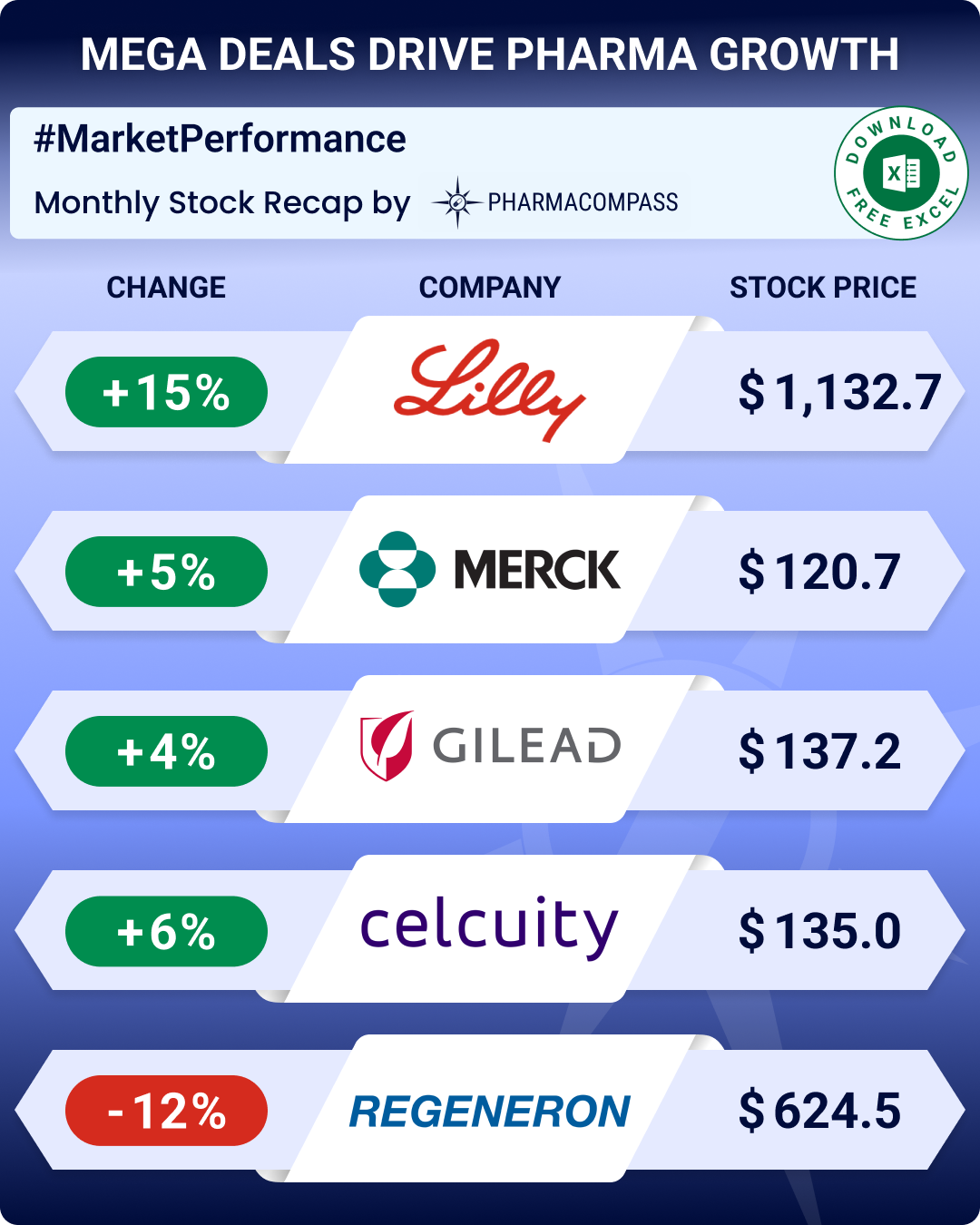

Stock Recap #PipelineProspector

Pipeline Prospector April-May 2026 highlights: Sun Pharma buys Organon for about US$ 11.8 bn; Lilly on acquisition overdrive

April and May were tough months, with oil prices rising globally due to the war in the Middle East.

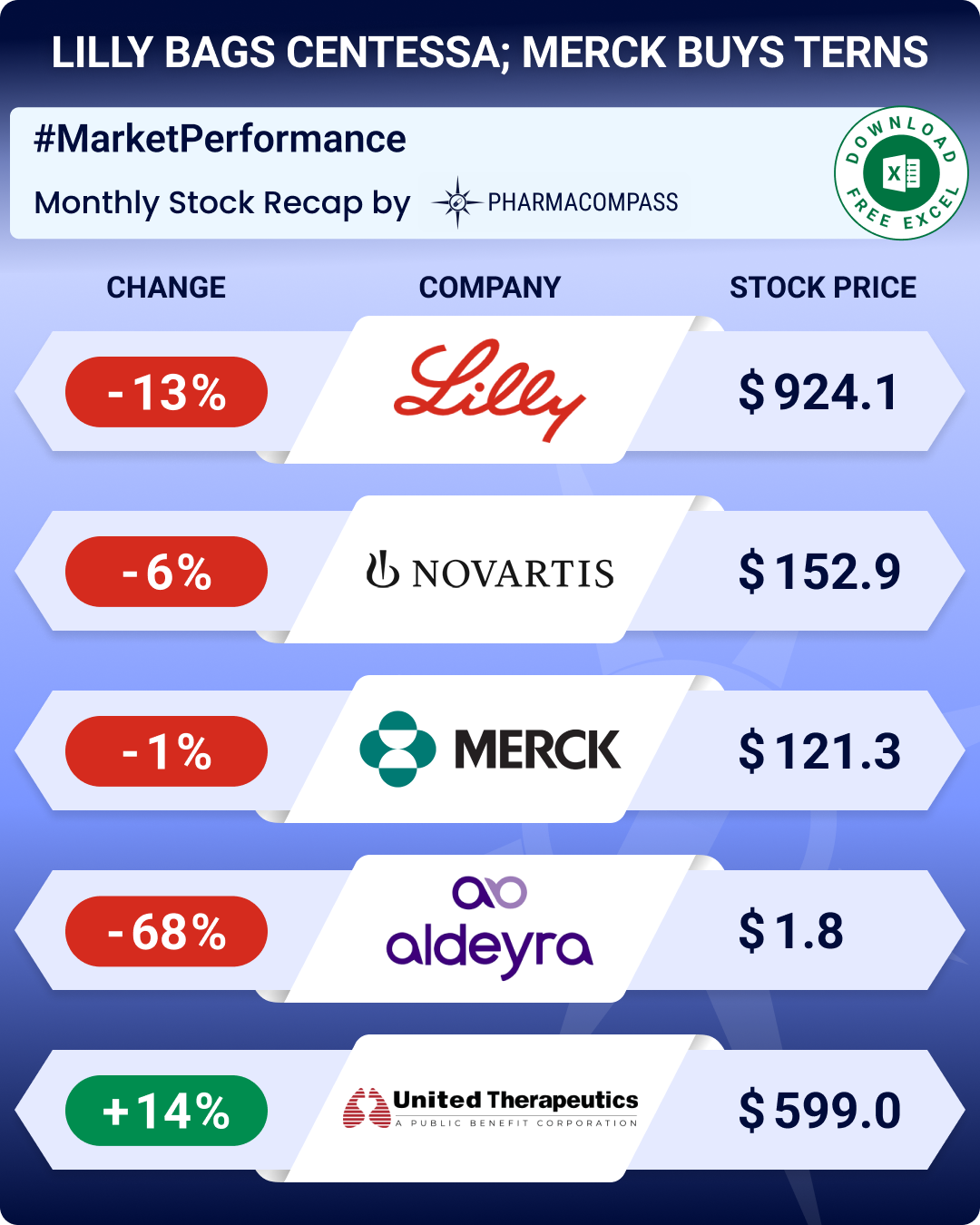

Pipeline Prospector March 2026 highlights: Lilly to acquire Centessa for US$ 7.8 bn; Merck buys Terns Pharma for US$ 6.7 bn

The

raging war in the Middle East has disrupted global pharmaceutical supply

chains, which are dep

Pipeline Prospector February 2026 highlights: Gilead buys Arcellx for US$ 7.8 bn; FDA okays Vanda’s psychotic pill

February

was a month of upheavals. In the US, the Supreme Court ruled that President Donald Trump

Pipeline Prospector Jan 2026 highlights: Astra, CSPC sign up to US$ 18.5 bn obesity deal; Wegovy’s pill version debuts in US

The

year 2026 began amid heightened geopolitical tensions, particularly over

Greenland. The US Pre

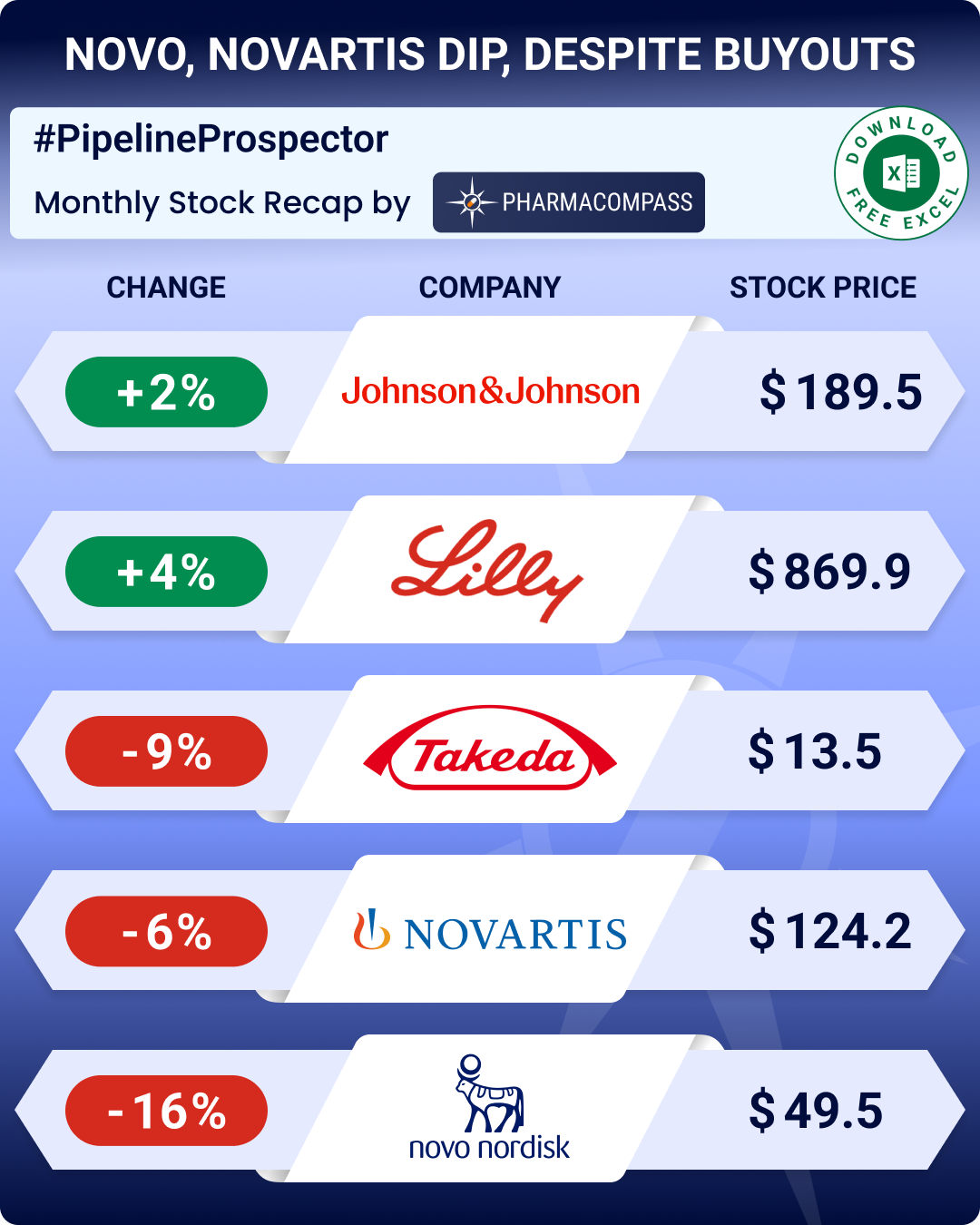

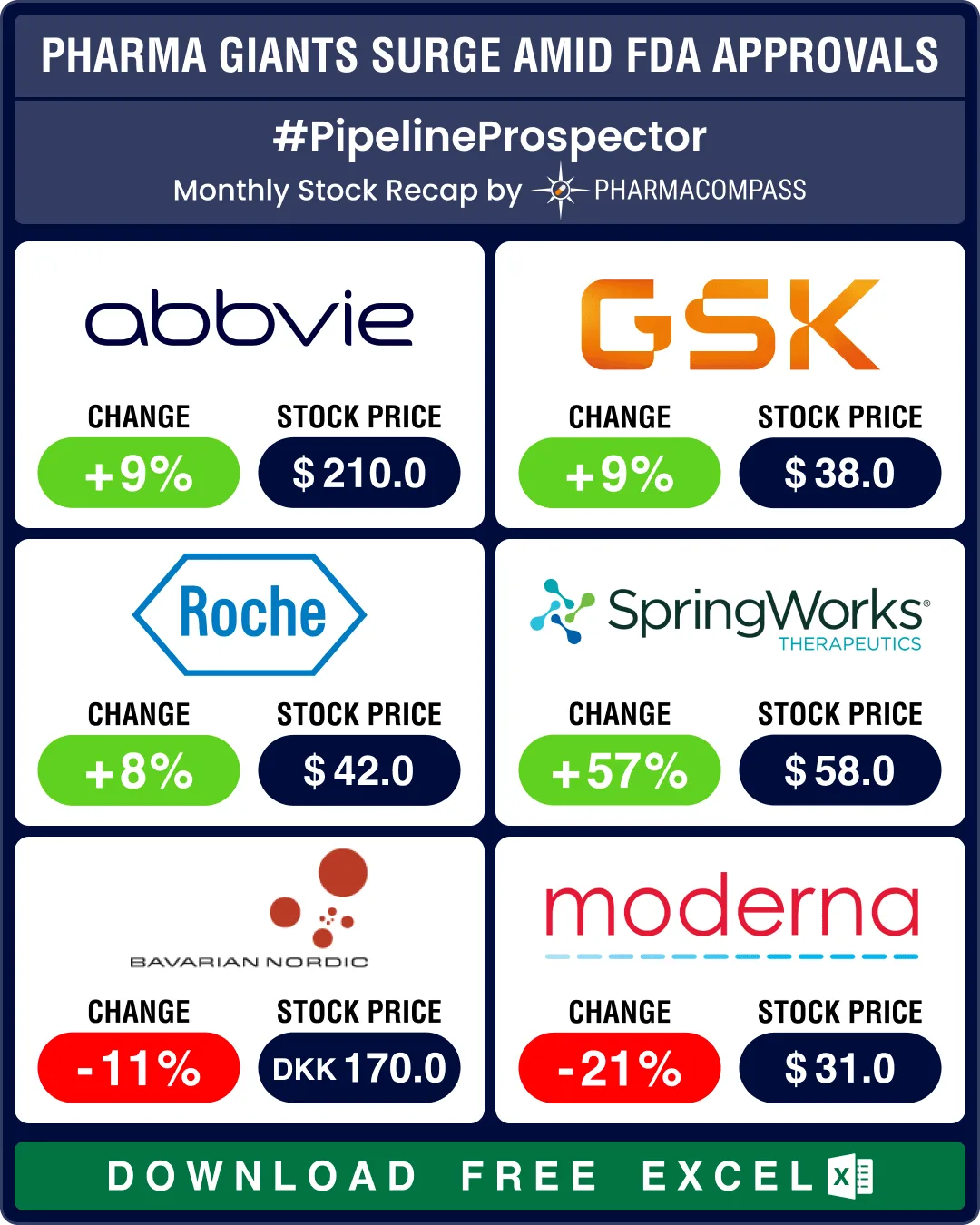

Pipeline Prospector 2025 highlights: FDA approves pill version of Novo’s Wegovy; BioMarin acquires Amicus for US$ 4.8 bn

Even though the biotech indices delivered strong gains through 2025, December closed on a muted note

Pipeline Prospector November 2025: Kimberly-Clark to buy Kenvue for US$ 48.7 bn; FDA approves Novartis’ gene therapy

November saw several big ticket

acquisitions across the consumer health and biopharma space, includ

Pipeline Prospector October 2025: Novartis to buy Avidity for US$ 12 bn; FDA approves Bayer’s med to treat hot flashes

October was abuzz

with dealmaking. Pharma majors such as Novartis, Novo Nordisk, and Bristol Myers

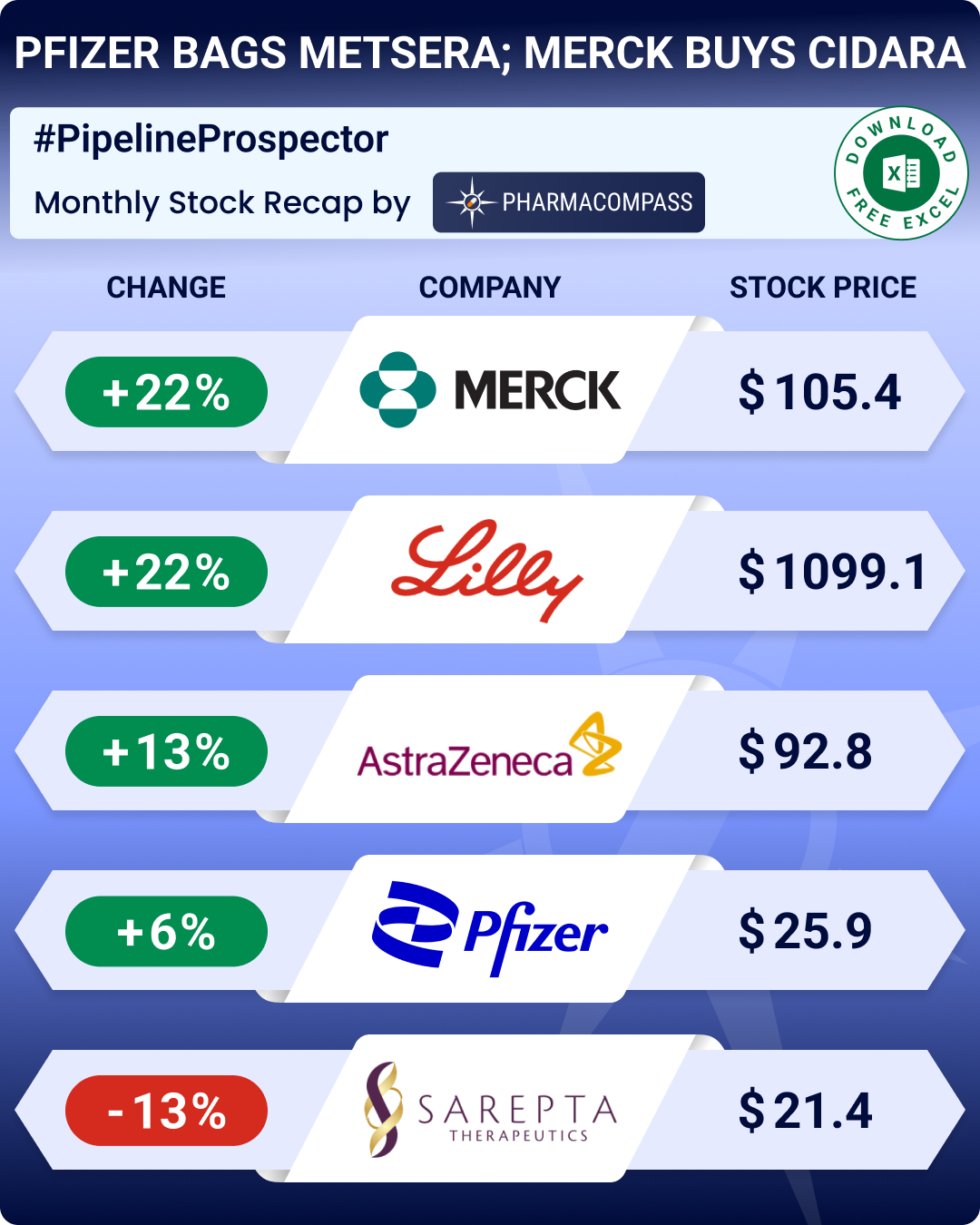

Pipeline Prospector September 2025: Genmab buys Merus for ~US$ 8 billion, Pfizer buys Metsera to enter obesity race

September saw a major clampdown on imports of “branded or patented drugs” into the US, t

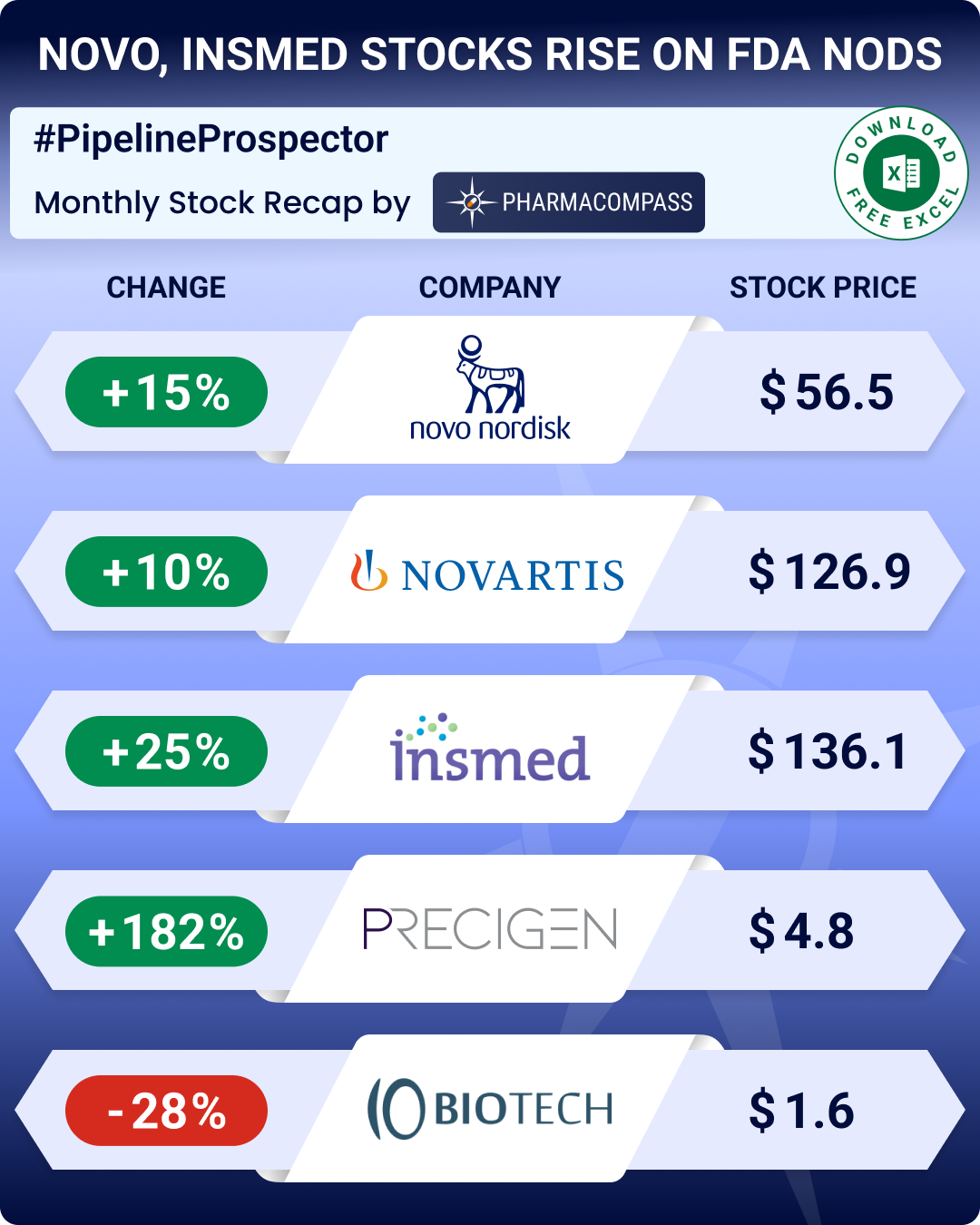

Pipeline Prospector August 2025: Novo’s Wegovy approved for MASH, Tonix Pharma’s fibromyalgia drug okayed

In

August, the global pharmaceutical industry witnessed several regulatory

upheavals and policy sh

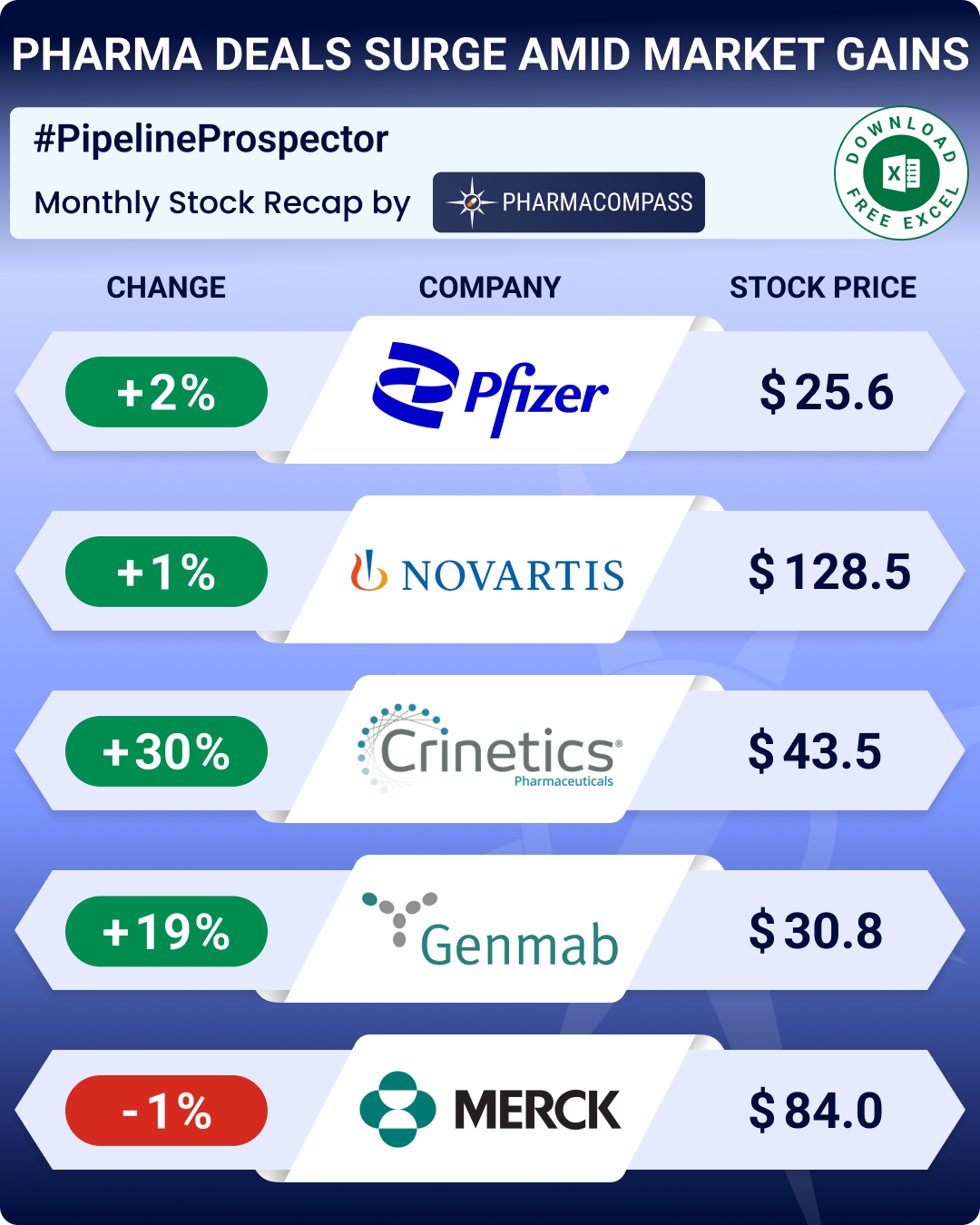

Pipeline Prospector July 2025: Merck to acquire Verona for US$ 10 bn; FDA okays Regeneron’s blood cancer med

In July, the pharmaceutical industry witnessed several deals and mergers and acquisitions (M&As). Bi

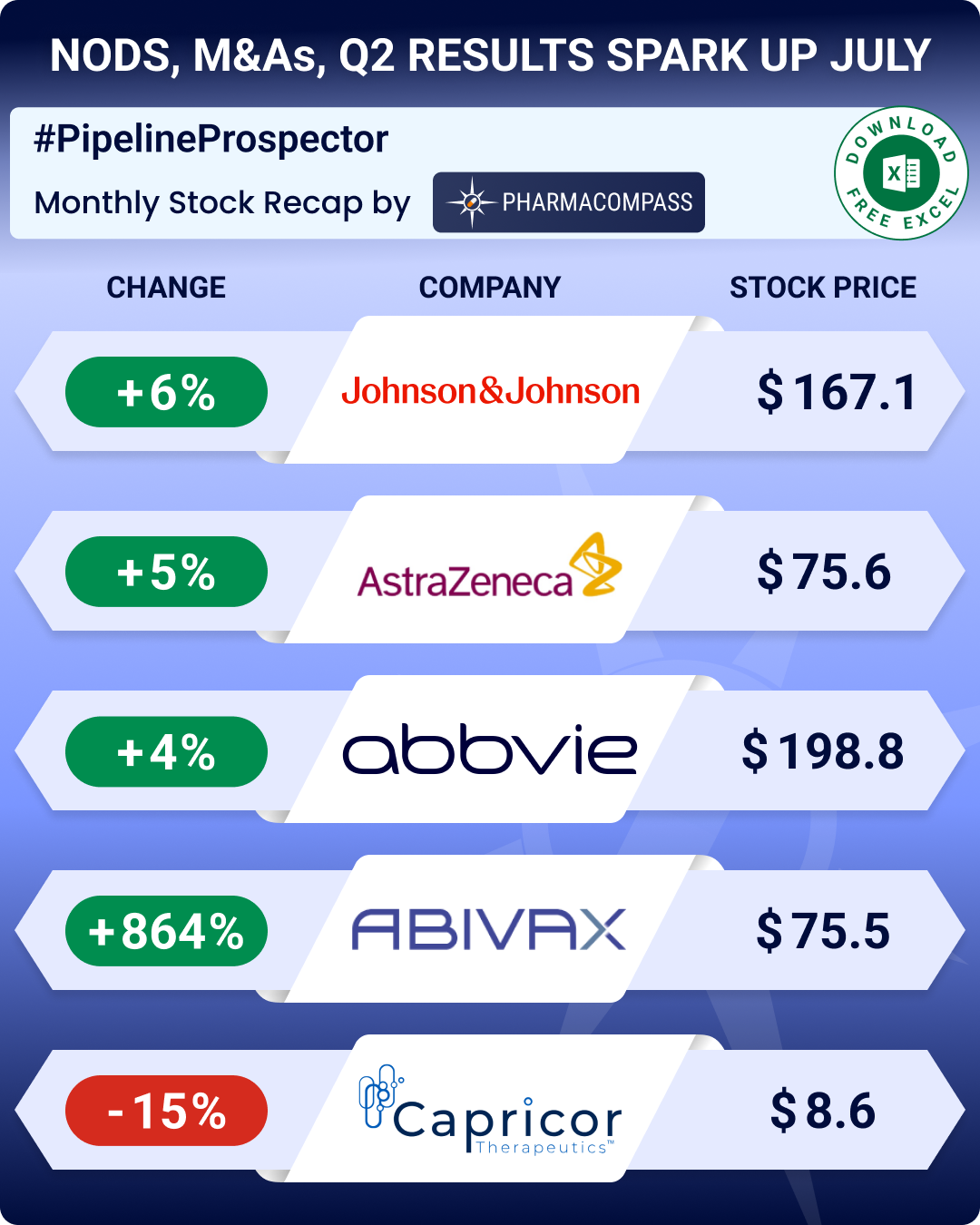

Pipeline Prospector June 2025: Sanofi, AbbVie, Eli Lilly, BioNTech lead pharma M&A spree; BMS, Astra ink major collaborations

In June, the pharmaceutical industry continued to witness more merger and acquisitions, deals, and g

Pipeline Prospector May 2025: Pfizer strikes US$ 6 bn oncology pact; Lilly diversifies pipeline with US$ 2.3 bn in deals

The month of May saw investors grow increasingly cautious. This resulted in a dip in the biotech ind

Pipeline Prospector April 2025: Merck KGaA buys SpringWorks for US$ 3.9 bn; Swiss giants lead pharma migration to US soil

April witnessed considerable volatility in pharmaceutical stocks as the US President Donald Trump&rs

Pipeline Prospector March 2025: Trump’s FDA overhaul spooks biotech stocks; Roche, AbbVie, Novo ink obesity drug deals

March ended with news that the top vaccine regulator of the US

Food and Drug Administration (FDA),

Pipeline Prospector Feb 2025: Bain buys Mitsubishi Tanabe for US$ 3.4 bn; Japan’s Ono gets FDA nod for rare joint tumor drug

February was a mixed bag for biopharma indices, underscoring the volatility and uncertainty in the s

Pipeline Prospector Jan 2025: J&J’s US$ 14.6 bn Intra-Cellular buyout kicks off deal frenzy; Ozempic clinches FDA nod for CKD

January was a busy month that saw several deals being announced at the JP Morgan Healthcare Conferen

Pipeline Prospector 2024 highlights: Rise in new breed of biotechs with maiden approvals; GLP-1 meds show promise beyond obesity

December proved to be one of the most bearish months of 2024 for the biopharma sector. The Nasdaq Bi

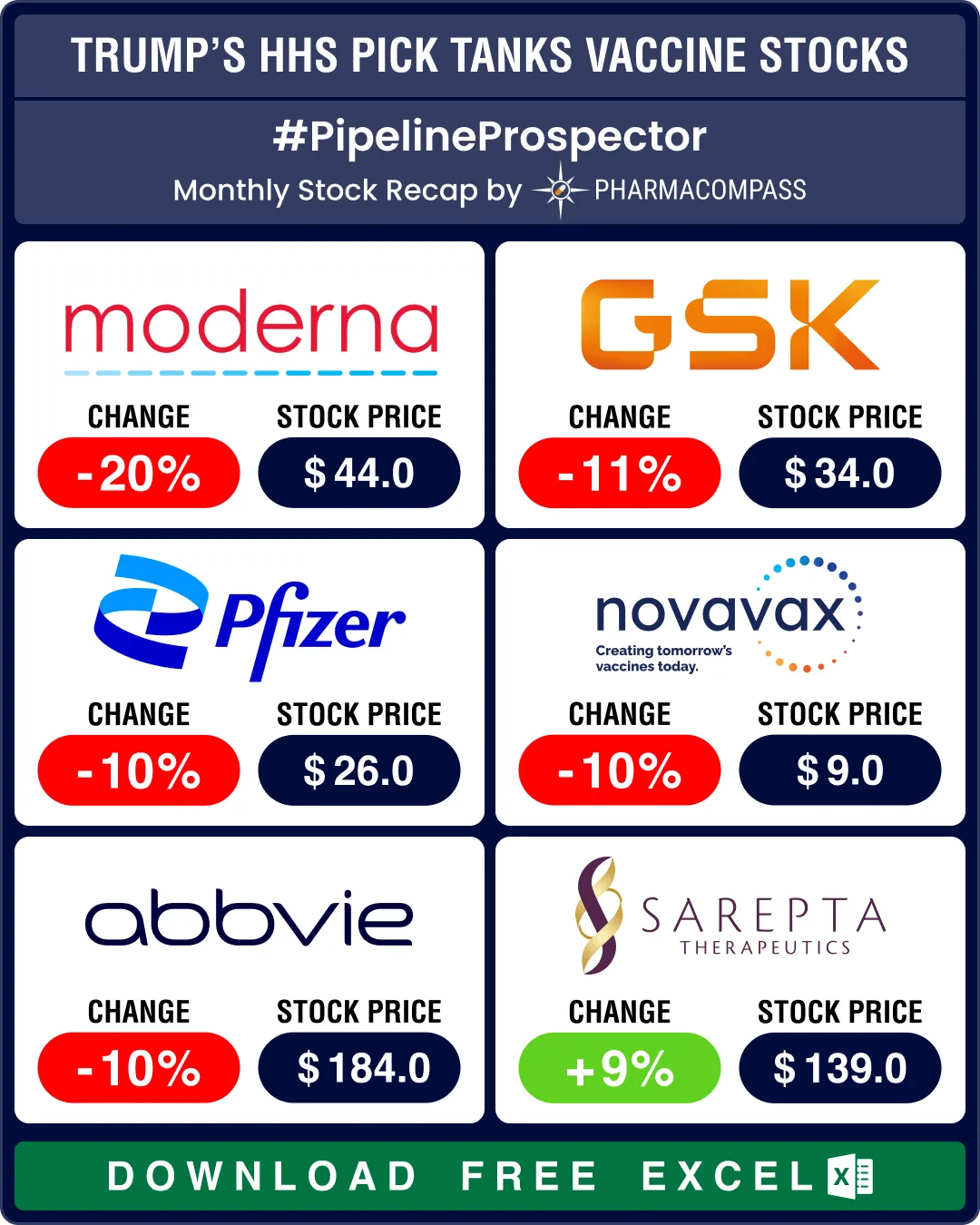

Pipeline Prospector Nov 2024: Trump’s HHS pick drags down jab makers’ stocks; Novartis, Merck, Roche ink billion-dollar deals

In November, the markets responded to US President-elect Donald Trump’s picks, particularly th

Pipeline Prospector Oct 2024: Lundbeck acquires Longboard for US$ 2.6 bn; molecular glue degrader tech witnesses dealmaking

In October, several pharma companies posted their third quarter (Q3) results. Drugmakers like Pfizer

Pipeline Prospector Sept 2024: BMS wins landmark FDA approval for schizophrenia med; Sanofi’s Dupixent okayed for COPD

Pharma indices settled slightly lower in September after four months of solid gains. The three major

Pipeline Prospector Aug 2024: Otsuka buys Jnana, Lilly’s market cap gains by over US$ 108 bn post new guidance

As summer draws to a close, pharma and biotech indices posted their fourth consecutive month in the

Pipeline Prospector July 2024: Indices continue to climb; Lilly buys Morphic for US$ 3.2 bn, Kisunla bags FDA nod

The biotechnology sector ended in the green for the third month in a row in July, significantly outp

Pipeline Prospector June 2024: FDA approves Merck’s next-gen pneumococcal vaccine, Verona’s COPD therapy

The pharma indices were back in the black in May, and the good streak continued through June with th

Pipeline Prospector May 2024: J&J inks two deals for eczema drugs; Novo scores trial wins in hemophilia, kidney disease

Pharma indices have rebounded after ending March and April in the red. May saw the Nasdaq Biotechnol

Pipeline Prospector April 2024: Indices dip amid muted Q1 results; Vertex acquires Alpine Immune for US$ 4.9 bn

Pharma indices had begun to recede in March. Their red streak accelerated in April with the Nasdaq B

Pipeline Prospector March 2024: FDA approves pathbreaking NASH drug from Madrigal, two meds for PAH

March was clearly a month of drug approvals, as the US Food and

Drug Administration (FDA) went on a

Pipeline Prospector Feb 2024: Novo’s parent buys Catalent for US$ 16.5 bn, FDA okays Iovance’s cell therapy

February was a good month for the pharma sector, complete with some important deals, successes from

Pipeline Prospector Jan 2024: Vertex’s non-opioid painkiller succeeds in trials; Sanofi buys Inhibrx for US$ 2.2 bn

The New Year got off to a stable start, with some good news

trickling in from clinical trials and B

- Privacy policy

- Terms and conditions

- Disclaimers

-

- Product listings are provided for informational purposes only. We do not supply or sell any products. Any products that may be covered by patent(s) are supplied solely for uses permitted under Section 107A of the Indian Patents Act and not for commercial sale.