After facing the worst year since 2008, biotech indices opened 2023 on a positive note. All the three indices posted gains in January — while the Nasdaq Biotechnology Index (NBI) was up 4.4 percent (at US$ 4,360), the S&P Biotechnology Select Industry Index (SPSIBI) rose 8.7 percent to US$ 6,896 and SPDR S&P Biotech ETF (XBI) increased 9 percent to US$ 88.90. In December 2022, the NBI was down 3.4 percent to US$ 4,213, while XBI had risen only 0.1 percent and SPSIBI had witnessed no change.Several major drugmakers have shared

their financial results for 2022 since last month. Pfizer posted an operational growth of 30 percent with 2022 revenues touching an all-time high of US$ 100.3 billion. Merck posted a 22 percent increase, with sales of Keytruda growing 22 percent to US$ 20.9

billion. GSK generated £29.3 billion (US$ 36.3 billion)

in revenue in 2022, an increase of 13 percent over 2021 figures, and Amgen posted a gain of 1 percent.Drugmakers like Eli

Lilly and Johnson

& Johnson saw a huge drop in sales of their

Covid-19 products. Lilly suffered a 9

percent drop and J&J saw a 4 percent decline in Q4 2022 revenue. More

companies are expected to release their 2022 results this month.Access the Pipeline Prospector Dashboard for January 2023 Newsmakers (Free Excel)Lower 2023 forecast, vaccine’s safety concern hammer Pfizer’s stockDespite the indices showing signs of recovery, stocks of several mega cap companies ended the month in the red. Pfizer’s stock suffered the biggest loss, dropping 14 percent in January, due to an interplay of various factors even as the drug behemoth reported best-ever sales in 2022, owing to its

Covid-19 vaccine Comirnaty and antiviral pill Paxlovid. First, the US Food and Drug

Administration (FDA) and Centers for Disease Control and Prevention (CDC) launched an investigation into the possibility of a stroke in older adults who had received its updated Covid-19 booster shot. Second, despite the stellar results, Pfizer’s forecast for 2023 was lower by 33 percent, with an estimated revenue of US$ 67 to 71 billion. With the pandemic receding, there has been a considerable drop in demand for Covid products. Pfizer’s Covid vaccine partner BioNTech also saw its stock go down 6 percent. The other big loser was AbbVie (drop of 9 percent) – its blockbuster immunology drug Humira (adalimumab) saw its exclusive run come

to an end in the US with Amgen launching a copycat — Amjevita. Seven other biosimilars are

due to be launched later this year.A federal appeals court in Philadelphia blocked J&J’s plan to use the Texas two-step bankruptcy strategy to resolve around 40,000 lawsuits alleging that its talc products cause cancer. In another setback, its Janssen unit halted a late-stage global trial of its HIV vaccine after the

drug was found to be ineffective at preventing infection. All these factors led

to a 8 percent drop in J&J stocks.AstraZeneca’s stock tumbled 6 percent in

January due to factors such as a second cancer lawsuit filed by Bristol Myers Squibb, wherein it claimed Astra’s cancer treatment Imjudo infringes on two patents

related to its blockbuster drug Yervoy. FDA also revoked the emergency use authorization (EUA) for AstraZeneca’s Covid-19 treatment Evusheld, expecting it to fail against the currently dominant Omicron sub-variant.January wasn’t a great month for Merck either, whose stock

plummeted 4 percent. The drugmaker halted a late-stage trial of its blockbuster immunotherapy drug Keytruda in prostate cancer after interim data showed that the drug failed to extend survival or help improve patients’ lives. Meanwhile, the drugmaker said it has identified the source of a potential cancer-causing agent – Nitroso-STG-19 – in its popular diabetes drugs Januvia and Janumet, and plans to

resolve the issue by the end of the year.Access the Pipeline Prospector Dashboard for January 2023 Newsmakers (Free Excel) Bayer gains on sales forecast for Kerendia, Nubeqa;

lawsuit settlements benefit TevaThree large cap companies — Bayer AG (14 percent), Teva (10 percent) and Vertex Pharmaceuticals (12 percent) – posted double digit gains on the bourses last month. Bayer hiked sales targets for two of its meds – heart drug Kerendia and prostate cancer

treatment Nubeqa – to US$ 3.2 billion each.Israeli drugmaker Teva said

it has either already settled with or confirmed participation of 48 US states to move forward with its US$ 4.25 billion proposed national settlement agreement to resolve thousands of lawsuits over its alleged role in the US opioid crisis.Vertex Pharmaceuticals said it plans to file for the US approval of its CRISPR gene-editing therapy exa-cel as a treatment for beta-thalassemia and sickle cell disease in the first quarter. If approved, the drug is expected to generate peak annual sales of over US$ 2 billion. Vertex has already applied for the drug’s authorization in the EU and UK. Vertex is also

testing a non-opioid drug, VX-548, for acute pain in a late-stage trial.Among small cap companies,

Massachusetts-based Theseus Pharmaceuticals posted a 180 percent surge in its stock price in January. The drugmaker

said it plans to release clinical data from a phase 1/2 trial of its lead candidate – THE-630 – for advanced gastrointestinal stromal tumor patients, later this year. Analysts expect THE-630 to compete against Pfizer’s Sutent (sunitinib), with projected sales of over US$ 1

billion by 2035. Theseus is also developing two other early-stage candidates.Access the Pipeline Prospector Dashboard for January 2023 Newsmakers (Free Excel) Accelerated nods bring gains for Biogen, Seagen; Lilly loses on Alzheimer’s setback Biogen’s second Alzheimer’s drug – Leqembi (lecanemab) — received FDA’s accelerated approval to treat patients

who are in the earliest stages of the neurodegenerative disease. However, Eli Lilly’s bid for an accelerated approval pathway for its experimental Alzheimer’s disease drug donanemab suffered a setback. FDA rejected the drug as Lilly did not provide enough data from patients who were treated for at least a year. However, days later Lilly’s cancer drug Jaypirca (pirtobrutinib) won accelerated approval as a treatment for

mantle cell lymphoma, a rare form of blood cancer.

FDA also accepted Lilly-Boehringer Ingelheim’s application for cancer drug Jardiance (empagliflozin) as a treatment for chronic kidney disease (CKD) in adult patients. Overall, while Biogen’s stock was up 5 percent in January, Lilly’s was down 7 percent.In another cancer drug

update, FDA granted accelerated approval to Seagen’s Tukysa (tucatinib) to treat HER2-positive unresectable or metastatic colorectal cancer. Seagen’s stock rose 8 percent last month. And BeiGene’s cancer drug Brukinsa

(zanubrutinib) received an approval in the US as a

treatment for adult patients with chronic lymphocytic leukemia (CLL) or small

lymphocytic lymphoma (SLL), pushing its stock up 11 percent. The drug has also received authorization in the UK.Access the Pipeline Prospector Dashboard for January 2023 Newsmakers (Free Excel) Our viewAs always, the new year began with the JP Morgan Healthcare Conference (San Francisco, January 9 to 12). For the last three years, the conference has been lackluster insofar as M&As were concerned. But this year, there were a number of buyouts – AstraZeneca said it will acquire US-based drug

developer CinCor Pharma for up to US$ 1.8 billion. Italy’s privately-held Chiesi Farmaceutici announced it is

buying Ireland-based rare diseases drugmaker Amryt Pharma for up to US$ 1.48 billion. And Ipsen picked up Albireo for US$ 952 million. Stocks of

CinCor, Amryt and Albireo shot up by over 100 percent following the takeover

news. While we do hope these buyouts signal an uptick

in M&A activity, we also know that drugmakers who made billions from the pandemic

are now facing a steep Covid cliff. Among these are Pfizer, BioNTech, Moderna, Gilead Sciences, AstraZeneca and Merck. The 2022 results announced so far confirm this trend. Insofar as biotech indices are concerned, we hope January has set the tone for the coming months.Access the Pipeline Prospector Dashboard for January 2023 Newsmakers (Free Excel)

Impressions: 1639

https://www.pharmacompass.com/pipeline-prospector-blog/pipeline-prospector-jan-2023-mega-cap-drugmakers-face-rout-at-bourses-even-as-biotech-indices-inch-upwards

#PipelineProspector by PharmaCompass

09 Feb 2023

We at PharmaCompass

are pleased to announce the launch of Pipeline Prospector, in

collaboration with SCORR Marketing,

a leading health science marketing agency.

The Pipeline Prospector

is a free-access database of global drug development deals and updates designed

for executives in the drug development industry. Our database will be updated

every month. The first of this two-part rollout of the initial version of the

Pipeline Prospector delivers access to a database of current deals and

developments. In the second phase, we will add pipeline data to provide more

in-depth therapeutic information.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

We begin 2020 with a

compilation of all the major deals and developments which were announced in

January.

Dealmakers at JPMorgan

Historically, January is the month of the annual JPMorgan Healthcare Conference in San Francisco — a platform where drug majors tend to announce significant deals and strategic shifts. Last year witnessed the US$ 74 billion acquisition of New Jersey-based cancer drug company Celgene by Bristol-Myers Squibb. After factoring in debt, the value of

the deal ballooned to about US$ 95 billion, which according to data compiled by

Refinitiv, was the largest healthcare deal on record.

This year started on

a muted note with Eli Lilly’s all-cash acquisition of California-based Dermira Inc being one of the only major deals. The acquisition will

allow Eli Lilly to expand its

immunology pipeline with a late-stage treatment for atopic dermatitis.

The acquisition gives

Lilly two key Dermira assets — lebrikizumab and Qbrexza (glycopyrronium)

cloth. Lebrikizumab is a novel, investigational, monoclonal antibody

designed to bind IL-13, which is believed to be a driver of signs and symptoms

of atopic dermatitis. It is currently in two Phase III trials for the treatment

of moderate-to-severe atopic dermatitis in adolescent and adult patients, aged

12 years and older.

In late 2019, FDA

granted fast-track designation to lebrikizumab, and analysts are

of the view that the drug could be a challenger to Dupixent, a skin drug made by Regeneron and Sanofi that is expected to bring in over US$ 11

billion in annual sales.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

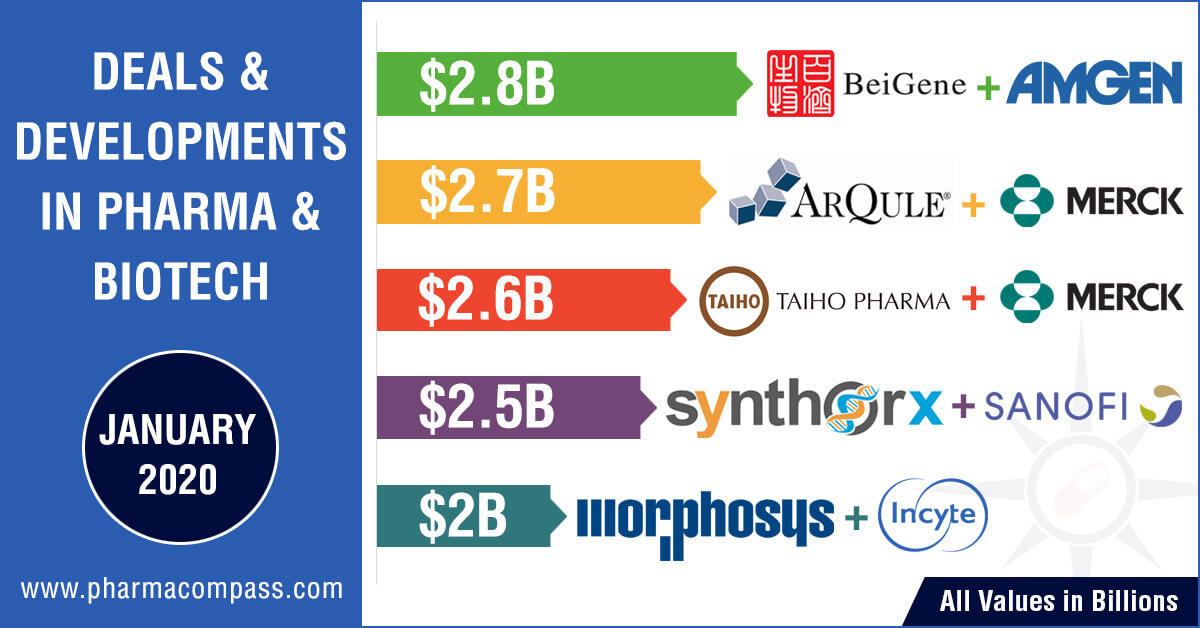

At the JPMorgan

conference, Incyte and MorphoSys announced a collaboration and licensing agreement to further develop and commercialize MorphoSys’ proprietary anti-CD19 antibody tafasitamab (MOR208) globally.

Tafasitamab is an

Fc-engineered antibody against CD19 currently in clinical development for the

treatment of B cell malignancies. MorphoSys and Incyte will co-commercialize

tafasitamab in the US, while Incyte has exclusive commercialization rights

outside of the US.

As per the agreement,

MorphoSys will receive

an upfront payment of US$ 750 million. In addition, Incyte will make an equity

investment into MorphoSys to the tune of US$ 150 million. Depending on the

achievement of certain developmental, regulatory and commercial milestones,

MorphoSys will be eligible to receive milestone payments amounting to nearly

US$ 1.1 billion. MorphoSys will also receive tiered royalties on ex-US net

sales of tafasitamab in a mid-teens to mid-twenties percentage range of net

sales.

An approval for

tafasitimab could come as soon as mid-2020, according to MorphoSys, which

submitted the drug to the US Food and Drug Administration in late 2019.

Around the same time

as these deals were announced, Biogen placed another bet on Alzheimer’s R&D by

paying Pfizer US$ 75 million upfront for a candidate currently in Phase I

trials.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

Amgen’s China bet

January also saw the

completion of two previously announced US$ 2.7 billion deals. As China, the

world’s second largest pharmaceutical market,

continues to remain a key growth area for Big Pharma, Amgen completed its acquisition of a 20.5 percent stake in the Chinese biotechnology firm Beigene worth approximately US$ 2.7 billion. The deal will give

Amgen’s cancer drugs greater exposure to the

Chinese market and also allow the firm to profit if BeiGene’s pipeline of molecularly targeted and

immuno-oncology products prove to be effective and ready for commercialization.

A month after Amgen

had announced its investment in BeiGene, the FDA approved BeiGene’s cancer therapy zanubrutinib (branded as Brukinsa) months ahead of

schedule. This was the first-ever FDA approval for a cancer therapy developed

by a Chinese biotech.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

Merck’s oncology focus

US-headquartered Merck, which is known as MSD (short for Merck Sharp

& Dohme) outside the United States and Canada, completed its acquisition of ArQule through its subsidiary for US$ 2.7 billion.

ArQule focusses on

kinase inhibitor discovery and development for the treatment of patients with

cancer and other diseases. The deal gives Merck access to ArQule’s experimental treatment ARQ 531 — a novel, oral Bruton’s tyrosine

kinase (BTK) inhibitor currently in a Phase 2 dose expansion study for the

treatment of B-cell malignancies.

In January, Merck

also announced an alliance with

Japanese drugmakers Taiho Pharmaceutical and Astex Pharmaceuticals (a wholly owned subsidiary of Otsuka Pharmaceutical). The American drugmaker said it is

willing to invest up to US$ 2.5 billion in order to gain

access to small-molecule inhibitors against several drug targets, including the

KRAS oncogene, from Taiho and Astex.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

According to a statement, Taiho, Astex and Merck will combine preclinical candidates and their data “with knowledge and expertise from their respective research programs.”

In exchange for giving Merck an exclusive global license to their small-molecule inhibitor candidates, Taiho and Astex will get US$ 50 million upfront, with the US$ 2.5 billion “contingent upon the achievement of preclinical, clinical, regulatory and sales milestones for multiple products arising from the agreement, as well as tiered royalties on sales.”

“Merck will fund research and development and will be responsible for commercialization of products globally,” the statement said. Taiho has retained co-commercialization rights in Japan and an option to promote the drugs (coming out of this alliance) in specific areas of South East Asia.

KRAS is short for the

gene Kirsten rat sarcoma viral oncogene homolog, which makes a protein

(KRAS protein) that is critical in promoting cell growth and survival in

non-cancerous cells. Cancers driven by KRAS mutations are both common and

deadly.

The year 2019 was a big one for KRAS, when several players — such as Amgen, Boehringer Ingelheim, Eli Lilly and Mirati — had reported progress in the field. For

instance, Amgen had reported encouraging anti-tumor activity with its AMG

510 candidate, which targets a KRAS mutation known as G12C.

In September last year, Boehringer Ingelheim (BI) had licensed an MEK inhibitor

from Indian drugmaker Lupin that it intends to pair with its lineup

of KRAS inhibitors. BI had also entered into a partnership with MD Anderson

Cancer Centre in the US for another KRAS inhibitor.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

Acceleron’s shares skyrocket

The share price of Boston-based Acceleron almost doubled in the month of January

when new Phase 2 data on the success of an experimental heart drug, sotatercept, found a statistically significant

decrease in pulmonary vascular resistance in patients with pulmonary arterial

hypertension(PAH).

Pulmonary arterial

hypertension (PAH) is a rare, progressive disorder characterized by high blood

pressure (hypertension) in the arteries of the lungs (pulmonary artery) for no

apparent reason. The pulmonary arteries are the blood vessels that carry blood

from the right side of the heart through the lungs.

In November 2019, the

FDA approved Acceleron’s luspatercept (brand name Reblozyl) for the treatment

of anemia among patients with beta-thalassemia who require regular red blood

cell transfusions. The approval provides patients with a therapy that, for the

first time, will help decrease the number of blood transfusions.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

Setback for France’s Ipsen and Nektar Therapeutics

French drugmaker Ipsen announced it was pausing a phase III trial of palovarotene, an experimental rare bone disease drug,

after an interim analysis found it is unlikely to meet its primary efficacy

endpoint. The decision to pause the trial is based on the results of a futility

analysis reviewed by the Independent Data Monitoring Committee (IDMC).

The announcement

marked yet another blow for palovarotene, which had run into safety and efficacy

problems since Ipsen acquired it in a US$ 1.3 billion (€1.1 billion) takeover of Clementia Pharmaceuticals. In

December, a safety concern prompted the FDA to halt dosing in children.

At the time of acquiring Clementia last year, David Meek, the then CEO of Ipsen, had called the drug “a largely derisked asset”. Since then, palovarotene has been the subject of a safety signal that led the FDA to stop the trial in children, a key population. The drug has now been rocked by an analysis that questions its efficacy.

Access the Pipeline Prospector Dashboard for All Deals &

Development Updates

Last month, we also

witnessed a major setback for Nektar Therapeutics as a joint FDA advisory committee voted

27-0 against the approval of oxycodegol for chronic low back pain.

Oxycodegol’s key selling point was that its central nervous system absorption rate was much slower than that of the other often abused

opioid drugs.

The focus on drug

development is constantly evolving and the Pipeline Prospector, our free access

database of global drug development deals and development updates, is designed

to provide the insights necessary for professionals to drive their business

forward.

Email us at support@pipelineprospector.com to learn more.

Access the Pipeline

Prospector Dashboard for All Deals & Development Updates

Impressions: 3690

https://www.pharmacompass.com/pipeline-prospector-blog/pipeline-prospector-jan-2020-deals-and-developments-in-pharma-and-biotech

#PipelineProspector by PharmaCompass

13 Feb 2020