X

API Suppliers

US DMFs Filed

0

CEP/COS Certifications

0

JDMFs Filed

0

Other Certificates

0

Other Suppliers

0

USA (Orange Book)

Europe

0

Canada

Australia

South Africa

Uploaded Dossiers

U.S. Medicaid

Annual Reports

Impressions: 3407

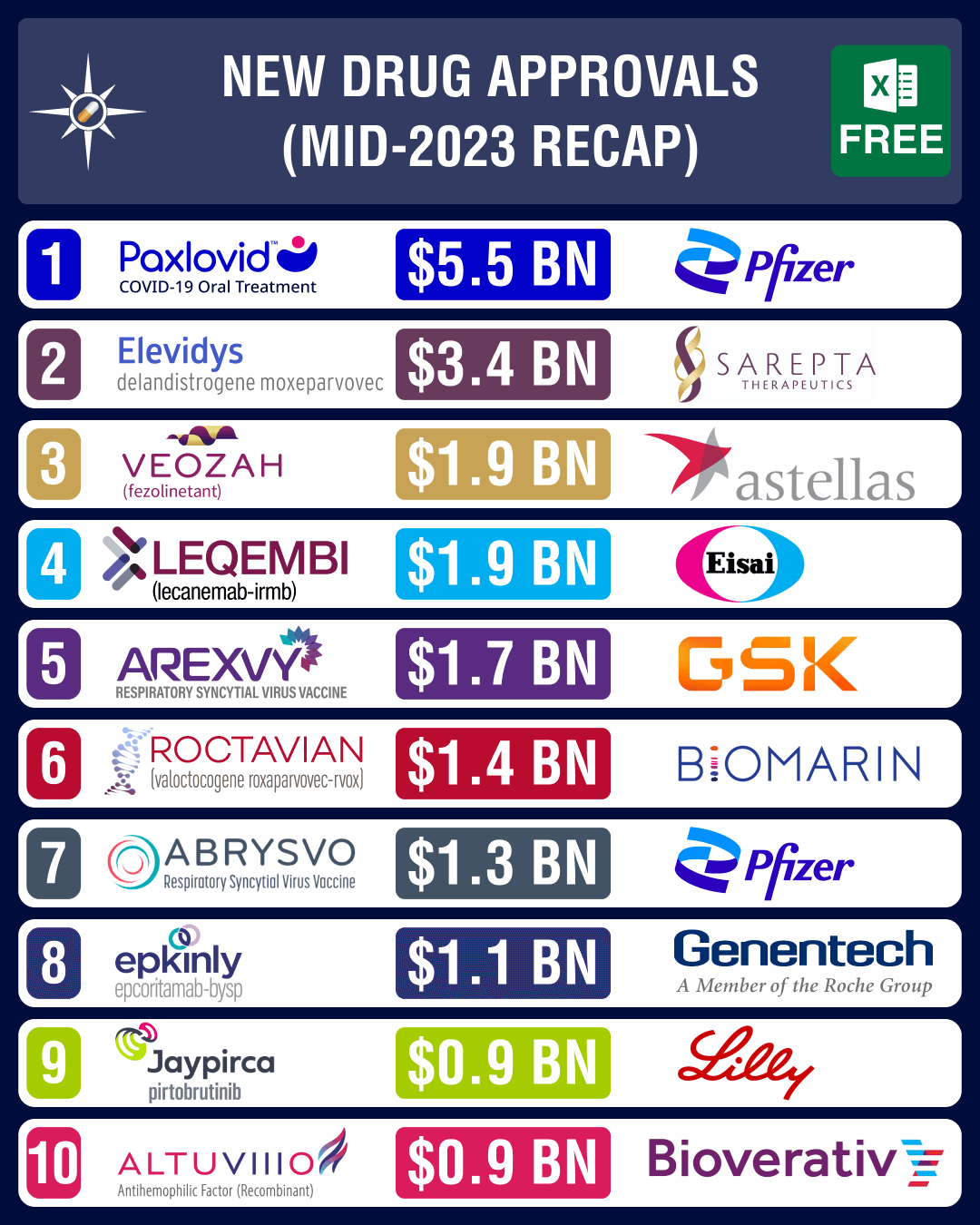

https://www.pharmacompass.com/radio-compass-blog/fda-reports-62-5-growth-in-new-drug-approvals-in-h1-2023-ema-health-canada-see-drop

Impressions: 2704

https://www.pharmacompass.com/radio-compass-blog/company-tracker-pfizer-turns-to-acquisitions-as-covid-products-sales-nosedive

Impressions: 3546

https://www.pharmacompass.com/radio-compass-blog/top-100-pharma-biotech-deals-in-2022

Impressions: 1501

https://www.pharmacompass.com/radio-compass-blog/amgen-ends-humira-s-20-year-reign-in-us-with-amjevita-launch

Impressions: 2695

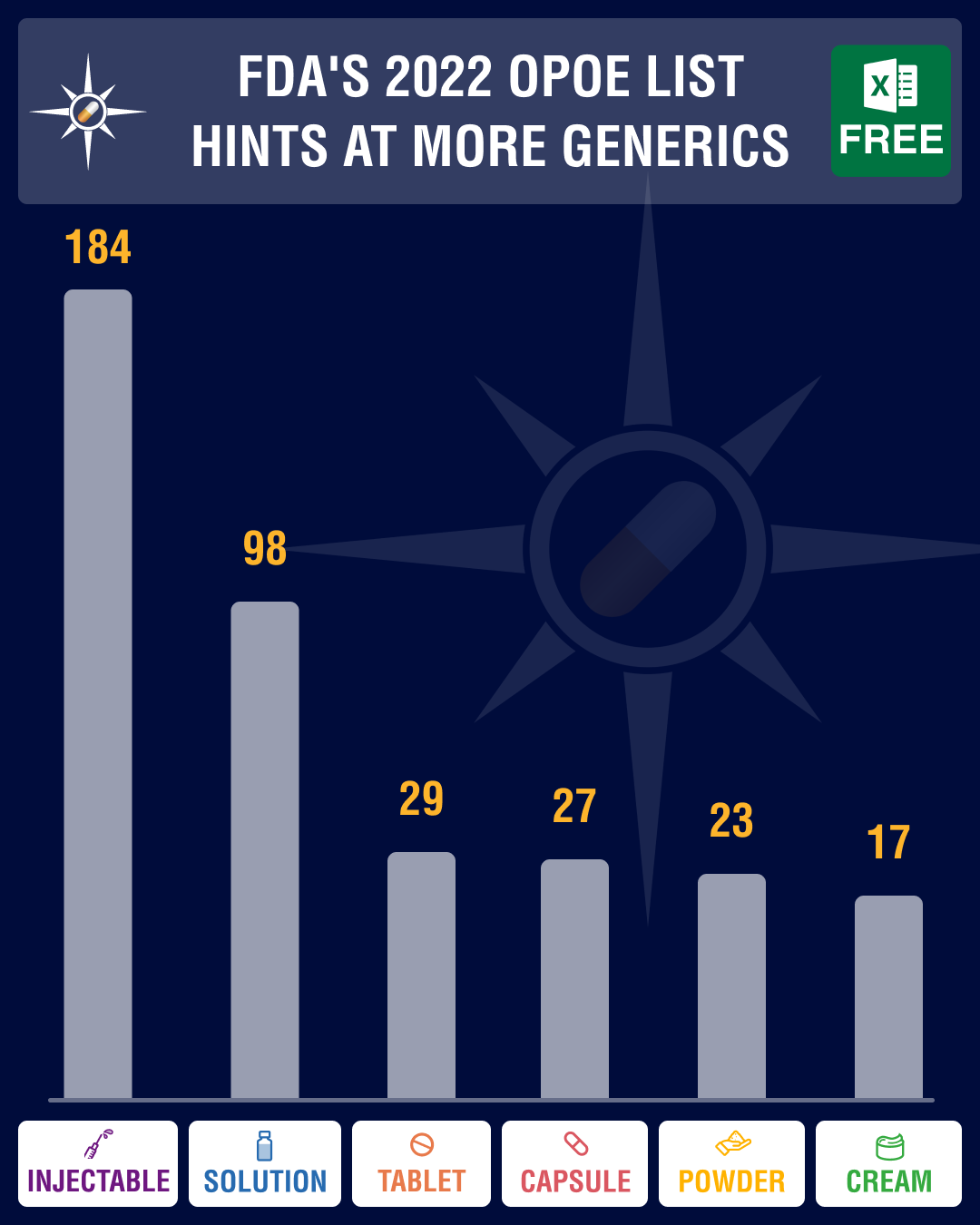

https://www.pharmacompass.com/radio-compass-blog/fda-s-list-of-off-patent-drugs-suggests-higher-approvals-of-first-generics-in-2022

Impressions: 2621

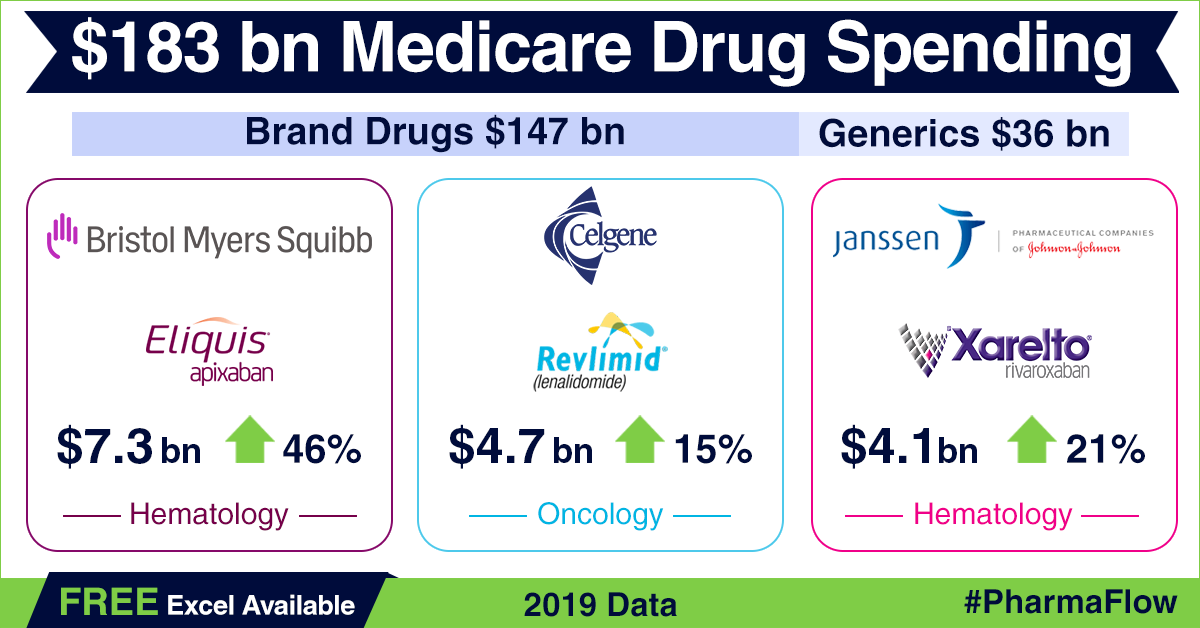

https://www.pharmacompass.com/radio-compass-blog/america-s-drug-price-hike-conundrum-in-backdrop-of-2019-medicare-part-d-data

Impressions: 54747

https://www.pharmacompass.com/radio-compass-blog/top-drugs-and-pharmaceutical-companies-of-2019-by-revenues

Impressions: 14508

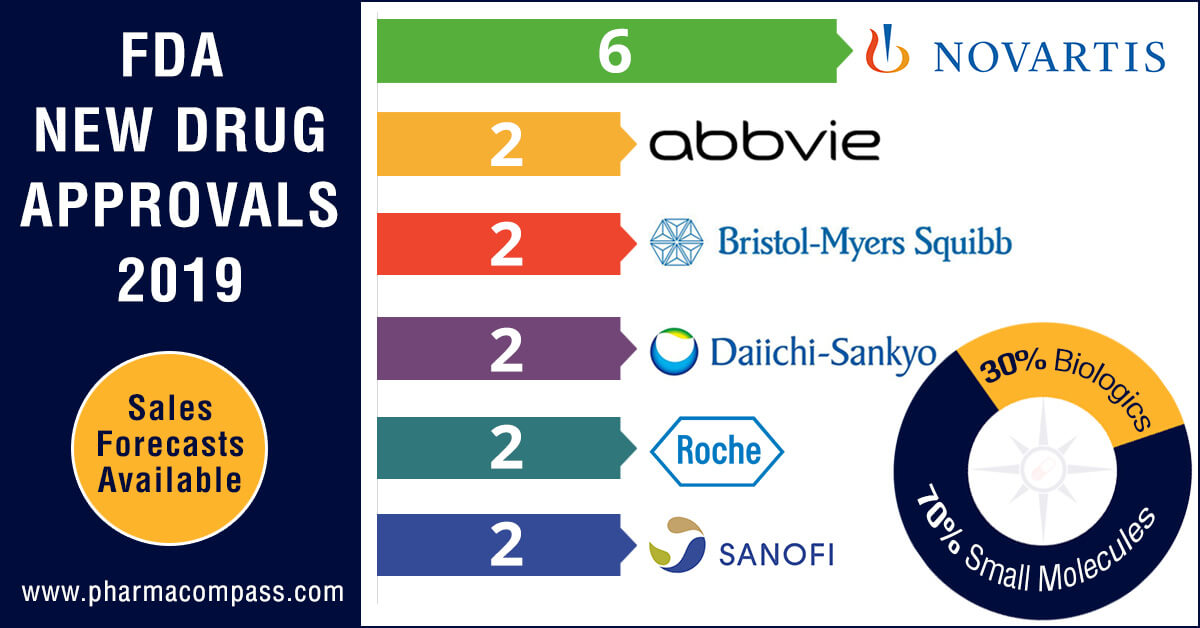

https://www.pharmacompass.com/radio-compass-blog/novartis-leads-in-new-drug-approvals-vertex-s-cystic-fibrosis-med-holds-highest-sales-potential

Impressions: 4698

https://www.pharmacompass.com/radio-compass-blog/us-market-offers-niche-opportunities-reveals-manufacturer-sales-data-from-medicare-part-d

Impressions: 58400

https://www.pharmacompass.com/radio-compass-blog/top-drugs-by-sales-in-2017-who-sold-the-blockbuster-drugs