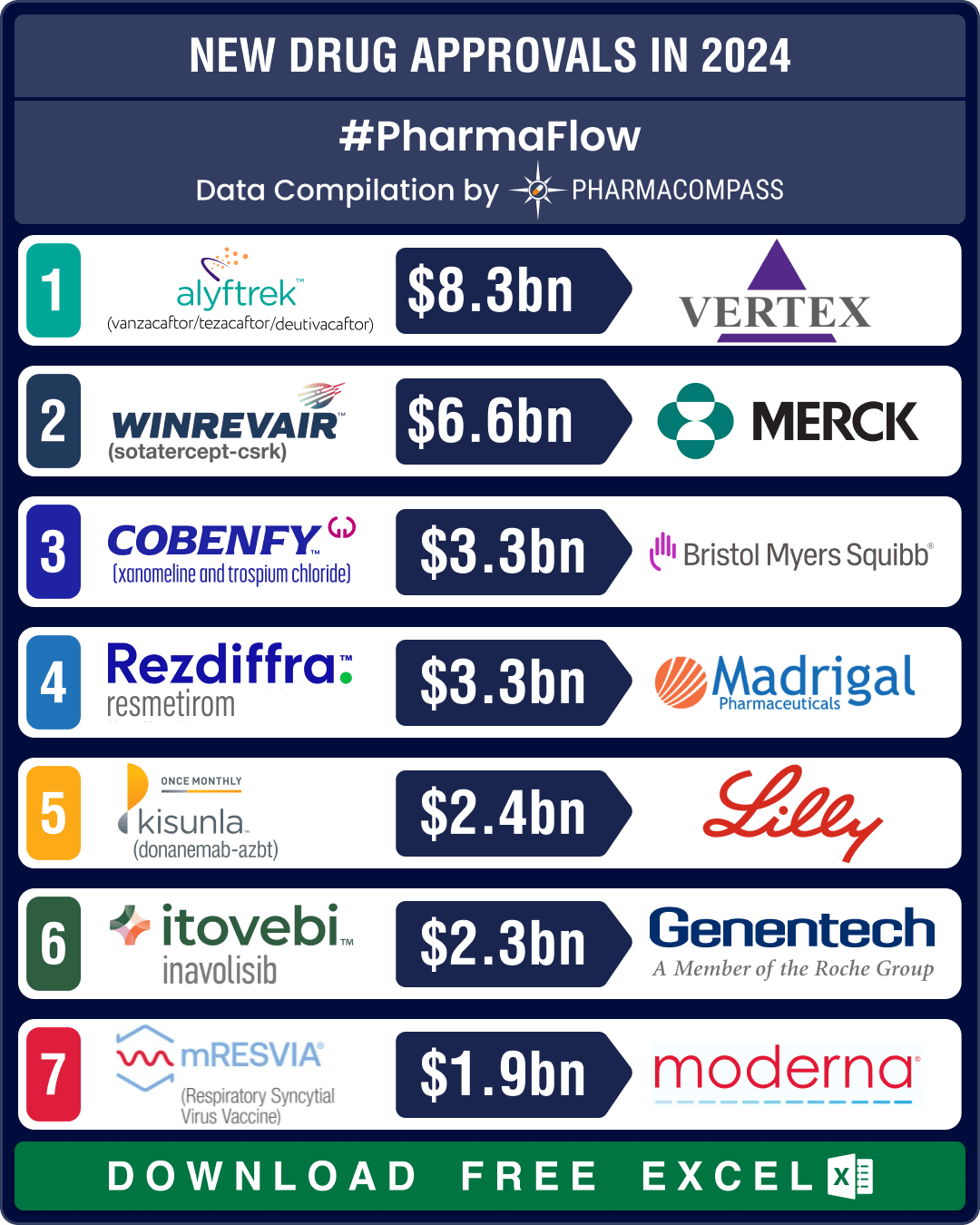

FDA okays 50 new drugs in 2024; BMS’ Cobenfy, Lilly’s Kisunla lead pack of breakthrough therapies

In 2024, the biopharma industry continued to advance on its robust trajectory of innovation. Though

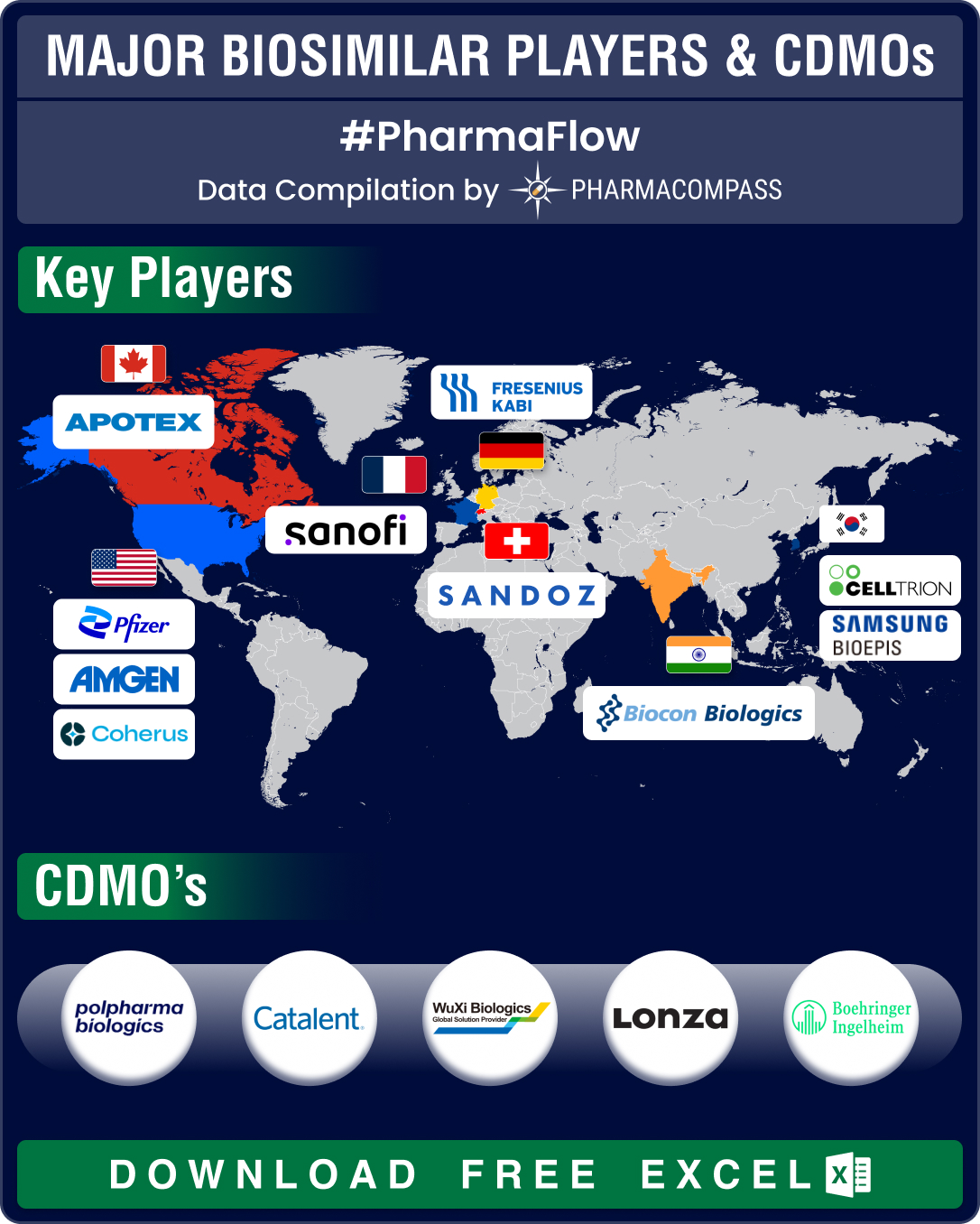

FDA approves record eight biosimilars in H1 2024; okays first interchangeable biosimilars for Eylea

Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of

- Privacy policy

- Terms and conditions

- Disclaimers

-

- Product listings are provided for informational purposes only. We do not supply or sell any products. Any products that may be covered by patent(s) are supplied solely for uses permitted under Section 107A of the Indian Patents Act and not for commercial sale.