BLOG

MARKET INTEL by PharmaCompass

CONTENT by Suppliers

- Interview #SpeakPharma

- Video #SupplierSpotlight

- Vlog #PharmaReel

- Company Bio #AboutSupplier

- Services Bio #AboutCapabilities

News

Create content with us, ask us

By PharmaCompass

2024-08-22

Impressions: 5089

The world of pharmaceuticals and biotechnology continued to evolve this year with strategic alliances reshaping industry contours. With mid-size deals taking centerstage, the growth trajectory appears to be marked by a balance of both caution and calculated ambition.

The deal-making environment was robust in 2023, with over 2,000 unique pharma and biotech deals totaling more than US$ 410 billion, according to the PharmaCompass database. Last year, there were over 200 mergers and acquisitions (M&As) with transactions exceeding US$ 160 billion in total value. Oncology, infections and infectious diseases, and neurology had emerged as the top three therapeutic areas for deals.

PharmaCompass’ analysis indicates that the momentum has been maintained in 2024. As of August 6, the industry had seen over 1,200 unique deals valued at more than US$ 230 billion, including over 120 M&A transactions surpassing US$ 60 billion in aggregate value. While oncology maintains its lead position, neurology and immunology have gained notable traction.

The one big difference is that 2024 is yet to witness a mega-deal, comparable to Pfizer’s US$ 43 billion acquisition of Seagen in 2023 or Amgen’s US$ 27.8 billion Horizon buyout announced in 2022. The largest transaction thus far has been Novo Nordisk Foundation’s US$ 16.5 billion acquisition of Catalent, a contract development and manufacturing organization (CDMO).

This compilation does not include deals related to acquisition of facilities, divestment, medical devices, diagnostics and animal health. We have considered deals announced, irrespective of when these transactions were completed. For a comprehensive overview of CDMO deals and developments in 2024, please refer to our dedicated roundup.

View Pharma & Biotech Acquisitions, Deals & Agreements in 2024 as of Aug. 6 (Free Excel Available)

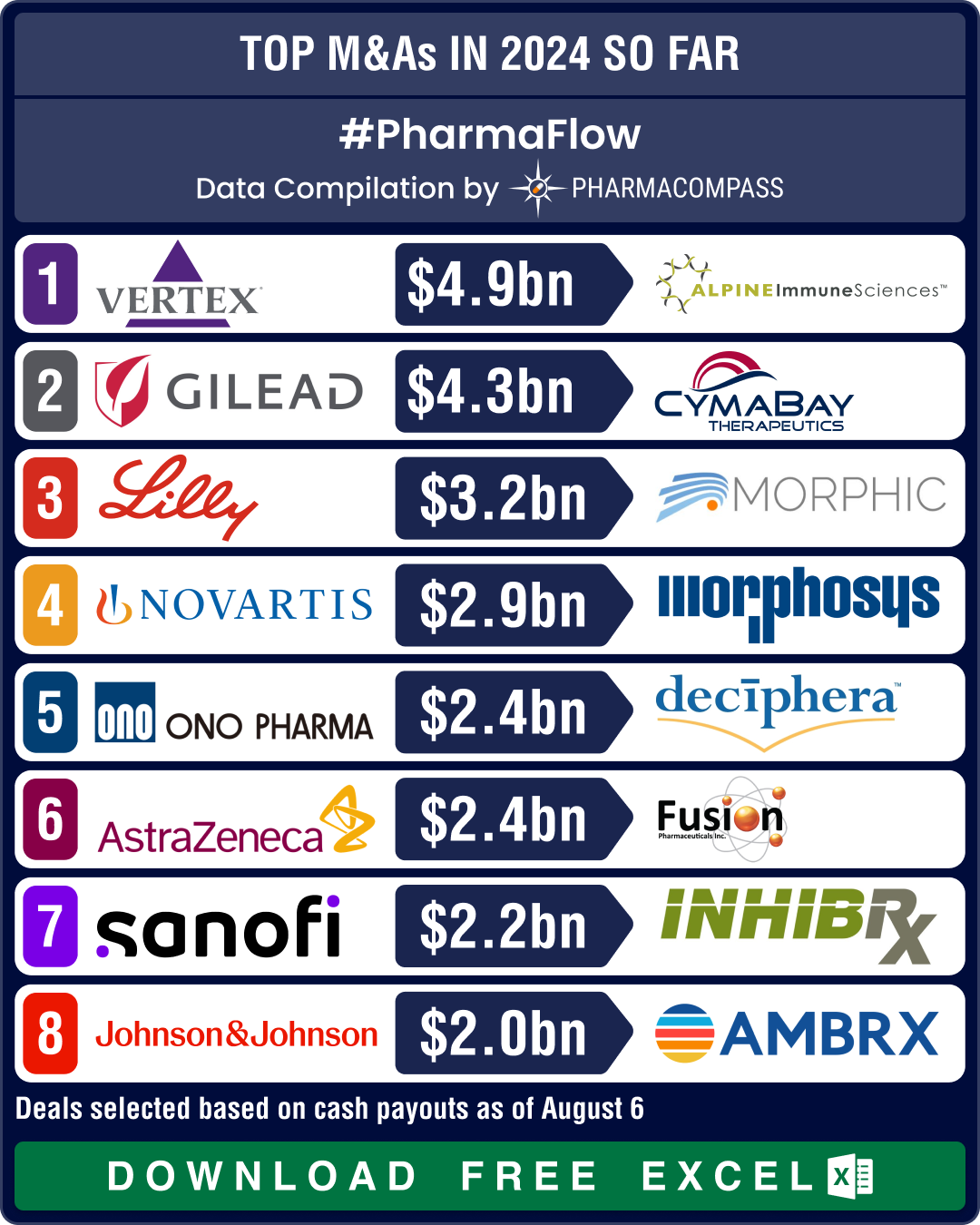

Vertex buys Alpine Immune for US$ 4.9 bn; Gilead’s CymaBay buyout pays off via FDA nod

Amongst the biggest acquisitions of 2024 was Vertex Pharmaceuticals’ buyout of Alpine Immune Sciences for US$ 4.9 billion. It granted Vertex access to protein-based immunotherapies, including the promising povetacicept for IgA nephropathy, a serious kidney disease.

Gilead Sciences’ acquisition of CymaBay Therapeutics for US$ 4.3 billion in February secured it access to seladelpar (Livdelzi), an experimental drug that received FDA’s accelerated approval this month for primary biliary cholangitis, a liver disease that affects the bile ducts.

Eli Lilly bolstered its presence in the US$ 26.65 billion inflammatory bowel disease (IBD) market by purchasing Morphic Holding for approximately US$ 3.2 billion in July. Through this deal, Lilly gained the oral IBD therapy candidate MORF-057, which will offer a more convenient dosing option compared to injectable drugs currently available in the market. Lilly sees the IBD space as a way to diversify beyond obesity.

Merck expanded its ophthalmology portfolio by acquiring Eyebiotech Limited for US$ 1.3 billion (plus US$ 1.7 billion in milestone payments), obtaining Restoret for diabetic macular edema and neovascular age-related macular degeneration.

Japanese drugmaker Ono Pharmaceutical acquired Deciphera Pharmaceuticals for US$ 2.4 billion, gaining Qinlock for gastrointestinal stromal tumors and vimseltinib for tenosynovial giant cell tumors. Sanofi targeted rare diseases by purchasing Inhibrx for up to US$ 2.2 billion. The acquisition gave the French drugmaker access to INBRX-101 for Alpha-1 antitrypsin deficiency, a genetic condition that can cause lung and liver damage.

View Pharma & Biotech Acquisitions, Deals & Agreements in 2024 as of Aug. 6 (Free Excel Available)

Novartis buys two oncology firms for their assets; J&J, Genmab join ADC bandwagon

Novartis has been on a shopping spree, and has made two significant purchases this year. First, it acquired MorphoSys for € 2.7 billion (US$ 2.9 billion), thereby adding the promising bone-marrow cancer treatment pelabresib to its pipeline. Second, it announced the acquisition of Mariana Oncology for US$ 1 billion upfront (plus US$ 750 million in milestone payments), thereby expanding into radioligand therapies (RLTs) to treat cancers with high unmet need. RLTs take a targeted approach, delivering radiation to the tumor, while limiting damage to the surrounding cells.

AstraZeneca entered the field of radioconjugates, which is a promising modality in the treatment of cancer, by acquiring Fusion Pharmaceuticals for US$ 2.4 billion.

In January this year, Johnson & Johnson had announced the acquisition of antibody-drug-conjugate (ADC) developer Ambrx Biopharma for about US$ 2 billion. With this buyout, J&J has joined the likes of Bristol Myers Squibb, AbbVie and GSK who had entered this promising field through acquisitions last year.

Similarly, Denmark’s Genmab bought ProfoundBio for US$ 1.8 billion in cash, boosting its oncology portfolio with three next-generation ADC candidates. This includes Rina-S, which recently received FDA’s fast track designation for the treatment of ovarian cancer.

View Pharma & Biotech Acquisitions, Deals & Agreements in 2024 as of Aug. 6 (Free Excel Available)

Novartis signs multiple collaborations; GSK, Takeda, AbbVie sign billion-dollar deals

Novartis was not just busy signing M&A deals, it also signed a bevy of collaboration agreements. For instance, Shanghai-based Argo partnered Novartis on two early-stage RNA interference candidates for cardiovascular diseases, potentially earning the former up to US$ 4.2 billion plus tiered royalties.

Novartis also agreed to pay up to US$ 3 billion (including US$ 150 million upfront) to Dren Bio to use the latter’s Targeted Myeloid Engager and Phagocytosis platform to develop bispecific antibodies to treat cancer.

Moreover, the Swiss drugmaker expanded its peptide discovery collaboration with Japan-based PeptiDream in a deal worth over US$ 2.71 billion in milestone payments, plus an upfront payment of US$ 180 million. Peptide-drug conjugates (PDCs) are the next generation of targeted therapeutic drugs after ADCs and Novartis is, thus far, the only big pharma with FDA-approved radioligand PDCs.

GSK entered a groundbreaking partnership with Flagship Pioneering, potentially worth over US$ 7 billion, to identify and develop 10 novel drugs and vaccines. The deal, starting with respiratory and immunology drugs, involves US$ 720 million in upfront and milestone payments for each candidate. This collaboration leverages Flagship’s extensive portfolio of over 40 biopharma companies with drug development capabilities.

There were two significant deals in the field of neuroscience. First, Takeda said it is paying Swiss biotech AC Immune US$ 100 million upfront with potential further payments of US$ 2.1 billion for an exclusive option to license global rights to an Alzheimer’s vaccine and related immunotherapies.

Second, AbbVie and clinical stage biotech Gilgamesh Pharmaceuticals joined forces in a deal potentially worth over US$ 2 billion to develop a new class of psychedelic compounds for psychiatric conditions, combining AbbVie’s psychiatric expertise with Gilgamesh’s innovative neuroplastogen research platform.

View Pharma & Biotech Acquisitions, Deals & Agreements in 2024 as of Aug. 6 (Free Excel Available)

Our view

During this year, companies like Novartis (with US$ 16.8 billion), GSK (US$ 14.5 billion), Sanofi (US$ 11.9 billion), Bristol Myers Squibb (US$ 11.6 billion), and AbbVie (US$ 9.1 billion) have made substantial investments in acquisitions, collaborations and other forms of dealmaking.

Though the deal-making environment is robust, we notice a shift towards mid-size transactions. Alongside, we notice a growing interest in areas such as ADCs, radiopharmaceuticals, and protein-based immunotherapies, underscoring their growing importance in drug development. There has also been significant interest in silencing RNA (siRNA) therapeutics, highlighting the industry's focus on novel approaches to disease treatment. With the industry focusing on cutting-edge technologies that address unmet medical needs, we feel there is little reason to fret over the size of the deals.

The PharmaCompass Newsletter – Sign Up, Stay Ahead

Feedback, help us to improve. Click here

Image Credit : Top M&A deals in 2024 by PharmaCompass license under CC BY 2.0

“ The article is based on the information available in public and which the author believes to be true. The author is not disseminating any information, which the author believes or knows, is confidential or in conflict with the privacy of any person. The views expressed or information supplied through this article is mere opinion and observation of the author. The author does not intend to defame, insult or, cause loss or damage to anyone, in any manner, through this article.”