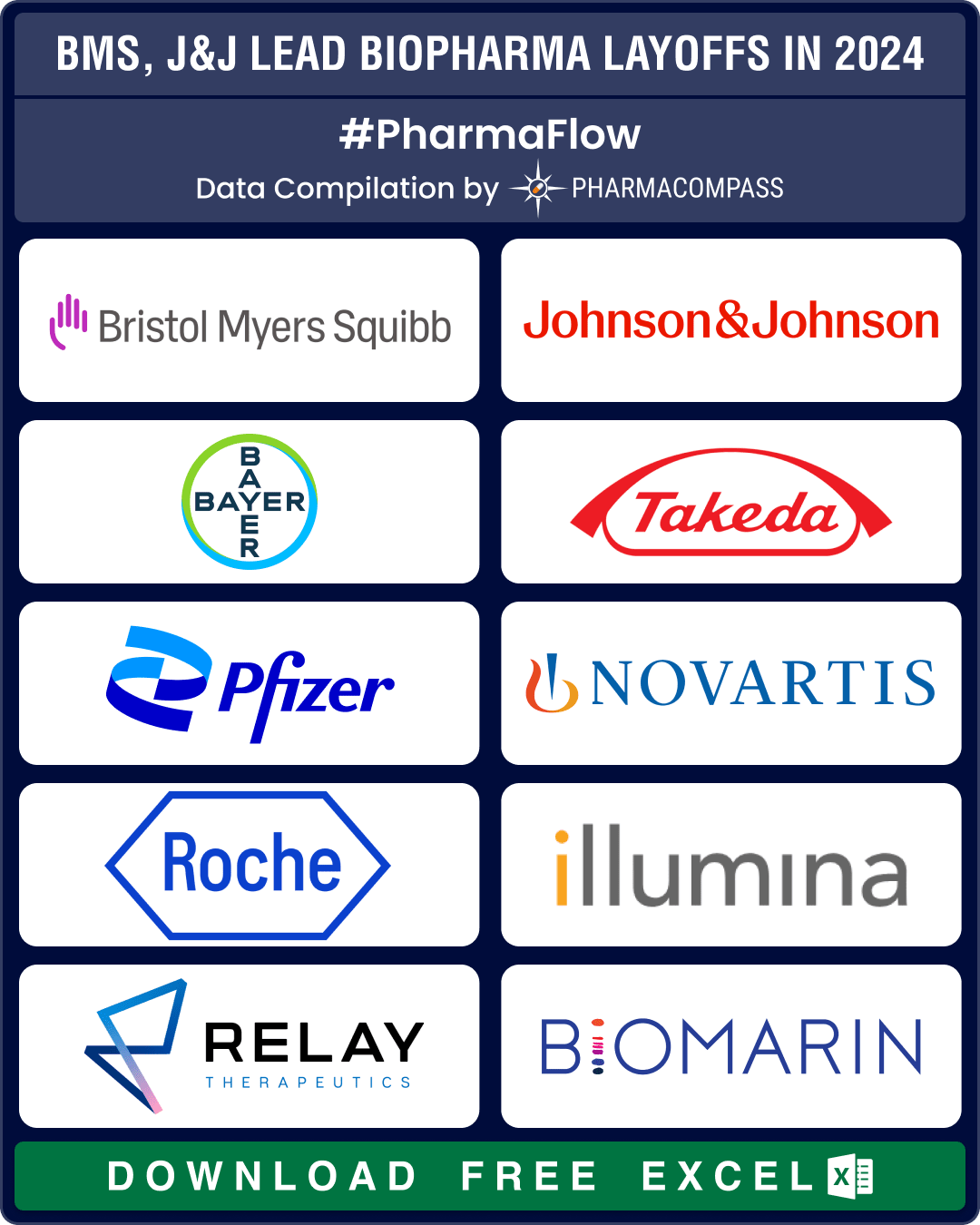

BMS, J&J, Bayer lead 25,000+ pharma layoffs in 2024; Amylyx, FibroGen, Kronos Bio hit by trial failures, cash crunch

Since 2022, there has been a significant surge in layoffs by pharmaceutical and biotech companies. W

- Privacy policy

- Terms and conditions

- Disclaimers

-

- Product listings are provided for informational purposes only. We do not supply or sell any products. Any products that may be covered by patent(s) are supplied solely for uses permitted under Section 107A of the Indian Patents Act and not for commercial sale.