X

API Suppliers

US DMFs Filed

CEP/COS Certifications

0

JDMFs Filed

0

EU WC

Listed Suppliers

USA (Orange Book)

Europe

Canada

Australia

South Africa

Uploaded Dossiers

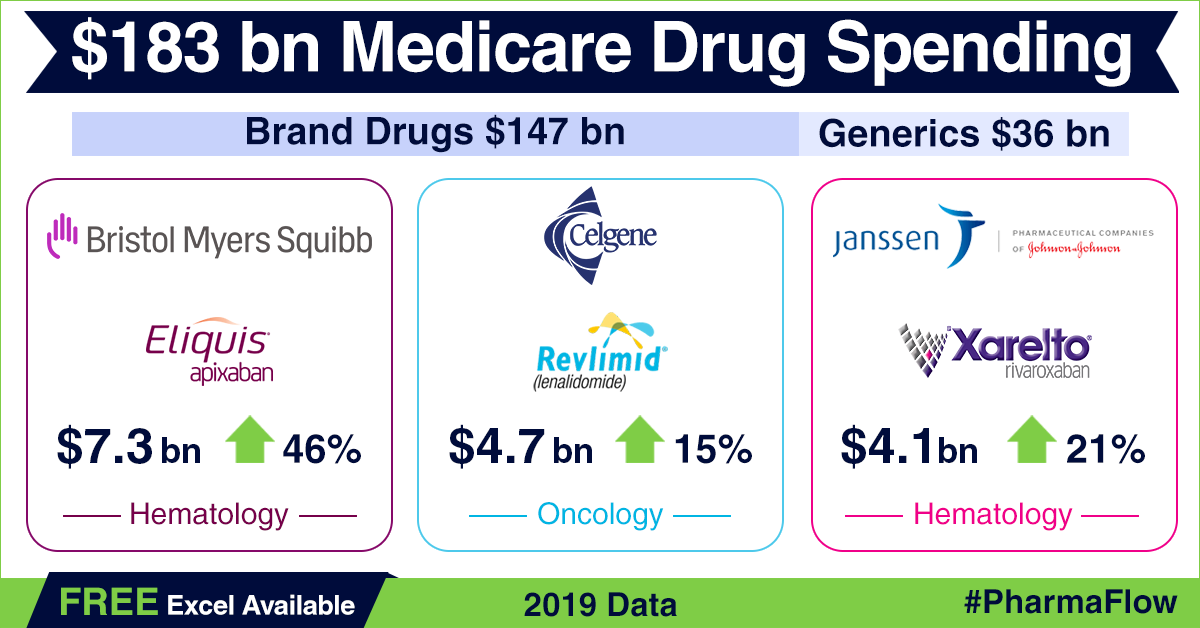

U.S. Medicaid

Annual Reports

0

Impressions: 5192

https://www.pharmacompass.com/radio-compass-blog/top-pharma-companies-and-drugs-in-2022-pfizer-breaks-us-100-billion-barrier-abbvie-s-humira-retains-second-spot

Impressions: 7950

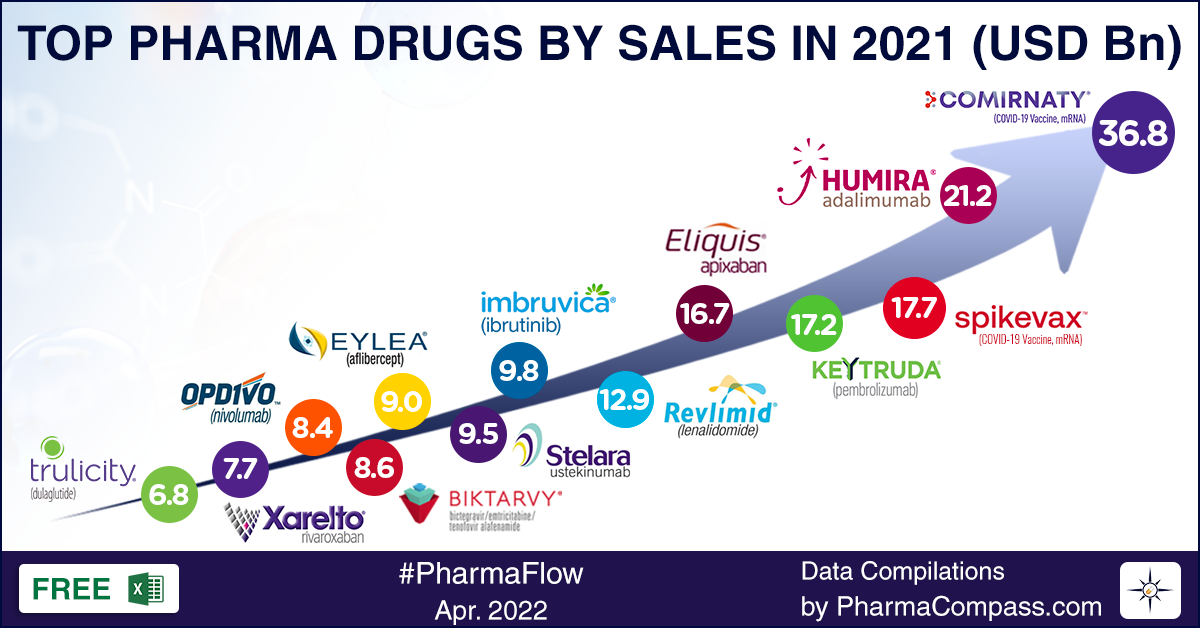

https://www.pharmacompass.com/radio-compass-blog/top-pharma-companies-drugs-in-2021-covid-vaccines-pills-cause-churn-in-list

Impressions: 2629

https://www.pharmacompass.com/radio-compass-blog/america-s-drug-price-hike-conundrum-in-backdrop-of-2019-medicare-part-d-data

Impressions: 54800

https://www.pharmacompass.com/radio-compass-blog/top-drugs-and-pharmaceutical-companies-of-2019-by-revenues

Impressions: 9301

https://www.pharmacompass.com/radio-compass-blog/chemical-entities-shine-in-the-top-10-fastest-growing-drugs-of-2016

Impressions: 4472

https://www.pharmacompass.com/radio-compass-blog/us-dmf-filings-indicate-a-robust-api-industry-with-multiple-first-to-file-challenges

Impressions: 12785

https://www.pharmacompass.com/radio-compass-blog/who-has-the-biggest-one-sales-of-the-top-pharma-products-by-revenue