Acquisitions and spin-offs dominated headlines in 2019 and the tone was set very early with Bristol-Myers Squibb acquiring

New Jersey-based cancer drug company Celgene in a US$ 74 billion deal announced on

January 3, 2019. After factoring

in debt, the deal value ballooned to about US$ 95 billion, which according

to data compiled by Refinitiv, made it the largest healthcare deal on

record.

In the summer, AbbVie Inc,

which sells the world’s best-selling drug Humira, announced its acquisition of Allergan Plc, known for Botox and other cosmetic

treatments, for US$ 63 billion. While the companies are still awaiting

regulatory approval for their deal, with US$ 49 billion in combined 2019

revenues, the merged entity would rank amongst the biggest in the industry.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

The big five by pharmaceutical sales — Pfizer,

Roche, J&J, Novartis and Merck

Pfizer

continued

to lead companies by pharmaceutical sales by reporting annual 2019 revenues of

US$ 51.8 billion, a decrease of US$ 1.9 billion, or 4 percent, compared to

2018. The decline was primarily attributed to the loss of exclusivity of Lyrica in 2019,

which witnessed its sales drop from US$ 5 billion in 2018 to US$ 3.3 billion in

2019.

In 2018, Pfizer’s then incoming CEO Albert Bourla had mentioned that the company did not see the need for any large-scale M&A activity as Pfizer had “the best pipeline” in its history, which needed the company to focus on deploying its capital to keep its pipeline flowing and execute on its drug launches.

Bourla stayed true to his word and barring the acquisition of Array Biopharma for US$ 11.4 billion and a spin-off to merge Upjohn, Pfizer’s off-patent branded and generic established medicines business with

Mylan, there weren’t any other big ticket deals which were announced.

The

Upjohn-Mylan merged entity will be called Viatris and is expected to have 2020

revenues between US$ 19 and US$ 20 billion

and could outpace Teva to

become the largest generic company in the world, in term of revenues.

Novartis, which had

followed Pfizer with the second largest revenues in the pharmaceutical industry

in 2018, reported its first full year earnings after spinning off its Alcon eye

care devices business division that

had US$ 7.15 billion in 2018 sales.

In 2019,

Novartis slipped two spots in the ranking after reporting total sales of US$

47.4 billion and its CEO Vas Narasimhan continued his deal-making spree by buying New

Jersey-headquartered The Medicines Company (MedCo) for US$ 9.7

billion to acquire a late-stage cholesterol-lowering

therapy named inclisiran.

As Takeda Pharmaceutical Co was

busy in 2019 on working to reduce its debt burden incurred due to its US$ 62

billion purchase of Shire Plc, which was announced in 2018, Novartis also purchased

the eye-disease medicine, Xiidra, from the Japanese drugmaker for US$ 5.3 billion.

Novartis’ management also spent a considerable part of 2019 dealing with data-integrity concerns which emerged from its 2018 buyout of AveXis, the

gene-therapy maker Novartis had acquired for US$ 8.7 billion.

The deal gave Novartis rights to Zolgensma,

a novel treatment intended for children less than two years of age with the

most severe form of spinal muscular atrophy (SMA). Priced at US$ 2.1 million,

Zolgensma is currently the world’s most expensive drug.

However,

in a shocking announcement, a month after approving the drug, the US Food and

Drug Administration (FDA) issued a press release on

data accuracy issues as the agency was informed by AveXis that

its personnel had manipulated data which

the FDA used to evaluate product comparability and nonclinical (animal)

pharmacology as part of the biologics license application (BLA), which was

submitted and reviewed by the FDA.

With US$

50.0 billion (CHF 48.5 billion) in annual pharmaceutical sales, Swiss drugmaker

Roche came in at number two position in 2019

as its sales grew 11 percent driven by

its multiple sclerosis medicine Ocrevus, haemophilia drug Hemlibra and cancer medicines Tecentriq and Perjeta.

Roche’s newly introduced medicines generated US$ 5.53 billion (CHF 5.4 billion) in growth, helping offset the impact of the competition from biosimilars for its three best-selling drugs MabThera/Rituxan, Herceptin and Avastin.

In late 2019, after months of increased

antitrust scrutiny, Roche completed

its US$ 5.1 billion acquisition of Spark Therapeutics to strengthen its presence in

gene therapy.

Last year, J&J reported almost flat worldwide sales of US$ 82.1 billion. J&J’s pharmaceutical division generated US$ 42.20 billion and its medical devices and consumer health divisions brought in US$ 25.96 billion and US$ 13.89 billion respectively.

Since J&J’s consumer health division sells analgesics, digestive health along with beauty and oral care products, the US$ 5.43 billion in consumer health sales from over-the-counter drugs and women’s health products was only used in our assessment of J&J’s total pharmaceutical revenues. With combined pharmaceutical sales of US$ 47.63 billion, J&J made it to number three on our list.

While the sales of products like Stelara, Darzalex, Imbruvica, Invega Sustenna drove J&J’s pharmaceutical business to grow by 4 percent over 2018, the firm had to contend with generic competition against key revenue contributors Remicade and Zytiga.

US-headquartered Merck, which is known as

MSD (short for Merck Sharp & Dohme) outside the United States and

Canada, is set to significantly move up the rankings next year fueled by its

cancer drug Keytruda, which witnessed a 55

percent increase in sales to US$ 11.1 billion.

Merck reported total revenues of US$ 41.75 billion and also

announced it will spin off its women’s health drugs,

biosimilar drugs and older products to create a new pharmaceutical

company with US$ 6.5 billion in annual revenues.

The firm had anticipated 2020 sales between US$ 48.8 billion and US$ 50.3 billion however this week it announced that the coronavirus pandemic will reduce 2020 sales by more than $2 billion.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Humira holds on to remain world’s best-selling drug

AbbVie’s acquisition of Allergan comes as the firm faces the expiration of patent protection for Humira, which brought in a staggering US$ 19.2 billion in sales last year for

the company. AbbVie has failed to successfully acquire or develop a major new

product to replace the sales generated by its flagship drug.

In 2019, Humira’s US revenues increased 8.6 percent to US$ 14.86 billion while internationally, due

to biosimilar competition, the sales dropped 31.1 percent to US$ 4.30 billion.

Bristol Myers Squibb’s Eliquis, which is also marketed by Pfizer, maintained its number two position

and posted total sales of US$ 12.1 billion, a 23 percent increase over 2018.

While Bristol Myers Squibb’s immunotherapy treatment Opdivo, sold in partnership with Ono in Japan, saw sales increase from US$ 7.57 billion to US$ 8.0 billion, the growth paled in comparison to the US$ 3.9

billion revenue increase of Opdivo’s key immunotherapy competitor Merck’s Keytruda.

Keytruda took the number three spot in drug sales that

previously belonged to Celgene’s Revlimid, which witnessed a sales decline from US$ 9.69 billion to US$ 9.4 billion.

Cancer treatment Imbruvica, which is marketed

by J&J and AbbVie, witnessed a 30 percent increase in sales. With US$ 8.1

billion in 2019 revenues, it took the number five position.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Vaccines – Covid-19 turns competitors into partners

This year has been dominated by the single biggest health emergency in years — the novel coronavirus (Covid-19) pandemic. As drugs continue to fail to meet expectations, vaccine development has received a lot of attention.

GSK reported the highest vaccine sales of all drugmakers with

total sales of US$ 8.4 billion (GBP 7.16 billion), a significant portion of its

total sales of US$ 41.8 billion (GBP 33.754 billion).

US-based Merck’s vaccine division also reported a significant increase in sales to US$ 8.0 billion and in 2019 received FDA and EU approval to market its Ebola vaccine Ervebo.

This is the first FDA-authorized vaccine against the deadly virus which causes

hemorrhagic fever and spreads from person to person through direct contact with

body fluids.

Pfizer and Sanofi also reported an increase in their vaccine sales to US$ 6.4

billion and US$ 6.2 billion respectively and the Covid-19 pandemic has recently

pushed drugmakers to move faster than ever before and has also converted

competitors into partners.

In a rare move, drug behemoths — Sanofi and GlaxoSmithKline (GSK) —joined hands to develop a vaccine for the novel coronavirus.

The two companies plan to start human trials

in the second half of this year, and if things go right, they will file

for potential approvals by the second half of 2021.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Our view

Covid-19 has brought the world economy to a grinding halt and shifted the global attention to the pharmaceutical industry’s capability to deliver solutions to address this pandemic.

Our compilation shows that vaccines and drugs

for infectious diseases currently form a tiny fraction of the total sales of

pharmaceutical companies and few drugs against infectious diseases rank high on

the sales list.

This could well explain the limited range of

options currently available to fight Covid-19. With the pandemic currently infecting

over 3 million people spread across more than 200 countries, we can safely

conclude that the scenario in 2020 will change substantially. And so should our

compilation of top drugs for the year.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Impressions: 54752

https://www.pharmacompass.com/radio-compass-blog/top-drugs-and-pharmaceutical-companies-of-2019-by-revenues

#PharmaFlow by PHARMACOMPASS

29 Apr 2020

The year 2017 was a landmark year for pharmaceutical

industries in the US and Europe, with a sharp increase in the number of new molecular entities (NMEs) being approved in both geographies.

The US Food

and Drug Administration (USFDA) approved 46 NMEs in 2017, the second highest

since 1996 when 53 NMEs were approved. In Europe, the European Medicines Agency

(EMA) approved 35 drugs with a new active substance, up from 27 in 2016.

Sales for most major pharmaceutical

companies continued to grow in 2017. Earnings forecasts for 2018 have been raised due to the recent US tax reform that has

generated investor hopes for accelerated dividend growth and share buyback

plans.

This week, PharmaCompass brings

you a compilation of the top drugs of 2017 by sales revenue.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

Top-sellers: Humira races ahead, despite launch of biosimilars; Enbrel a distant second

There wasn’t any upheaval

at the top of the pharma drug sales charts. AbbVie’s anti-TNF (tumor necrosis factor) giant

Humira (adalimumab), which is approved to treat

psoriasis and rheumatoid arthritis, added

almost another US $3 billion to its 2016 sales and posted nearly US $19 billion in revenues.

Last year, AbbVie’s raised expectations for Humira’s earnings to reach US $21 billion in global sales by 2020. The

company believes this drug will continue to be a significant cash contributor

until 2025 and the US $21 billion sales forecast

by 2020 is about US $3 billion higher than its expectation two years ago.

In 2016, the US Food and Drug Administration

(FDA) approved Amgen’s Amjevita (adalimumab-atto) — a biosimilar of Humira. And in 2017, another Humira biosimilar — Boehringer Ingelheim’s Cyltezo

(adalimumab-adbm) — received approval from the FDA and European authorities.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

Enbrel (etanercept),

the longest-used biologic medicine for the treatment of rheumatism around the

world, was the second best-selling drug with US $8.262 billion in 2017 sales.

The sales of the drug were down from US $9.366 billion in

2016 owing to lower selling prices and increased

competition, which in turn hurt demand.

Since it was first approved in the United States in 1998,

Enbrel has been approved in over 100 countries and the drug is promoted by Amgen,

Pfizer

and Takeda

in different geographies.

Novartis’ biosimilar copy of Enbrel, which got approved by the FDA in August

2016 for the treatment of patients with

rheumatoid arthritis (RA), plaque psoriasis, ankylosing spondylitis (AS) and

other diseases is still not on the market because of a patent-protection

challenge from Amgen.

Amgen is arguing in the US federal court

that its drug has patent protection until 2029.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

Fast-growing drugs: Eylea and Revlimid bring

fortunes for Regeneron and Celgene

Regeneron’s

flagship eye treatment, Eylea (aflibercept) which is marketed by Bayer outside the United States, added another US $1 billion in

annual sales last year to record US $8.260 billion in total sales. Eylea net

sales grew 11 percent year-on-year in the US and 19 percent year-over-year

outside the US.

The company believes much of the recent

growth in the US was driven by demographic trends with an aging population as

well as an overall increase in the prevalence of diabetes.

These demographic trends are expected to

continue in the coming years, providing an opportunity for continued growth.

Eylea sales alone contribute 63 percent to Regeneron’s total sales.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

Celgene’s

Revlimid

(lenalidomide)

— a thalidomide derivative introduced in 2004 as an immunomodulatory agent for the treatment of various cancers such as multiple myeloma — brought in an additional US $1.2 billion in 2017 sales and had total revenues of US $8.187 billion.

Revlimid continues to contribute more than 60 percent to the company’s total sales of US $13 billion.

Celgene received a setback this month as the

USFDA refused to consider Celgene’s

application for ozanimod, an experimental

treatment for relapsing multiple sclerosis. The treatment was being seen as a

key to the company’s fortunes as Celgene had

said ozanimod is worth US $4 billion to

US $6

billion a year in peak sales.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

Gilead’s Hepatitis C franchise enters free fall

Gilead Sciences’ blockbuster hepatitis C drugs franchise that includes Sovaldi and Harvoni continue to feel the

competitive heat as they registered US $9.137

billion in 2017 sales, down from US $14.834

billion the previous year.

While reporting 2017 results, Gilead provided guidance for

2018 and said its sales of Hepatitis C drugs could fall

further to US $3.5 billion - US $4 billion. At their peak in 2015, Gilead’s Sovaldi and Harvoni had together generated

US $19.1 billion in sales.

One of the major reasons for this drop is AbbVie’s launch of its new treatment Mavyret

at a deep price discount to the competition. AbbVie

also claims to have the shortest treatment course at eight weeks, compared with

12 weeks or longer for other treatments.

AbbVie reported US $1.274 billion in Hepatitis C drug sales

in 2017, down from US $1.522 billion in 2016.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

Novartis’ Gleevec, Merck’s cardiovascular drugs, GSK’s Advair face generic heat

Novartis’ Gleevec (imatinib), which had at one point become the best-selling drug for Novartis and had brought in US $3.323 billion for the company in 2016, started facing generic competition last year and the anti-cancer drug lost US $1.380 billion in sales to bring in ‘only’ US $1.943 billion last year.

The US patents of Merck’s cardiovascular drugs — Zetia (Ezetimibe)

and Vytorin (Ezetimibe

and Simvastatin) — expired in April 2017. In May 2010, Merck and Glenmark

Pharmaceuticals entered into an agreement that allowed Glenmark to launch

a generic version of Zetia in late 2016. The drugs

that had combined sales of US $3.701

billion in 2016 felt the generic heat in 2017 and the sales were US

$1.606 billion lower at US $2.095

billion.

Click here to Access All the 2017 Data (Excel

version available) for FREE!

GSK’s Advair, which was expected

to encounter generic competition in 2017, continued to breathe easy as the FDA

found deficiencies in the applications of Hikma, Mylan and Sandoz.

All three failed to get the FDA nod for their generic versions of Advair, a drug used in the management of asthma and chronic obstructive pulmonary disease that generated sales worth US $4.431 billion (£3.130 billion) in 2017.

Top 15 drugs by sales

Here is PharmaCompass’ compilation

of the best-selling drugs of 2017. This is based on information extracted from

annual reports and US Securities and Exchange Commission (SEC) filings of major

pharmaceutical companies.

If you would like your own copy of all the information we’ve collected, email us at support@pharmacompass.com and we’ll send you an Excel version.

Click here to access all the 2017 data (Excel

version available) for FREE!

S. No.

Company / Companies

Product Name

Active Ingredient

Main Therapeutic Indication

2017 Revenue in Millions (USD)

1

AbbVie Inc., Eisai

Humira®

Adalimumab

Immunology (Organ Transplant, Arthritis etc.)

18,946

2

Amgen, Pfizer Inc., Takeda

Enbrel®

Etanercept

Immunology (Organ Transplant, Arthritis etc.)

8,262

3

Regeneron, Bayer

Eylea

Aflibercept

Ophthalmology

8,260

4

Celgene

Revlimid

Lenalidomide

Oncology

8,187

5

Roche

MabThera®/Rituxan®

Rituximab

Oncology

7,831

6

Johnson & Johnson, Merck, Mitsubishi Tanabe

Remicade®

Infliximab

Autoimmune Disorders

7,784

7

Roche

Herceptin®

Trastuzumab

Oncology

7,435

8

Bristol-Myers Squibb, Pfizer Inc.

Eliquis®

Apixaban

Cardiovascular Diseases

7,395

9

Roche

Avastin®

Bevacizumab

Oncology

7,089

10

Bayer, Johnson & Johnson

XareltoTM

Rivaroxaban

Cardiovascular Diseases

6,590

11

Bristol Myers Squibb, Ono Pharmaceutical

Opdivo

Nivolumab

Oncology

5,815

12

Sanofi

Lantus

Insulin Glargine

Diabetes

5,731

13

Pfizer Inc.

Prevnar 13/Prevenar 13

Pneumococcal 7-Valent Conjugate

Anti-bacterial

5,601

14

Pfizer Inc., Eisai

Lyrica

Pregabalin

Neurological/Mental Disorders

5,318

15

Amgen, Kyowa Hakko Kirin

Neulasta®

Pegfilgrastim

Blood Disorders

4,553

Sign up, stay ahead

In order to stay informed, and receive

industry updates along with our data compilations, do sign up for the PharmaCompass Newsletter and

you will receive updated information as it becomes available along with a lot

more industry analysis.

Click here to Access All

the 2017 Data (Excel version available) for FREE!

Impressions: 58407

https://www.pharmacompass.com/radio-compass-blog/top-drugs-by-sales-in-2017-who-sold-the-blockbuster-drugs

#PharmaFlow by PHARMACOMPASS

29 Mar 2018

Global

pharmaceutical companies are increasingly focusing on the development of new

biologics. In fact, in 2016, nine out of the top

15 pharmaceutical drugs by sales were of biologic origin. This makes us wonder

what the future holds for manufacturers specializing in drugs that originate

from chemical synthesis.

This

week, PharmaCompass continued its analysis of the top pharma drugs by

sales to evaluate the drugs that registered large sales growth in 2016.

Click here to Access All the 2016 Data (Excel version available) for FREE!

Please

note that these are not the top-selling drugs, but are the top 10 drugs that

registered the maximum growth in global sales over 2015.

Interestingly, things didn’t appear that bad for drugs originating from chemical synthesis — while the top two drugs on the list were biologics, the remaining originated from chemical synthesis.

Here’s a list of drugs that witnessed the largest sales growth in 2016:

1. Opdivo (nivolumab) – Bristol-Myers Squibb

2016

sales: US$ 3,774 million

2015 sales:

US$ 942 million

Sales

growth: US$ 2,832 million

First

approved in 2014, Bristol-Myers Squibb’s Opdivo and Merck’s Keytruda — also known as checkpoint inhibitors — continued to stay on track to be among the top 20 best-selling drugs in the world by 2020. They represent the hot new field of immunotherapy and are known to have given 90-year old Jimmy Carter (former President of the United States) hope in his fight against cancer.

With

a sales growth of US$ 2.832 billion, Opdivo registered the highest sales growth

of any single drug in 2016. However, Bristol-Myers Squibb received a nasty

surprise last year when Opdivo did not demonstrate the desired slowdown in the

progress of advanced lung cancer in a trial, as compared to conventional

chemotherapy.

While Bristol-Myers’ stock price plunged on this news, Merck announced that not only did Keytruda succeed in a clinical trial as an initial treatment for advanced non-small cell lung cancer, but patients actually lived longer. Although Keytruda did not make it to our list of top 10 drugs by sales growth in 2016, it did register a sales increase of US$ 836 million, as its sales grew from US$ 566 million to US$ 1,402 million.

Click here to Access All the 2016 Data (Excel version available) for FREE!

2. Humira (adalimumab) – AbbVie

2016

sales: US$ 16,078 million

2015

sales: US$ 14,012 million

Sales

growth: US$ 2,066 million

Abbvie’s Humira (adalimumab)

juggernaut continued as it not only remained the best-selling drug in the

world, but also added another US$ 2 billion to its 2015 sales by generating

record sales of US $16.078 billion in 2016.

Last

year, the US Food and Drug Administration (FDA) approved Amgen’s Amjevita™ (adalimumab – atto) — a biosimilar of Humira®. Therefore, it remains to be seen if Humira will be able to sustain the momentum. Amjevita was approved for treating adults with a variety of medical conditions ranging from rheumatoid arthritis, plaque psoriasis, to ulcerative colitis.

3. Epclusa (sofosbuvir and velpatasvir) – Gilead

2016

sales: US$ 1,752 million (new launch)

Gilead’s third sofosbuvir-based regimen — Epclusa (sofosbuvir and velpatasvir) was approved by the US FDA in June 2016. It is the first and only all-oral, pan-genotypic single tablet regimen for chronic Hepatitis C virus infection. While Epclusa registered an impressive start, Gilead's other two sofosbuvir-based treatments — Sovaldi (sofosbuvir) and Harvoni (sofosbuvir and lepidasvir) — saw their combined sales decline by almost US$ 6 billion.

Click here to Access All the 2016 Data (Excel version available) for FREE!

4. Imbruvica (ibrutinib) — Johnson & Johnson / AbbVie

2016

sales: US$ 3,083 million

2015

sales: US$ 1,443 million

Sales

growth: US$ 1,640 million

Abbvie’s 2015 US$ 21 billion buy of Pharmacyclics seems to be paying off.

The Pharmacyclics buy was a way to get access to Imbruvica (ibrutinib), a cancer drug which

is co-marketed with Johnson & Johnson. It generated sales of US$ 3.083 billion in 2016. Imbruvica works by blocking a specific protein called Bruton’s tyrosine kinase (BTK). In December 2011, Johnson & Johnson said it would pay Pharmacyclics as much as US$ 975 million to fund getting the drug to market in exchange for half the profits generated globally.

5. Eliquis (apixaban) -

Bristol-Myers Squibb / Pfizer

2016

sales: US$ 3,342 million

2015

sales: US$ 1,860 million

Sales

growth: US$ 1,483 million

Although

apixaban was the third-to-market

novel oral anticoagulant (NOAC), which is co-promoted by Pfizer and Bristol-Myers Squibb as Eliquis, it continues to unseat Johnson & Johnson’s Xarelto (rivaroxaban) as the leader in its

class based on total prescriptions. Rivaroxaban's total 2016 sales were US$

5.392 billion.

While Pfizer’s reports its sales as part of Alliance revenues, and exact sales are not known, Bristol-Myers Squibb results alone put Eliquis in the top 10 list. Generics are hot on their tail as, last month, Pfizer and Bristol-Myers’ filed suits against 16 generic makers to uphold their patents for apixaban.

6. Genvoya (elvitegravir,

cobicistat, emtricitabine, tenofovir alafenamide) — Gilead

2016

sales: US$ 1,484 million

2015

sales: US$ 45 million

Sales

growth: US$ 1,439 million

Genvoya has been the most

successful HIV treatment launch since the introduction of Atripla (the first

single-tablet regimen launched a decade ago). Gilead is the dominant HIV

player in the US market and has the top three most-prescribed HIV regimens in

the US.

Genvoya

adds Tenofovir Alafenamide (TAF) to already known

treatments. TAF based drugs have demonstrated a better safety profile. They

would also allow Gilead to maintain its dominance in the HIV market.

Click here to Access All the 2016 Data (Excel version available) for FREE!

7. Ibrance (palbociclib) — Pfizer

2016

sales: US$ 2,135 million

2015

sales: US$ 723 million

Sales

growth: US$ 1,412 million

Discovered

in Pfizer laboratories and approved by the US

FDA in February 2015, Ibrance is used in combination

with Letrozole as a first-line

treatment of postmenopausal women with estrogen receptor-positive, human

epidermal growth factor receptor 2-negative (ER+/HER2-) metastatic breast

cancer.

8. Triumeq (abacavir,

dolutegravir, lamivudine) – GlaxoSmithKline

2016

sales:US$ 2,151 million

2015

sales: US$ 905 million

Sales

growth: US$ 1,246 million

GlaxoSmithKline's HIV drugs business — ViiV Healthcare — has been enjoying sales growth with the introduction of Triumeq ® in its portfolio. While GSK is the major shareholder in ViiV Healthcare, Pfizer and Shionogi also have a stake. Triumeq® is the company’s first fixed-dose combination tablet for a once-daily single pill regimen that combines dolutegravir, an integrase inhibitor, with the nucleoside reverse transcriptase inhibitors — abacavir and lamivudine.

9. Revlimid (lenalidomide) – Celgene

2016

sales: US$ 6,974 million

2015

sales: US$ 5,801 million

Sales

growth: US$ 1,173 million

Celgene’s Revlimid (lenalidomide) — a thalidomide-derivative introduced in 2004 as an immunomodulatory agent for the treatment of various cancers such as multiple myeloma — brought in US$ 5.8 billion in 2015, and grew another 20 percent this year, to US $6.974 billion. Revlimid now contributes more than 60 percent to Celgene's total sales of US$ 11.229 billion.

10. Xarelto (rivaroxaban) – Johnson & Johnson (US) and Bayer

2016

sales: US$ 5,392 million

2015

sales: US$ 4,255 million

Sales

growth: US$ 1,137 million

Bayer’s Xarelto, which is promoted by Johnson & Johnson in the United States, provided patients with an alternative to the old-guard therapy — warfarin. While rivaroxaban is competing with other

novel oral anticoagulants (NOAC) like Eliquis (apixaban) and Pradaxa (dabigatran), rivaroxaban has the

class lead in indications.

Xarelto

recently posted positive results in a large-scale Phase 3 study —COMPASS, involving 27,402 patients, that assessed the effect of the

blood thinner in preventing major adverse cardiac events (MACE).

The

trial was stopped a year early

on the advice of an independent Data Monitoring Committee, after the primary

endpoint of prevention of MACE (which includes cardiovascular death, myocardial

infarction and stroke) reached its pre-specified criteria for superiority over aspirin.

Click here to Access All the 2016 Data (Excel version available) for FREE!

Our

view

In QuintilesIMS Institute’s new annual drug spending report, analysts have forecasted that

over the coming five years the industry should continue to receive 40 to 45 new

drug approvals every year.

A quarter of all the drugs in late-stage development are now

focused on oncology. The rate of oncology drug development has hit such a

rapid pace that new drugs are superseding old ones in a matter of a few years.

It’s clear that this compilation will see radical changes next year. However, with eight out of the 10 fastest-selling drugs coming from chemical synthesis, traditional generic manufacturers still have a lot of opportunities to explore.

Sign up,

stay ahead

In order to stay informed,

and receive industry updates along with our data compilations, do sign up for

the PharmaCompass Newsletter and you will receive updated information as

it becomes available along with a lot more industry analysis.

Click here to Access All the 2016 Data (Excel version available) for FREE!

Impressions: 9289

https://www.pharmacompass.com/radio-compass-blog/chemical-entities-shine-in-the-top-10-fastest-growing-drugs-of-2016

#PharmaFlow by PHARMACOMPASS

17 May 2017

The year 2016 finished with a whimper insofar as mergers and acquisitions (M&As) were concerned. The preceding year — 2015 — had gone down in history as a record year for M&As in the pharmaceutical and biotech space, when deals worth US $300 billion were announced.

While drug companies were not as active on

the M&A front, the product sales growth in 2016 continued to stay extremely

robust and the order of the top ranked drugs changed little from the previous

year.

This week, PharmaCompass brings you

a compilation of the top drugs of 2016 by sales revenue.

Click here to Access All the

2016 Data (Excel version available) for FREE!

The top-sellers

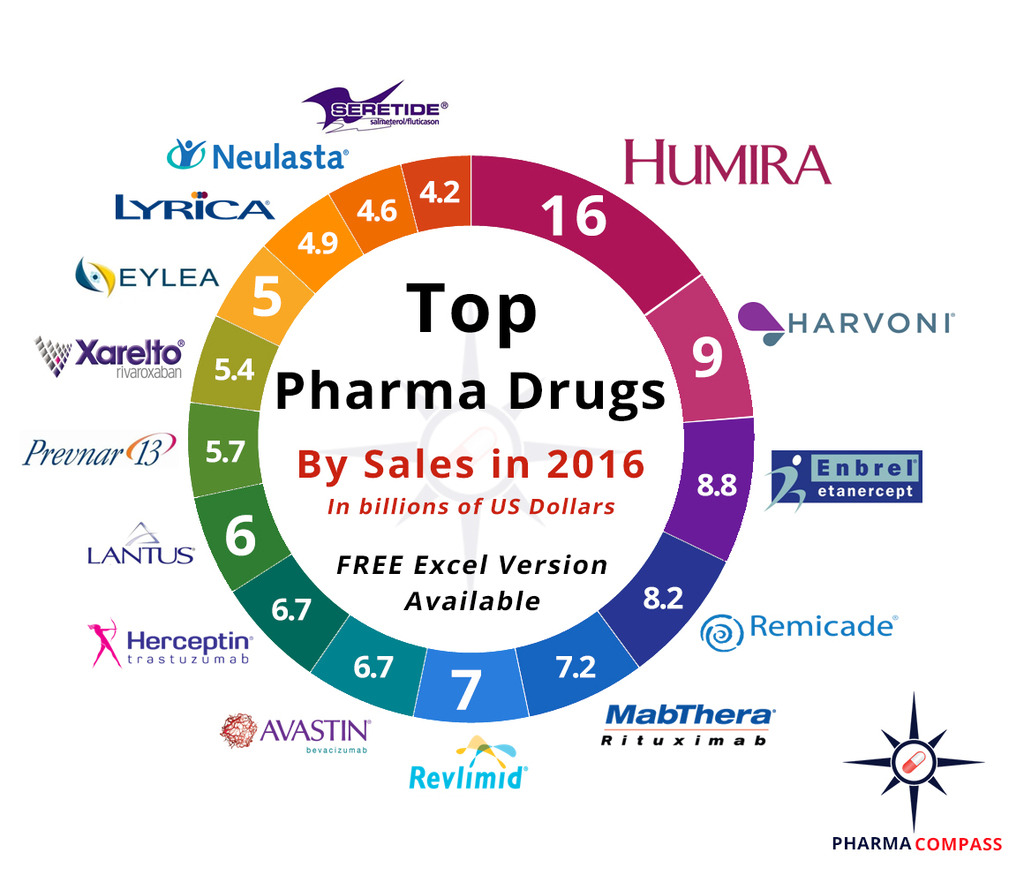

Abbvie’s Humira (adalimumab) continued to remain the best-selling drug in the

world and added another US $2 billion to its 2015 sales by generating record

sales of US $16.078 billion in 2016.

Last year also saw the US Food and Drug Administration (FDA) approve Amgen’s Amjevita™ (adalimumab – atto) — a biosimilar of Humira®. Amjevita was approved for treating adults with a variety of medical conditions ranging from rheumatoid arthritis, plaque psoriasis, to ulcerative colitis.

Click here to Access All the

2016 Data (Excel version available) for FREE!

Gilead’s Harvoni (ledipasvir and sofosbuvir), with record sales of US $13.864 billion in 2015, had a slightly muted performance in 2016 as sales fell to US $9.081 billion (a drop of US $4.783 billion). Gilead failed to maintain its initial rate of new prescriptions, and competition from Merck and AbbVie forced it to offer major discounts to health insurers.

While Gilead executives still believe there is lots of growth left in the hepatitis C market, this year Gilead will continue to face headwinds as Merck's new combination pill — Zepatier — entered the market with a list price at US $54,600 for a 12-week regimen, well below the US $94,500 for Harvoni.

Biological drugs, Enbrel (etanercept),

Remicade (infliximab) and MabThera (rituximab), held onto their positions of 2015, although their combined sales increased a little over US $300

million.

This means that for yet another year, the

four best-selling drugs in the world are from biological origin.

Celgene’s Revlimid (lenalidomide) — a thalidomide derivative introduced in 2004 as an immunomodulatory agent for the treatment of various cancers such as multiple myeloma — brought in US $5.8 billion in 2015, and grew another 20 percent this year, to US $6.974 billion. Revlimid now contributes more than 60 percent to the company's total sales of US $11.229 billion.

With almost identical sales of US $6.7

billion, Roche’s cancer treatments Herceptin and Avastin were also into

the top 10 best selling drugs in 2016, making Roche have the most number of

products, three of which made it to the list.

Click here to Access All the

2016 Data (Excel version available) for FREE!

Facing onslaught of generics, biosimilars

Against the backdrop of questions being raised about

insulin pricing and possible collusion in the United States, Sanofi saw its insulin treatment Lantus (insulin glargine) drop from number six on the 2015 list to number 9 in 2016 as sales fell by US $717 million to a little over US $6 billion. Sanofi’s competitors in the diabetes space — Novo Nordisk and Eli Lilly — also registered a drop in their insulin sales.

In addition to the pricing pressure, Sanofi will continue to contend with Lilly and Boehringer Ingelheim’s FDA approved biosimilar of insulin glargine — Basaglar — which was approved in December 2015.

Click here to Access All the

2016 Data (Excel version available) for FREE!

Basaglar is biologically similar to Sanofi’s Lantus and was announced at a price 15 percent lower than that of Lantus.

GSK’s Advair, which is preparing for generic competition in 2017, saw its sales drop 5 percent in British Pounds to £3,485. However, the dollar value was significantly lower in view of the fall in the Pound’s value after Brexit.

AstraZeneca’s Crestor (rosuvastatin calcium), Otsuka’s Abilify (aripiprazole) and Novartis’ Gleevec (imatinib) all saw their sales crash in 2016 as a result of generic onslaught. The three drugs together witnessed a combined sales drop of US $5.7 billion.

Top 20 drugs by sales

Here is PharmaCompass’ compilation

of the best-selling drugs of 2016. This is based on information extracted from

annual reports and US Securities and Exchange Commission (SEC) filings of major

pharmaceutical companies.

If you would like your own copy of all the information we’ve collected, email us at support@pharmacompass.com and we’ll send you an Excel version.

Click

here to access all the 2016 data (Excel version available) for FREE!

S. No

Product

Active Ingredient

Main Therapeutic Indication

Company

2016 Revenue in Millions (USD)

2015 Revenue in Millions (USD)

Sales Difference in Millions (USD)

1

Humira

Adalimumab

Immunology (Organ Transplant, Arthritis etc.)

Abbvie

16,078

14,012

2,066

2

Harvoni

Ledipasvir and Sofosbuvir

Infectious Diseases (HIV, Hepatitis etc.)

Gilead

9,081

13,864

(4,783)

3

Enbrel

Etanercept

Immunology (Organ Transplant, Arthritis etc.)

Amgen/Pfizer Inc.

8875

8697

178

4

Remicade

Infliximab

Immunology (Organ Transplant, Arthritis etc.)

Johnson & Johnson/Merck & Co

8,234

8,355

(121)

5

MabThera/Rituxan

Rituximab

Oncology

Roche

7227

6974.55

252

6

Revlimid

Lenalidomide

Oncology

Celgene

6,974

5,801

1,173

7

Avastin

Bevacizumab

Oncology

Roche

6,715

6,617

98

8

Herceptin

Trastuzumab

Oncology

Roche

6,714

6,473

242

9

Lantus

Insulin Glargine

Diabetes

Sanofi

6,057

6,773

(717)

10

Prevnar/Prevenar

13

Pneumococcal 13-Valent Conjugate

Anti-bacterial

Pfizer Inc.

5,718

6,246

(528)

11

Xarelto

Rivaroxaban

Cardiovascular Diseases

Bayer/Johnson & Johnson

5,392

4,255

1,137

12

Eylea

Aflibercept

Ophthalmology

Regeneron Pharmaceuticals, Inc./Bayer

5,046

3,978

1,068

13

Lyrica

Pregabalin

Neurological/Mental Disorders

Pfizer Inc.

4,966

4,839

127

14

Neulasta

Pegfilgrastim

Blood Disorders

Amgen

4,648

4,715

(67)

15

Seretide/Advair

Salmeterol

Respiratory Disorders

GlaxoSmithKline

4,252

4,491

(239)

16

Copaxone

Glatiramer

Neurological/Mental Disorders

Teva

4,223

4,023

200

17

Sovaldi

Sofosbuvir

Infectious Diseases (HIV, Hepatitis etc.)

Gilead

4,001

5,276

(1,275)

18

Tecfidera

Dimethyl Fumarate

Neurological/Mental Disorders

Biogen

3,968

3,638

330

19

Januvia

Sitagliptin

Diabetes

Merck & Co

3,908

3,864

44

20

Opdivo

Nivolumab

Oncology

Bristol-Myers Squibb

3,774

942

2,832

Blockbusters in the making

With almost US $5 billion in sales, a 14 percent growth over the previous year, Pfizer’s Lyrica enjoyed its last year before generic competition enters the market as Generics (UK) Limited (Mylan) and Actavis Group PTC ehf won a patent challenge in the United Kingdom.

Lyrica generics are expected in the United

States in late 2018.

Click here to Access All the

2016 Data (Excel version available) for FREE!

As Abbvie’s Humira begins to face competition from Amgen, Abbvie’s US $21 billion buy of Pharmacyclics seems to be paying off. The Pharmacyclics buy was a way to get access to Imbruvica (ibrutinib), which generated total 2016 sales of US $3.083 billion — an increase of US $1.64 billion over the previous year.

Anticoagulants, Xarelto (rivaroxaban), Eliquis (apixaban), Pradaxa (dabigatran) all registered significant positive growth with a combined increase of almost US $ 2.75 billion.

Gilead and GSK’s combination HIV treatments — Genvoya and Triumeq — also reported sales increase of over a billion dollars each.

Sign up,

stay ahead

In order to stay informed, and receive

industry updates along with our data compilations, do sign up for the PharmaCompass

Newsletter and you will receive updated information as it becomes available

along with a lot more industry analysis.

Click here to Access All the

2016 Data (Excel version available) for FREE!

Impressions: 58546

https://www.pharmacompass.com/radio-compass-blog/top-drugs-by-sales-in-2016-who-sold-the-blockbuster-drugs

#PharmaFlow by PHARMACOMPASS

19 Apr 2017

This week’s Phispers has regulatory and M&A news from across the world as Pfizer ends its support to drugs used in lethal injections, Endo’s problems get compounded and Thalidomide’s Nazi war criminal links are uncovered. European regulators to ‘rely more’ on FDA inspectionsSince the US Department of Justice imposed a US $ 500

million fine on Indian drug manufacturer Ranbaxy in 2013, we have seen regulatory concerns over globalization of drug manufacturing. The Ranbaxy controversy also demonstrated differences in the approaches of regulators in the EU and the US. While the US FDA banned the import of products from two of Ranbaxy’s factories into the US, no such move was taken by the European regulator, the European Medicines Agency (EMA). “A legal framework will allow us to be able to rely

more on US inspections,” Emer Cooke, head of international affairs at the EMA, said in a news report. “That will allow us to release resources to adopt a more risk-based approach.” This statement manifests that European regulators rely more

on FDA inspections, than on their own. Cooke was referring to the need for

Transatlantic Trade and Investment Partnership, a partnership between the EU

and the US to better channel scarce resources between the two regions. Data-integrity issues uncovered at Capsugel’s U.S. plant Problems of data-integrity don’t seem limited only to Asia as Sweden’s regulator, Medical Products Agency (MPA), uncovered “two critical and one major concerns” related to data-integrity at Capsugel’s Bend Research Inc. facility in Oregon. The inspectors also found that several findings, from two previous MPA inspections, had not been corrected and concluded that the facility had an “unacceptable level of GMP compliance”.Bend

Research makes oral solid dose products, primarily for clinical trials and was acquired

by Capsugel

in 2013. Capsugel subsequently invested $20m in to add commercial

spray drying capacity at the Oregon site. Mylan and Pfizer put skin in the game by

investing billionsThis week, both Mylan NV and Pfizer made

acquisitions in the dermatology/topicals space.

Mylan NV announced its decision to

buy skin drug assets from Renaissance Acquisition Holdings LLC for around

US $ 1 billion to complement its existing products. Pfizer, on the other hand, will buy Anacor Pharmaceuticals – a biopharmaceutical company – for US $ 4.5 billion. This is said to be Pfizer’s Plan B, post the collapse of the Allergan mega deal. Pfizer CEO Ian Read had earlier said Pfizer will shop for deals to beef up the “innovative” side of its business. Anacor is “a strong fit” with Pfizer’s inflammation and immunology group, said Albert Bourla, group president of the Pfizer division that includes innovative pharma. The acquisition is “expected to enhance near-term revenue growth for the innovative business.” For instance, Anacor’s eczema therapy, crisaborole, should bring in US $ 2 billion in annual sales. “The dermatology/topicals space has long been an area of focus for Mylan and one that we have targeted for expansion,” Heather Bresch, Mylan’s chief executive officer, said. Pfizer ends support to drugs used in lethal

injectionsLast week, Pfizer took a milestone

step and announced it had imposed sweeping controls on the distribution of

its products to ensure that none are used in lethal injections. This is a step that closes the last remaining open-market

source of drugs used in executions. Such restrictions have already been adopted

by over 20 American and European drug companies. They have cited moral or

business reasons to take such steps. “With Pfizer’s announcement, all FDA-approved manufacturers of any potential execution drug have now blocked their sale for this purpose,” said Maya Foa, who tracks drug companies for Reprieve, a London-based human rights advocacy group. Thalidomide’s inventor knew about its risks before marketing it, says filmVancouver

documentary director John Zaritsky who has made his third film this year on Thalidomide – the

devastating drug that caused thousands of birth defects before being pulled out of the market in the early 1960s – has revealed an interesting finding in his latest film ‘No Limits’. The world premiere of the film took place on May 7, as part of Vancouver’s DOXA festival. According to the film, developers of the drug were war criminals in Nazi Germany. It also shows how today’s developing world is still marketing thalidomide as treatment for leprosy — leading to the birth of deformed babies. The drug maker – Grunenthal – continues to operate. According to the film, Grunenthal researcher and Thalidomide’s inventor, Heinrich Mueckter, had been a doctor at the Buchenwald concentration camp, performing experiments on prisoners. Mueckter

became a multi-millionaire through Thalidomide sales. The documents revealed

that Grunenthal knew months before putting Thalidomide on the market that their

drug would produce malformed babies. They still went ahead and made fortunes

off the drug. China’s Fosun group makes billion dollar bid for India’s Gland PharmaThis

week, Shanghai

Fosun Pharmaceutical (Group) announced it has made a

non-binding bid for India’s Gland

Pharma Ltd,

the Hyderabad-based injectable drugs manufacturer. According

to a Reuters news report, Gland Pharma founders and KKR, which jointly own

about 96 percent of the company, are selling their combined stake, which is

valued at US $ 1 billion and US $ 1.5 billion respectively. Global

buyout firm Advent International and US-based Baxter

International are also said to be among the companies interested in buying out

Gland Pharma. Shanghai Fosun said the proposal was made through its unit Fosun

Industrial Co Ltd. More trouble for Endo as Mylan, Novartis eye Teva’s generic portfolioAfter the disappointing guidance which caused Endo’s stock price to crash last week, the Federal Trade Commission (FTC) attacked Endo for delaying the launch of an authorized generic. The FTC filed a complaint

in a district court in Pennsylvania against Endo, Impax, Watson

Laboratories and others, alleging the companies violated the FTC Act by entering into no-AG commitments, among other things on two of its “most important branded prescription drug products,’’ Opana ER, an opioid drug, and Lidoderm, a lidocaine patch.Meanwhile Endo’s arch rival Teva’s drug portfolio in the UK, Ireland and Iceland is attracting bidders such as Mylan NV

and Novartis AG. According

to reports, private equity firms such as Apollo Global Management and Cinven

are weighing bids for Teva, which could fetch US $ 1.5 to US $ 2 billion. Teva is selling assets as it works to get regulatory approval for its US $ 40.5 billion acquisition of Allergan Plc’s generics business. Envoy warns Colombia government about its

efforts to override Novartis patentLast month, a Colombian embassy official sent a memo to the foreign

minister of his country warning the government about its efforts to override a

patent on a cancer drug made by Novartis. According to the official, such efforts

could harm US support for peace initiative in Colombia. According to

reports, the Colombian health ministry has been planning to issue a compulsory

license for Gleevec (also marketed as Glivec) – a leukemia treatment – which would allow generic drug makers to manufacture a cheaper version of the drug. Novartis has strongly opposed the move. The leaked memo was posted by Knowledge Ecology International and

states that the US Trade Representative and staffers from the Senate Finance

Committee requested to meet embassy officials to discuss US concerns with

Colombia's plans. Gilead gets Sovaldi patent in India amid protests

by patient groupsIn a politically sensitive move, the Indian Patent Office (IPO) reversed

course and granted a patent to Gilead

Sciences for its Sovaldi

hepatitis C treatment. This way, the IPO earned the wrath of many patient groups, while

handing Gilead an unexpected victory. The decision came in response to a

challenge to the Gilead patent filed by several patient advocacy groups and

companies that make pharmaceutical ingredients. Last year, the IPO had rejected

the company’s patent application on grounds that it was not a significant

improvement over an earlier compound developed by Gilead.

Impressions: 3021

https://www.pharmacompass.com/radio-compass-blog/capsugel-s-u-s-plant-has-data-integrity-issues-billion-dollar-chinese-bid-for-indian-sterile-manufacturer-pfizer-mylan-s-dermatology-bet

#PharmaFlow by PHARMACOMPASS

19 May 2016