For the pharmaceutical industry, 2025 was a watershed year

when obesity drugs settled firmly in the mainstream market. Glucagon-like

peptide-1 (GLP-1) receptor

agonists that treat diabetes and help in weight loss, dominated our top 10 list of drugs with four entries — Mounjaro (tirzepatide), Ozempic (semaglutide), Zepbound (tirzepatide) and Wegovy (semaglutide).In 2024, the top 10 drugs generated a total revenue of US$ 142

billion. This figure rose significantly in 2025,

climbing to US$

180.02 billion, reflecting strong growth.The year unequivocally belonged to Eli Lilly. The

Indiana-headquartered drugmaker made a

dramatic ascent, leaping from the ninth spot in 2024 to the numero uno position in our top drugmakers’ list for 2025. It posted 45 percent growth in sales, which rose to US$

65.18 billion in 2025.In terms of therapeutic areas, oncology saw the maximum

sales (at US$ 229.1 billion), followed by immunology (US$ 126.8 billion),

infectious diseases (US$ 99.2 billion), diabetes (US$ 95.8 billion), neurology

(US$ 70.4 billion), cardiology (US$ 67.6 billion) and hematology (US$ 29.3

billion). View Our Interactive Dashboard on Top Drugs in 2025 by Sales (Free Excel Available)Lilly zooms past Pfizer on back of tirzepatide franchise; Roche, AbbVie, J&J make it to top five Eli Lilly’s spectacular climb to the number one spot was driven by Mounjaro and Zepbound. Mounjaro leapt from the eighth spot in 2024 (when its sales stood at US$ 11.5 billion) to the number two position in 2025, raking in US$ 23 billion. Lilly’s other GLP-1 drug, Zepbound, also broke into the top 10, debuting at number nine with sales of US$ 13.5 billion. Taken together, Lilly’s tirzepatide franchise

hit US$

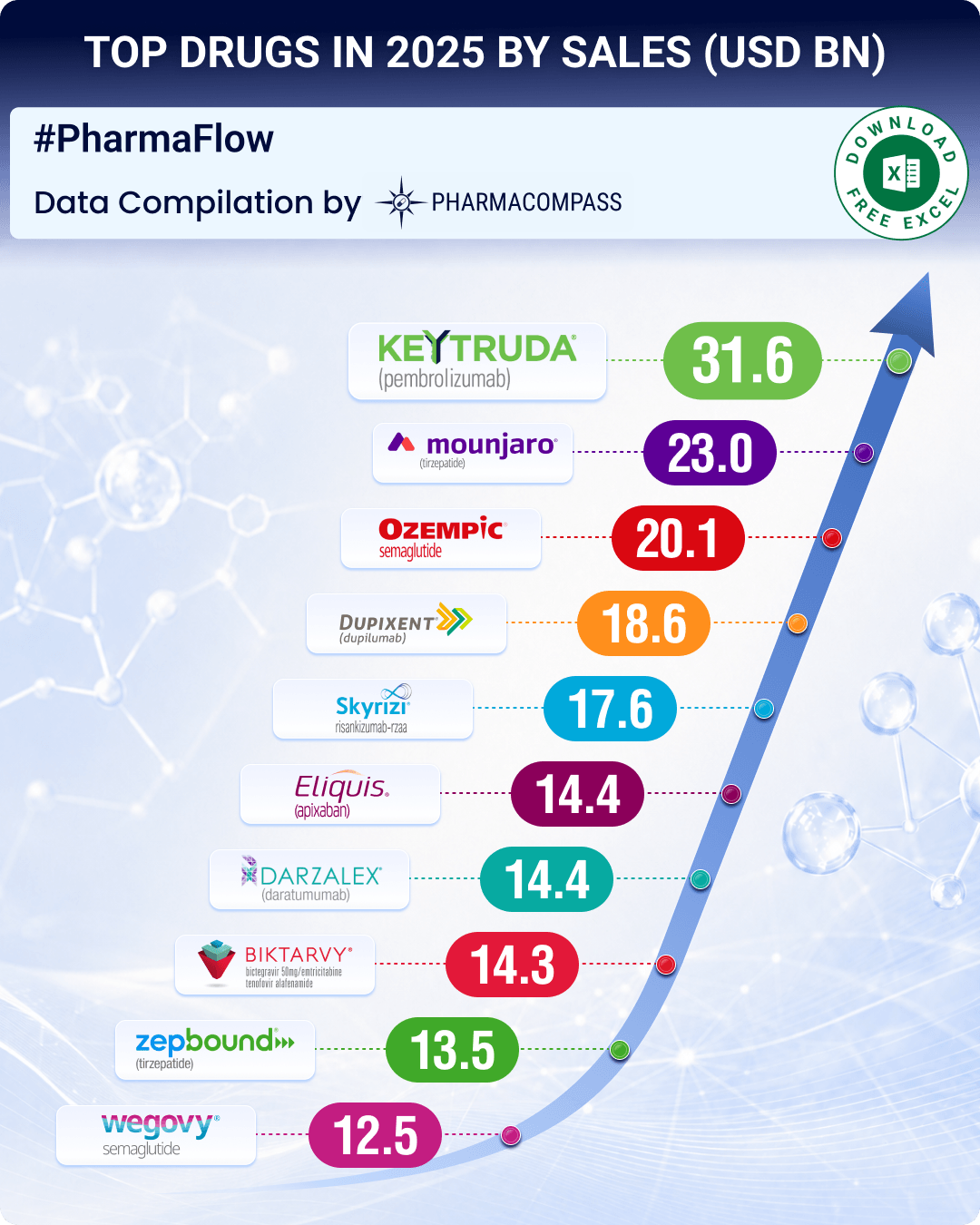

36.50 billion in 2025, surpassing Merck's Keytruda

(pembrolizumab).At the number two position was Pfizer, with sales of US$ 62.58 billion. Notably, not a single Pfizer drug made it to the top 10 list. Pfizer’s sales fell by 1.63

percent in 2025, from US$ 63.63 billion in 2024. The decline was attributed to lower Covid‑19 revenues due to reduced infection

rates, which impacted Paxlovid (nirmatrelvir/ritonavir) sales,

and a narrower US vaccine recommendation, which affected Comirnaty

(tozinameran) sales.Roche came

third, reporting sales of CHF 47.7

billion (US$ 62.10 billion) in 2025, compared to CHF 46.2 billion (US$ 50.86 billion) in 2024.At number four was AbbVie — it reported full-year net revenues of US$

61.16 billion in 2025, compared to US$ 56.33 billion in 2024. The company’s immunology portfolio remained a key driver, bringing in US$

30.41 billion in sales. Skyrizi (risankizumab) — approved for plaque psoriasis, psoriatic arthritis, Crohn’s disease, and ulcerative colitis — emerged as a major

growth engine, with sales of US$ 17.56 billion.Rounding out the top five was Johnson & Johnson, whose innovative medicine division

reported sales of US$ 60.4

billion, up from US$ 56.9 billion in 2024. View Our Interactive Dashboard on Top Drugs in 2025 by Sales (Free Excel Available)Merck’s Keytruda retains top-selling drug status, followed by Lilly’s Mounjaro, Novo’s OzempicMerck’s Keytruda retained

its position as the world’s best-selling drug for the third consecutive year, generating approximately US$ 31.6 billion in sales, up from US$ 29.5

billion in 2024 and US$ 25

billion in 2023. Keytruda has become the pillar of

cancer immunotherapy, with over 40 indications. The launch of Keytruda Qlex, a subcutaneous

formulation co-administered with berahyaluronidase alfa,

has further strengthens its lifecycle.Amongst other oncology drugs, J&J’s Darzalex (daratumumab)

generated US$ 14.4 billion in sales, taking

it to the number seven spot. Its strong performance has been supported by

Darzalex Faspro, a subcutaneous formulation launched in 2020 that significantly

reduces administration time. Growth from Darzalex and other brands helped

offset the decline in Stelara (ustekinumab), whose

sales fell 41 percent to US$ 6.1 billion, from US$ 10.4 billion in 2024.Among diabetes, obesity and metabolic drugs, Lilly’s Mounjaro was at the number two spot, followed by Novo Nordisk’s Ozempic at number three. Ozempic posted sales of US$ 20.09 billion. Lilly’s Zepbound was at the ninth spot, with sales of US$ 13.54 billion. Novo’s Wegovy was tenth, with sales of US$ 12.5 billion. Together with Rybelsus, Novo’s semaglutide franchise

generated approximately US$ 36.1 billion in 2025 sales.In immunology, Sanofi and Regeneron’s Dupixent

(dupilumab) stood

fourth and maintained

its leadership with sales of US$ 18.6 billion.

Dupixent is now approved across nine indications.At fifth position was another immunology drug — AbbVie’s Skyrizi (risankizumab). It has

emerged as AbbVie’s key growth engine post‑Humira (adalimumab),

delivering 49.87 percent growth and generating US$ 17.56 billion in 2025 sales.

First approved in April 2019 for plaque psoriasis, it is now approved across

four indications.The other drugs in our top 10 list were Eliquis (apixaban) and Biktarvy

(bictegravir/emtricitabine/tenofovir

alafenamide). Eliquis, co-developed

and commercialized by Bristol

Myers Squibb and Pfizer, stood sixth with sales of US$ 14.4

billion. Gilead’s Biktarvy

(bictegravir/emtricitabine/tenofovir alafenamide) held the number eight

position, with sales of

US$ 14.3 billion in 2025. The drug commands over 52

percent of the US market for HIV treatments. View Our Interactive Dashboard on Top Drugs in 2025 by Sales (Free Excel Available)Astra’s revenue rises by 8.6 percent; Merck, Novartis, Sanofi, Novo make it to top 10 AstraZeneca’s revenues increased 8.6 percent to US$ 58.73 billion, compared to US$ 54.10 billion in 2024, though its ranking fell from fifth to sixth position in 2025. Astra’s revenue growth was driven by strong performance across oncology, cardiovascular, renal and metabolism, respiratory and immunology, and rare disease portfolios. Farxiga (dapagliflozin), a drug

used to manage blood sugar, was a key driver, generating US$ 8.4

billion in revenue in 2025.At number seven was Merck, with sales of

US$ 58.1 billion, reflecting a modest growth of 1.3

percent, which was driven by Keytruda.Novartis stood

eighth on our 2025 list (against seventh in 2024),

with net sales of US$ 54.5

billion in 2025, up from US$ 50.3

billion in 2024. Sanofi landed at the ninth position,

with sales of US$ 51.7

billion, against US$ 42.6 billion in 2024. Novo

Nordisk rounded out the top ten, posting revenues of DKK

309.06 bn (US$ 48.7 billion) in 2025 — a growth of 21.37 percent compared to DKK 290.40 billion (US$ 40.2 billion) in 2024 — driven primarily by its obesity and diabetes care portfolio. View Our Interactive Dashboard on Top Drugs in 2025 by Sales (Free Excel Available)Our viewThe 2025 rankings confirm what analysts have been expecting for some time — that the market for anti-obesity drugs could reach

US$ 100 billion by 2030. The four GLP-1 drugs in our 2025 list

together generated combined revenue of approximately US$ 70 billion. At this

pace, the US$ 100 billion market size may arrive sooner than projected, perhaps

as early as 2026 or 2027.