X

API Suppliers

US DMFs Filed

CEP/COS Certifications

JDMFs Filed

Other Certificates

Other Suppliers

USA (Orange Book)

Europe

Canada

Australia

South Africa

Uploaded Dossiers

U.S. Medicaid

Annual Reports

Impressions: 2622

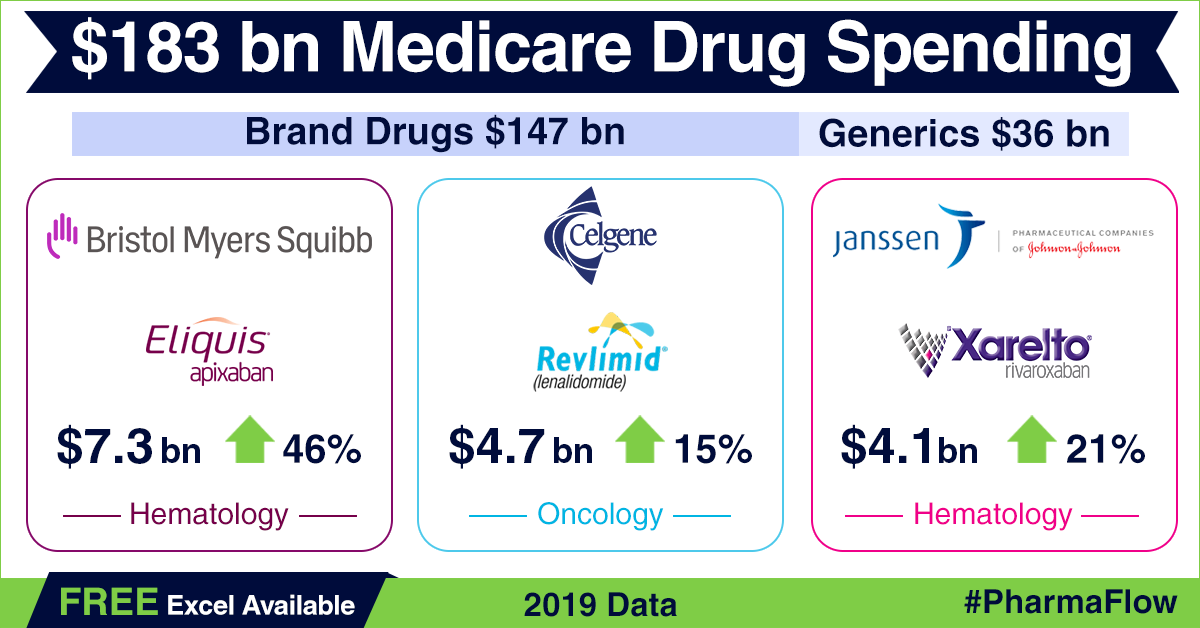

https://www.pharmacompass.com/radio-compass-blog/america-s-drug-price-hike-conundrum-in-backdrop-of-2019-medicare-part-d-data

Impressions: 54752

https://www.pharmacompass.com/radio-compass-blog/top-drugs-and-pharmaceutical-companies-of-2019-by-revenues

Impressions: 58407

https://www.pharmacompass.com/radio-compass-blog/top-drugs-by-sales-in-2017-who-sold-the-blockbuster-drugs

Impressions: 3177

https://www.pharmacompass.com/radio-compass-blog/after-beef-india-may-ban-gelatin-capsules-gsk-gilead-s-hiv-race-heats-up

Impressions: 4737

https://www.pharmacompass.com/radio-compass-blog/price-gouging-by-aspen-in-italy-explosion-at-basf-india-acts-on-illegal-metformin-exports

Impressions: 56504

https://www.pharmacompass.com/radio-compass-blog/top-drugs-by-sales-revenue-in-2015-who-sold-the-biggest-blockbuster-drugs

Impressions: 12778

https://www.pharmacompass.com/radio-compass-blog/who-has-the-biggest-one-sales-of-the-top-pharma-products-by-revenue