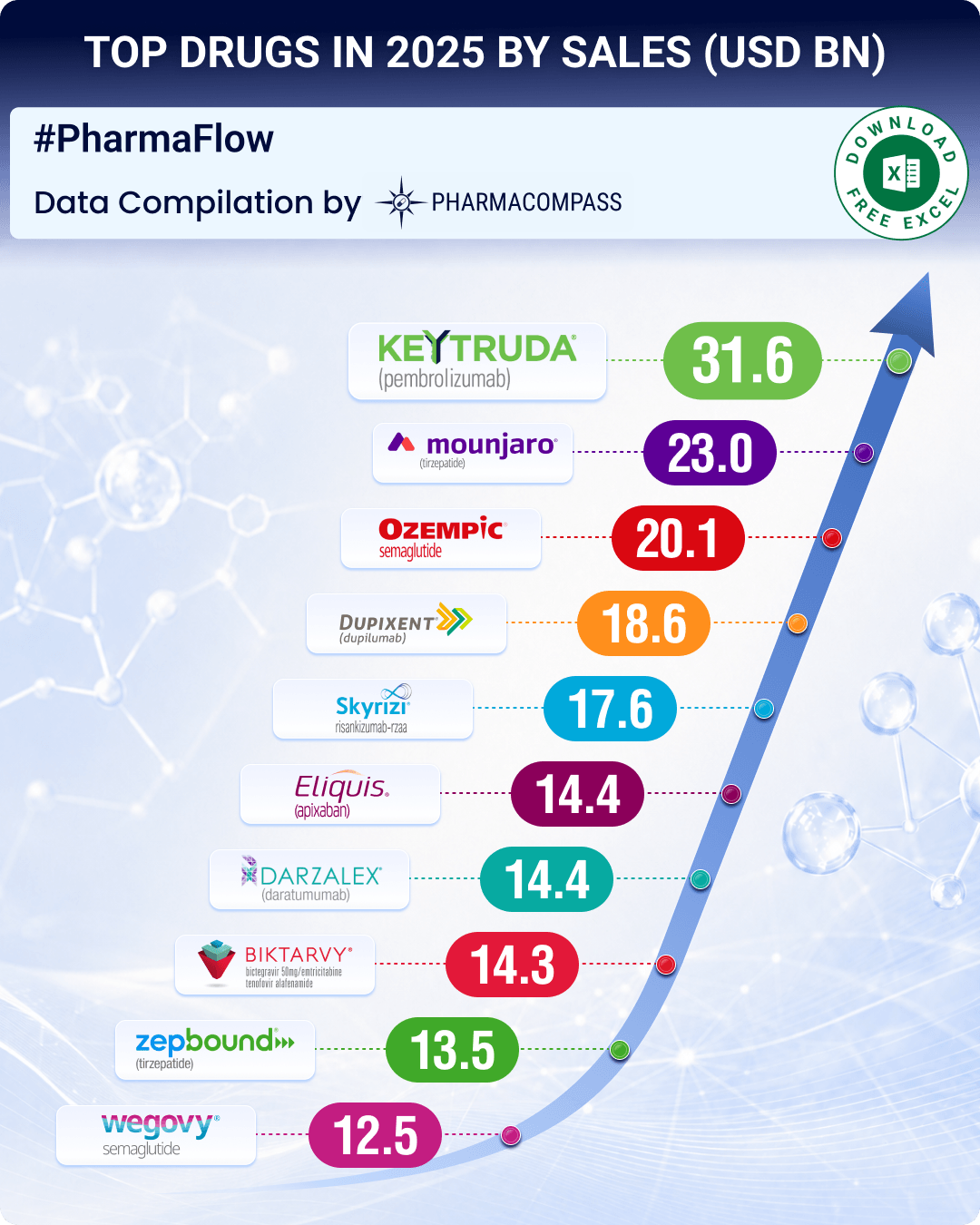

Top Pharma Companies & Drugs in 2025: Lilly vaults eight spots to emerge at the top; GLP-1 drugs dominate list

For the pharmaceutical industry, 2025 was a watershed year

when obesity drugs settled firmly in the

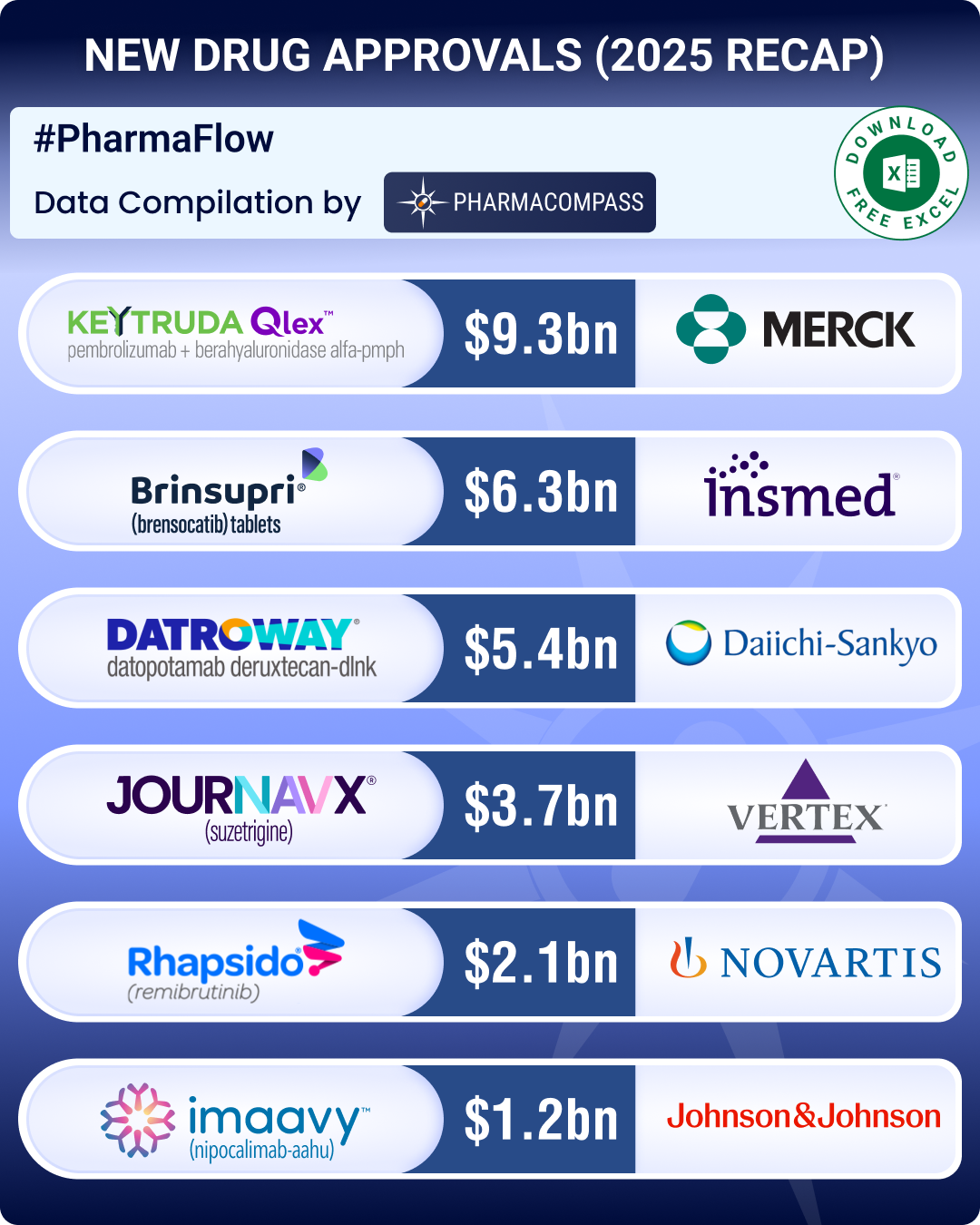

FDA approvals drop 8% in 2025, with fewer blockbusters; Brinsupri, Rhapsido make it to first-in-class list

Our

update for new drug approvals by the US Food and Drug Administration (FDA) in

the first half (

Top news of 2025: Drugmakers invest in US capacities, agree to lower Medicaid prices; Pfizer buys obesity-focused biotech Metsera

The year 2025 was an eventful one, marked by increased trade

tensions, tariff threats, accelerated

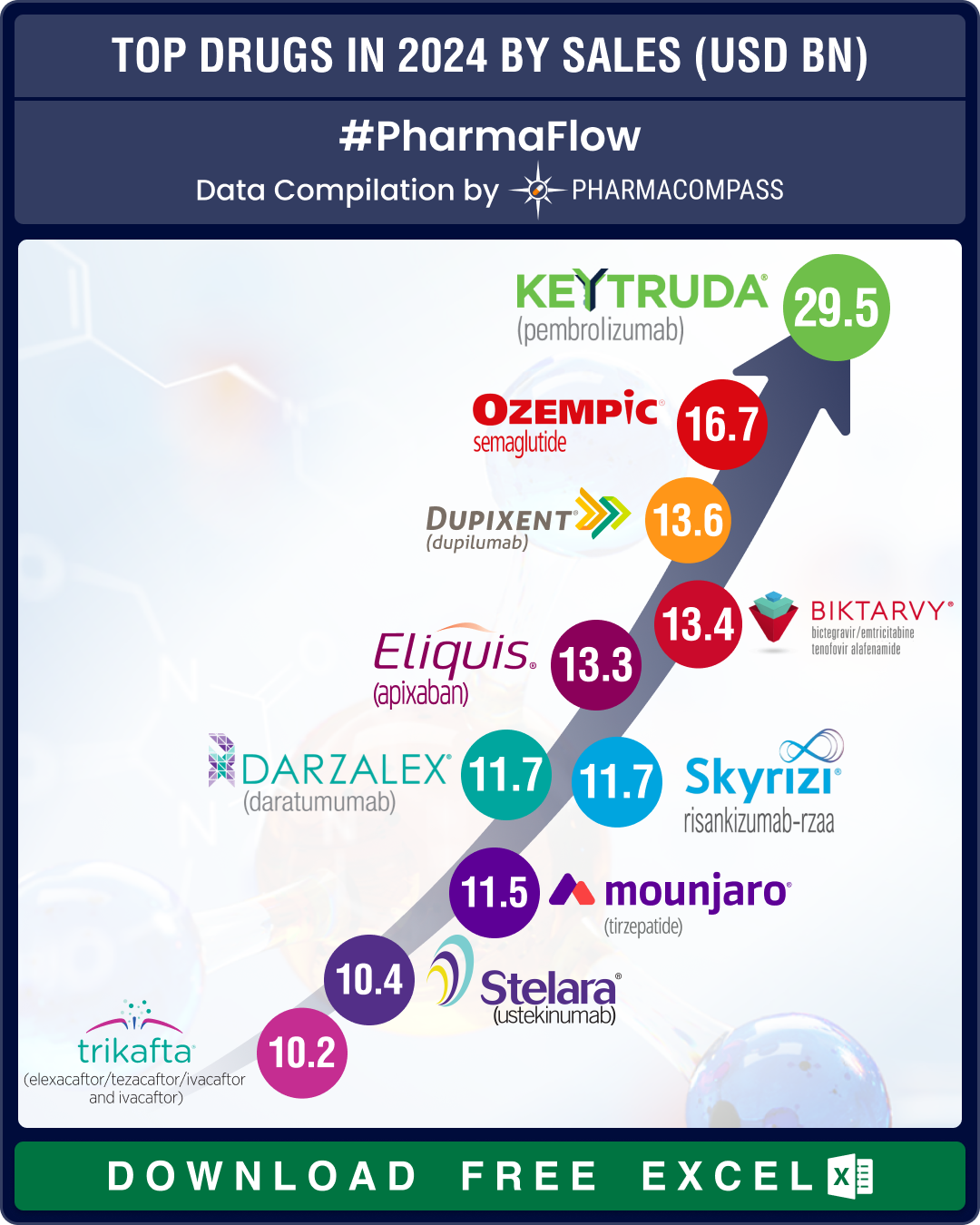

Top Pharma Companies & Drugs in 2024: Merck’s Keytruda maintains top spot as Novo’s semaglutide nips at its heels

In 2024, Big Pharma players consolidated

and maintained their dominance, even as innovation continu

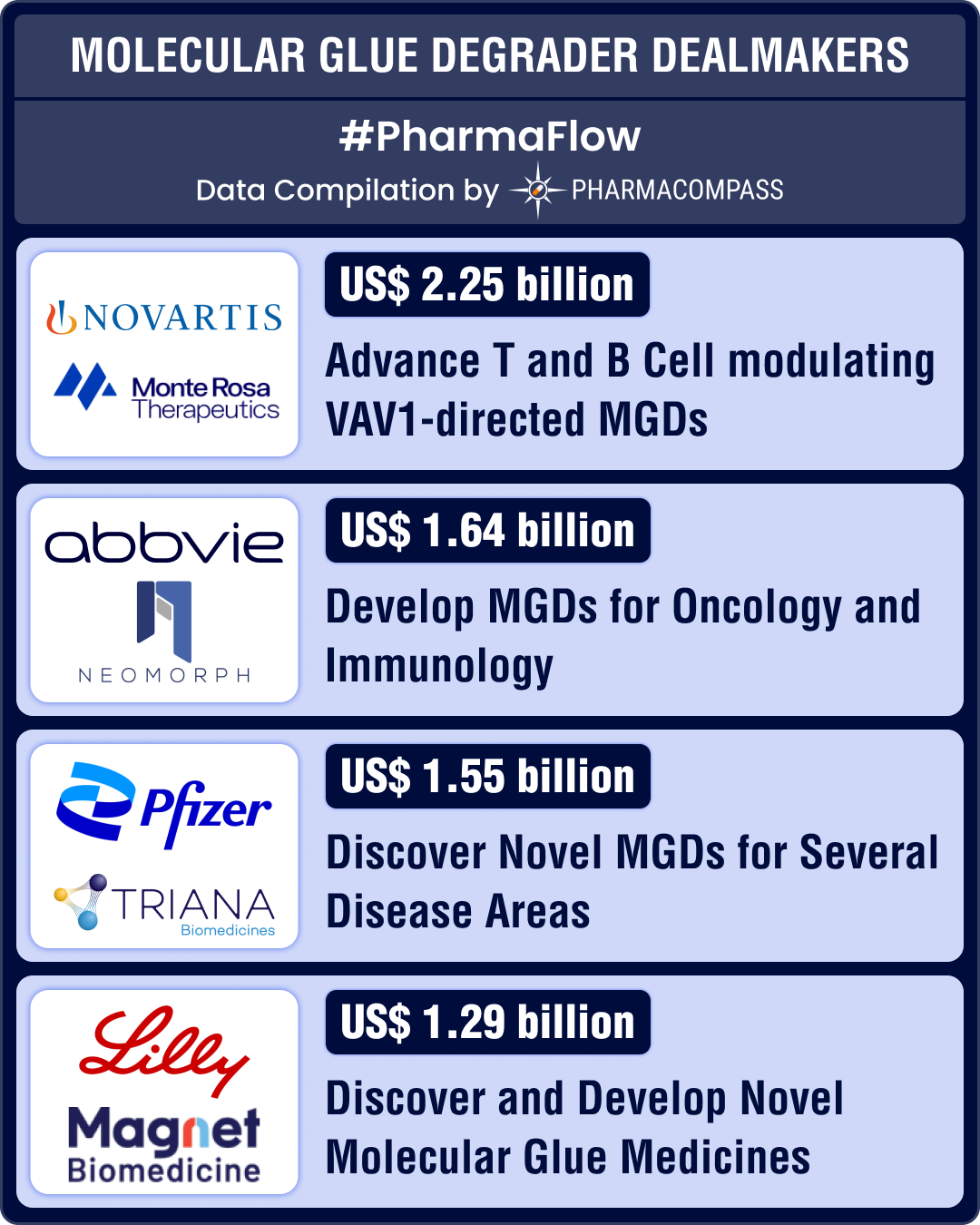

Molecular glue degraders: Lilly, AbbVie sign billion-dollar deals; BMS leads with three late-stage drugs

This week, we delve into molecular glue degraders (MGDs), one of the most promising frontiers in dru

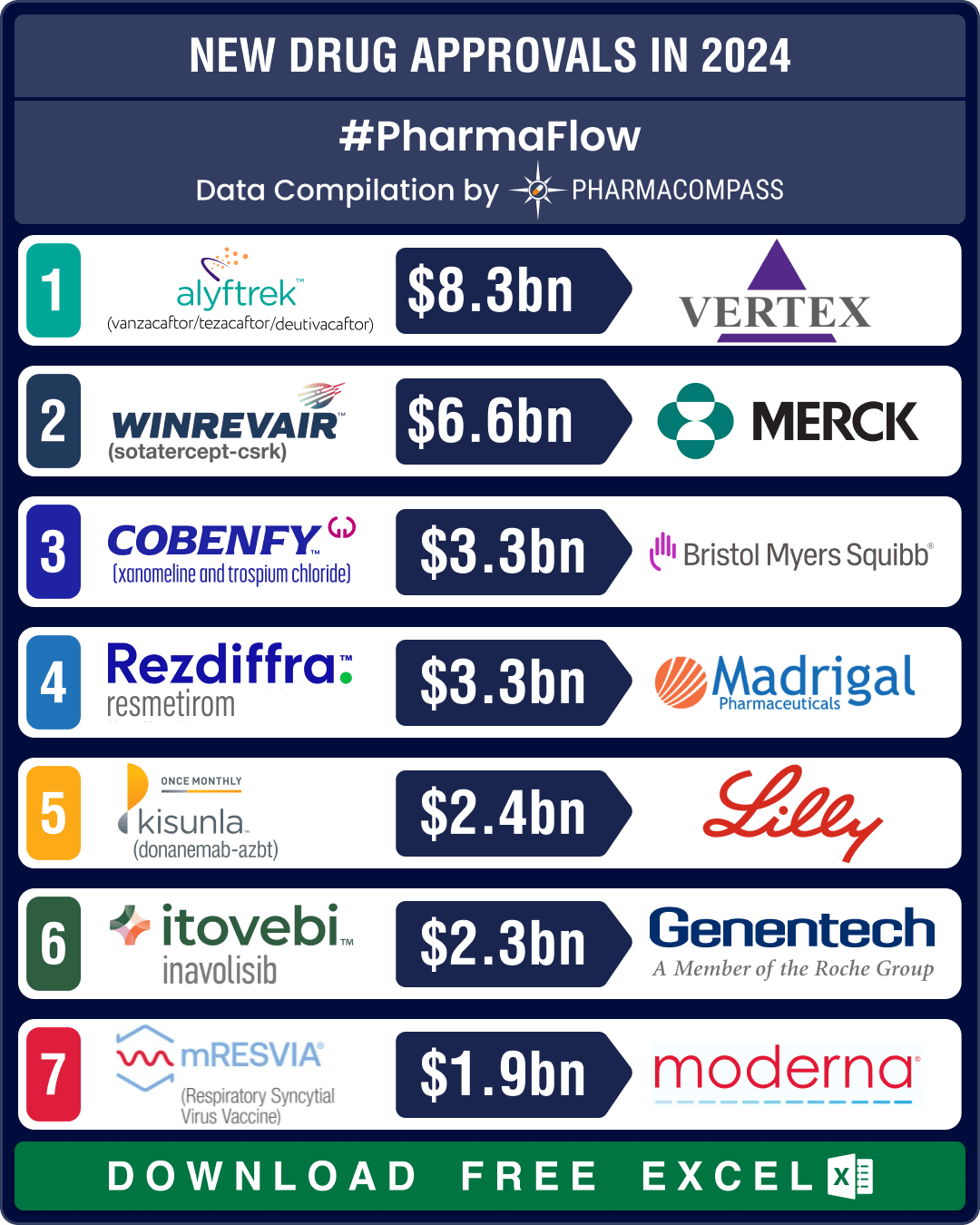

FDA okays 50 new drugs in 2024; BMS’ Cobenfy, Lilly’s Kisunla lead pack of breakthrough therapies

In 2024, the biopharma industry continued to advance on its robust trajectory of innovation. Though

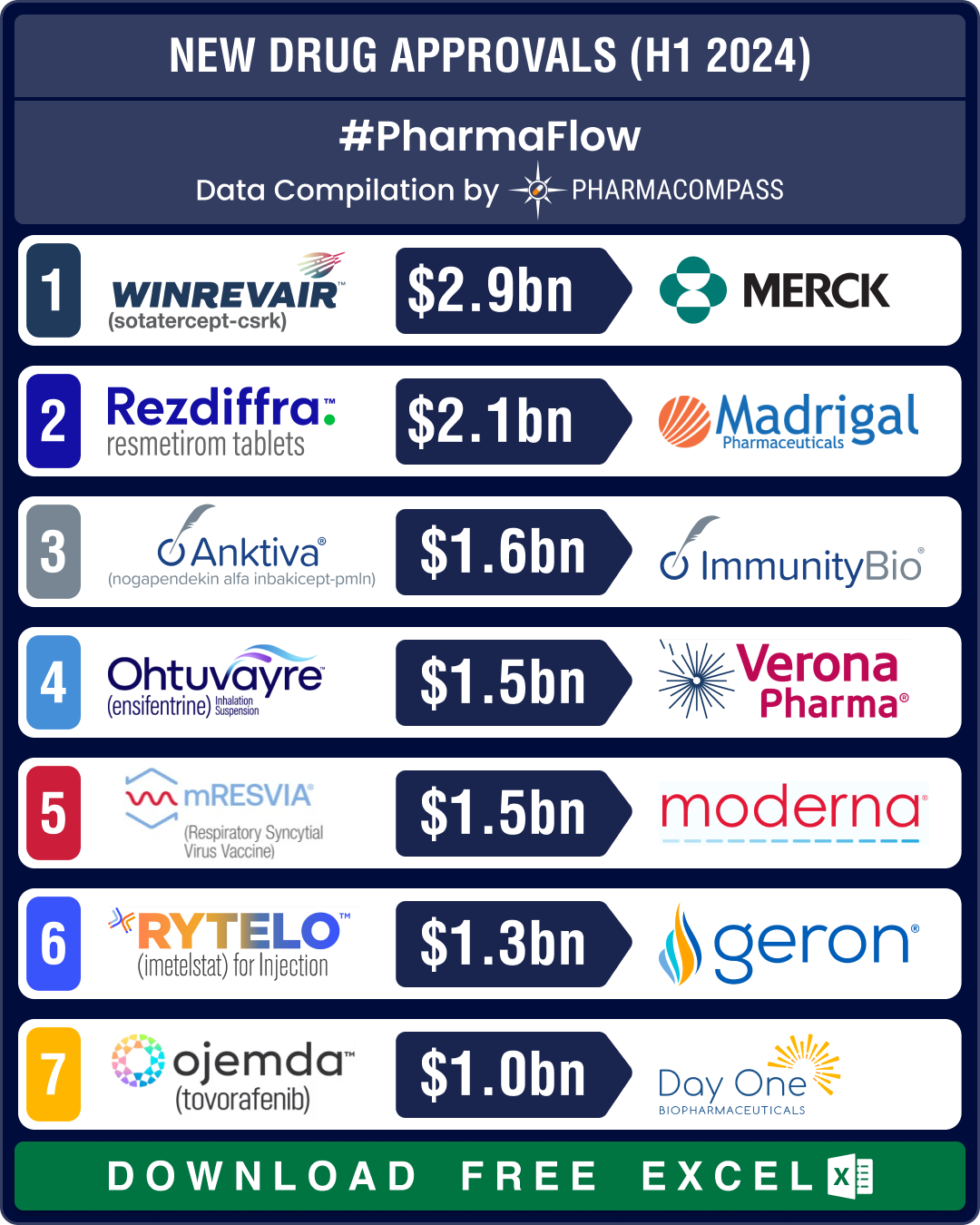

FDA approvals slump 19% in H1 2024; NASH, COPD, PAH get new treatment options

The first half of 2024 saw a significant slowdown in approvals of new drugs and biologics by the US

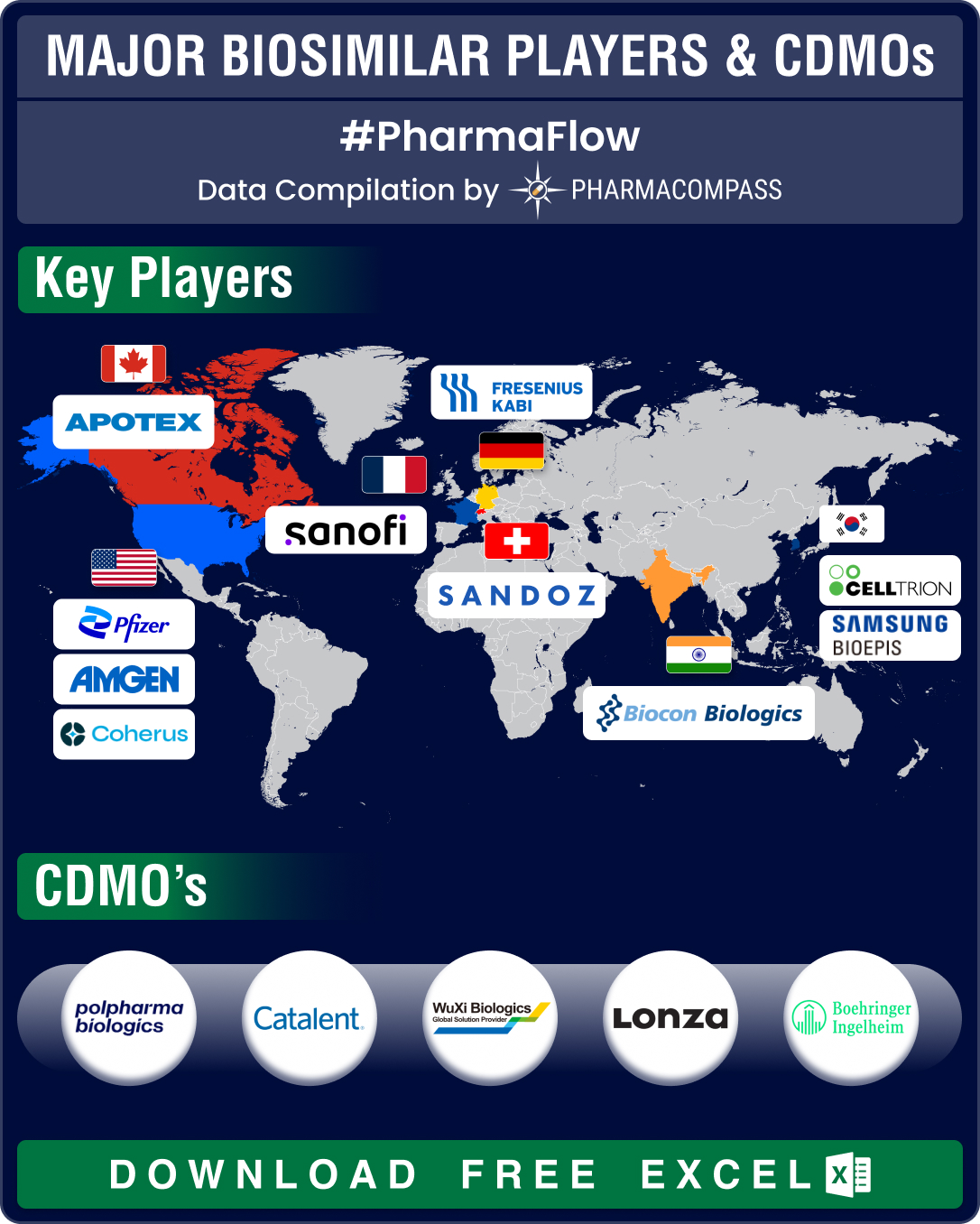

FDA approves record eight biosimilars in H1 2024; okays first interchangeable biosimilars for Eylea

Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of

- Privacy policy

- Terms and conditions

- Disclaimers

-

- Product listings are provided for informational purposes only. We do not supply or sell any products. Any products that may be covered by patent(s) are supplied solely for uses permitted under Section 107A of the Indian Patents Act and not for commercial sale.