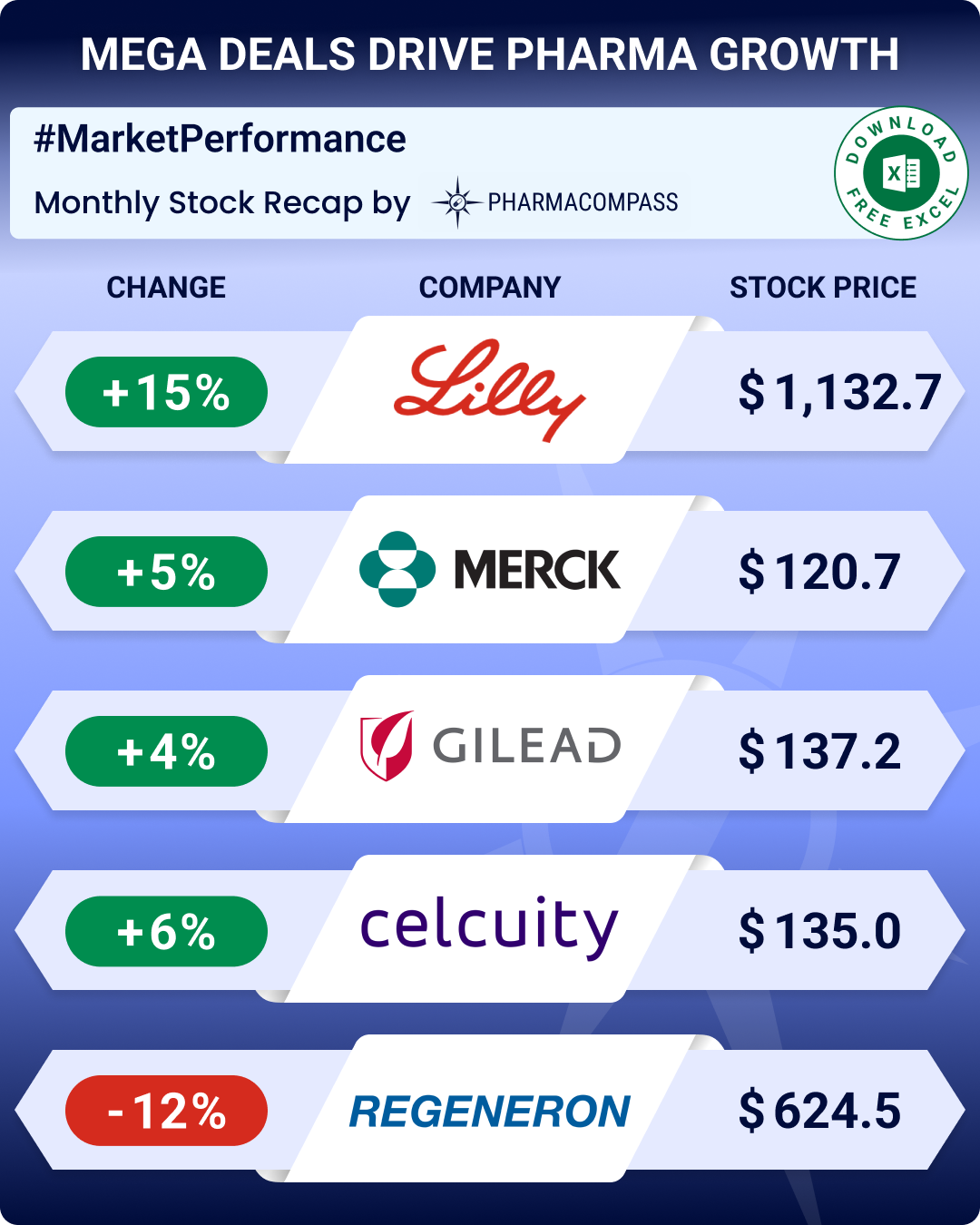

BLOG

MARKET INTEL by PharmaCompass

CONTENT by Suppliers

- Interview #SpeakPharma

- Video #SupplierSpotlight

- Vlog #PharmaReel

- Company Bio #AboutSupplier

- Services Bio #AboutCapabilities

News

Create content with us, ask us

Global pharmaceutical companies are increasingly focusing on the development of new biologics. In fact, in 2016, nine out of the top 15 pharmaceutical drugs by sales were of biologic origin. This makes us wonder what the future holds for manufacturers specializing in drugs that originate from chemical synthesis.

This week, PharmaCompass continued its analysis of the top pharma drugs by sales to evaluate the drugs that registered large sales growth in 2016.

Click here to Access All the 2016 Data (Excel version available) for FREE!

Please note that these are not the top-selling drugs, but are the top 10 drugs that registered the maximum growth in global sales over 2015.

Interestingly, things didn’t appear that bad for drugs originating from chemical synthesis — while the top two drugs on the list were biologics, the remaining originated from chemical synthesis.

Here’s a list of drugs that witnessed the largest sales growth in 2016:

1. Opdivo (nivolumab) – Bristol-Myers Squibb

2016 sales: US$ 3,774 million

2015 sales: US$ 942 million

Sales growth: US$ 2,832 million

First approved in 2014, Bristol-Myers Squibb’s Opdivo and Merck’s Keytruda — also known as checkpoint inhibitors — continued to stay on track to be among the top 20 best-selling drugs in the world by 2020. They represent the hot new field of immunotherapy and are known to have given 90-year old Jimmy Carter (former President of the United States) hope in his fight against cancer.

With a sales growth of US$ 2.832 billion, Opdivo registered the highest sales growth of any single drug in 2016. However, Bristol-Myers Squibb received a nasty surprise last year when Opdivo did not demonstrate the desired slowdown in the progress of advanced lung cancer in a trial, as compared to conventional chemotherapy.

While Bristol-Myers’ stock price plunged on this news, Merck announced that not only did Keytruda succeed in a clinical trial as an initial treatment for advanced non-small cell lung cancer, but patients actually lived longer. Although Keytruda did not make it to our list of top 10 drugs by sales growth in 2016, it did register a sales increase of US$ 836 million, as its sales grew from US$ 566 million to US$ 1,402 million.

Click here to Access All the 2016 Data (Excel version available) for FREE!

2. Humira (adalimumab) – AbbVie

2016 sales: US$ 16,078 million

2015 sales: US$ 14,012 million

Sales growth: US$ 2,066 million

Abbvie’s Humira (adalimumab) juggernaut continued as it not only remained the best-selling drug in the world, but also added another US$ 2 billion to its 2015 sales by generating record sales of US $16.078 billion in 2016.

Last year, the US Food and Drug Administration (FDA) approved Amgen’s Amjevita™ (adalimumab – atto) — a biosimilar of Humira®. Therefore, it remains to be seen if Humira will be able to sustain the momentum. Amjevita was approved for treating adults with a variety of medical conditions ranging from rheumatoid arthritis, plaque psoriasis, to ulcerative colitis.

3. Epclusa (sofosbuvir and velpatasvir) – Gilead

2016 sales: US$ 1,752 million (new launch)

Gilead’s third sofosbuvir-based regimen — Epclusa (sofosbuvir and velpatasvir) was approved by the US FDA in June 2016. It is the first and only all-oral, pan-genotypic single tablet regimen for chronic Hepatitis C virus infection. While Epclusa registered an impressive start, Gilead's other two sofosbuvir-based treatments — Sovaldi (sofosbuvir) and Harvoni (sofosbuvir and lepidasvir) — saw their combined sales decline by almost US$ 6 billion.

Click here to Access All the 2016 Data (Excel version available) for FREE!

4. Imbruvica (ibrutinib) — Johnson & Johnson / AbbVie

2016 sales: US$ 3,083 million

2015 sales: US$ 1,443 million

Sales growth: US$ 1,640 million

Abbvie’s 2015 US$ 21 billion buy of Pharmacyclics seems to be paying off. The Pharmacyclics buy was a way to get access to Imbruvica (ibrutinib), a cancer drug which is co-marketed with Johnson & Johnson. It generated sales of US$ 3.083 billion in 2016. Imbruvica works by blocking a specific protein called Bruton’s tyrosine kinase (BTK). In December 2011, Johnson & Johnson said it would pay Pharmacyclics as much as US$ 975 million to fund getting the drug to market in exchange for half the profits generated globally.

5. Eliquis (apixaban) -

Bristol-Myers Squibb / Pfizer

2016 sales: US$ 3,342 million

2015 sales: US$ 1,860 million

Sales growth: US$ 1,483 million

Although apixaban was the third-to-market novel oral anticoagulant (NOAC), which is co-promoted by Pfizer and Bristol-Myers Squibb as Eliquis, it continues to unseat Johnson & Johnson’s Xarelto (rivaroxaban) as the leader in its class based on total prescriptions. Rivaroxaban's total 2016 sales were US$ 5.392 billion.

While Pfizer’s reports its sales as part of Alliance revenues, and exact sales are not known, Bristol-Myers Squibb results alone put Eliquis in the top 10 list. Generics are hot on their tail as, last month, Pfizer and Bristol-Myers’ filed suits against 16 generic makers to uphold their patents for apixaban.

6. Genvoya (elvitegravir,

cobicistat, emtricitabine, tenofovir alafenamide) — Gilead

2016 sales: US$ 1,484 million

2015 sales: US$ 45 million

Sales growth: US$ 1,439 million

Genvoya has been the most successful HIV treatment launch since the introduction of Atripla (the first single-tablet regimen launched a decade ago). Gilead is the dominant HIV player in the US market and has the top three most-prescribed HIV regimens in the US.

Genvoya adds Tenofovir Alafenamide (TAF) to already known treatments. TAF based drugs have demonstrated a better safety profile. They would also allow Gilead to maintain its dominance in the HIV market.

Click here to Access All the 2016 Data (Excel version available) for FREE!

7. Ibrance (palbociclib) — Pfizer

2016 sales: US$ 2,135 million

2015 sales: US$ 723 million

Sales growth: US$ 1,412 million

Discovered in Pfizer laboratories and approved by the US FDA in February 2015, Ibrance is used in combination with Letrozole as a first-line treatment of postmenopausal women with estrogen receptor-positive, human epidermal growth factor receptor 2-negative (ER+/HER2-) metastatic breast cancer.

8. Triumeq (abacavir,

dolutegravir, lamivudine) – GlaxoSmithKline

2016 sales:US$ 2,151 million

2015 sales: US$ 905 million

Sales growth: US$ 1,246 million

GlaxoSmithKline's HIV drugs business — ViiV Healthcare — has been enjoying sales growth with the introduction of Triumeq ® in its portfolio. While GSK is the major shareholder in ViiV Healthcare, Pfizer and Shionogi also have a stake. Triumeq® is the company’s first fixed-dose combination tablet for a once-daily single pill regimen that combines dolutegravir, an integrase inhibitor, with the nucleoside reverse transcriptase inhibitors — abacavir and lamivudine.

9. Revlimid (lenalidomide) – Celgene

2016 sales: US$ 6,974 million

2015 sales: US$ 5,801 million

Sales growth: US$ 1,173 million

Celgene’s Revlimid (lenalidomide) — a thalidomide-derivative introduced in 2004 as an immunomodulatory agent for the treatment of various cancers such as multiple myeloma — brought in US$ 5.8 billion in 2015, and grew another 20 percent this year, to US $6.974 billion. Revlimid now contributes more than 60 percent to Celgene's total sales of US$ 11.229 billion.

10. Xarelto (rivaroxaban) – Johnson & Johnson (US) and Bayer

2016 sales: US$ 5,392 million

2015 sales: US$ 4,255 million

Sales growth: US$ 1,137 million

Bayer’s Xarelto, which is promoted by Johnson & Johnson in the United States, provided patients with an alternative to the old-guard therapy — warfarin. While rivaroxaban is competing with other novel oral anticoagulants (NOAC) like Eliquis (apixaban) and Pradaxa (dabigatran), rivaroxaban has the class lead in indications.

Xarelto

recently posted positive results in a large-scale Phase 3 study —COMPASS, involving 27,402 patients, that assessed the effect of the

blood thinner in preventing major adverse cardiac events (MACE).

The

trial was stopped a year early

on the advice of an independent Data Monitoring Committee, after the primary

endpoint of prevention of MACE (which includes cardiovascular death, myocardial

infarction and stroke) reached its pre-specified criteria for superiority over aspirin.

Click here to Access All the 2016 Data (Excel version available) for FREE!

Our

view

In QuintilesIMS Institute’s new annual drug spending report, analysts have forecasted that over the coming five years the industry should continue to receive 40 to 45 new drug approvals every year.

A quarter of all the drugs in late-stage development are now focused on oncology. The rate of oncology drug development has hit such a rapid pace that new drugs are superseding old ones in a matter of a few years.

It’s clear that this compilation will see radical changes next year. However, with eight out of the 10 fastest-selling drugs coming from chemical synthesis, traditional generic manufacturers still have a lot of opportunities to explore.

Sign up,

stay ahead

In order to stay informed, and receive industry updates along with our data compilations, do sign up for the PharmaCompass Newsletter and you will receive updated information as it becomes available along with a lot more industry analysis.

Click here to Access All the 2016 Data (Excel version available) for FREE!

The PharmaCompass Newsletter – Sign Up, Stay Ahead

Feedback, help us to improve. Click here

Image Credit : Top 10 fastest-growing drugs of 2016 by PharmaCompass is licensed under CC BY 2.0

“ The article is based on the information available in public and which the author believes to be true. The author is not disseminating any information, which the author believes or knows, is confidential or in conflict with the privacy of any person. The views expressed or information supplied through this article is mere opinion and observation of the author. The author does not intend to defame, insult or, cause loss or damage to anyone, in any manner, through this article.”